President Energy is an oil and gas exploration and production company. It currently has producing assets in the US and Argentina and has exploration assets in Paraguay.

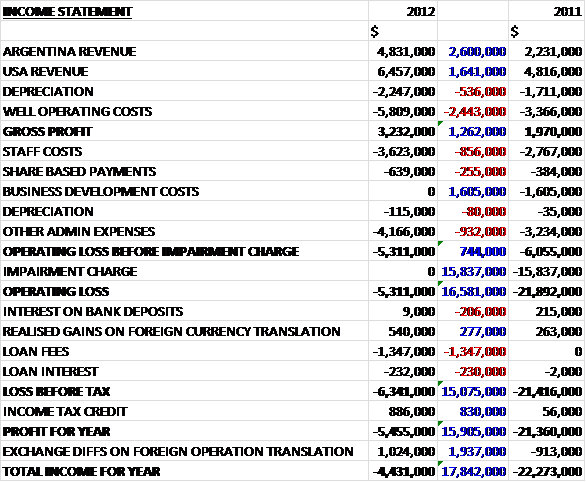

President receives revenue from its Argentinian and US assets. Argentinian revenue more than doubled to $4.8M year on year due to development drilling undertaken and the contribution of a full year or production, and US revenue was up $1.6M to $6.5M. Well operating costs also increased, up $2.4M to $5.8M reflecting a full year of Argentinian production costs, and the group also experienced a $536K increase in depreciation to give a gross profit of $3.2M, up by $1.3M on last year. As far as admin costs were concerned, there was a $856K increase in staff costs, along with a $255K increase in share based payments. There was the lack of a $1.6M business development cost but other admin expenses were $932K higher, which meant that operating loss before last year’s impairment charge was $5.3M, compared to a loss of $6.1M in 2011. That impairment charge in 2011 was $15.8M, relating mainly to the East Lake Verret assets in Louisianna which had been written off due to the fact that no commercial reserves were found, which obviously skews the results for that year. Finance costs in 2012 were up, driven by $1.4M in loan fees so, after a tax credit the loss for the year was $5.5M, $15.9M better than last year but it would have been broadly fat were it not for that impairment charge.

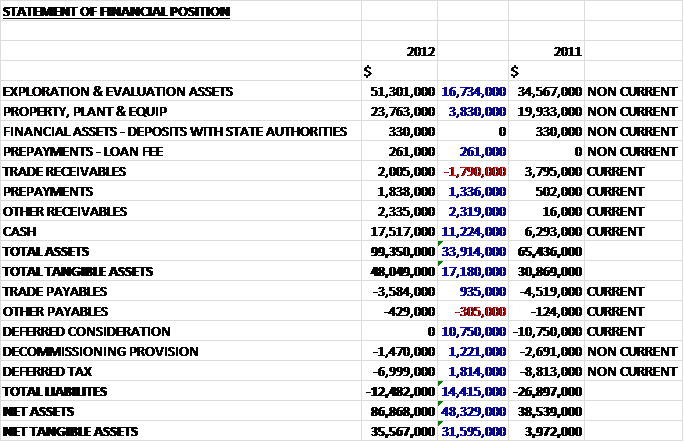

Overall, total assets were up an impressive $33.9M. The main drivers were a $16.7M increase in capitalised exploration assets relating mainly to the entry into Paraguay via two farm-in agreements, along with some new exploration licenses in Argentina. There is also an amount of $14.6M carried relating to the Australian assets that the group is looking to farm out. Other drivers include a $11.2M increase in cash due to the issue of new shares, a $3.8M hike in fixed assets and $2.3M more of other receivables, only slightly mitigated by a $1.8M reduction in trade receivables. Almost all liabilities fell, driven in particular by the lack of $10.8M worth of deferred consideration and a $1.2M fall in decommissioning provisions leading to net assets that were some $48.3M higher at $86.9M.

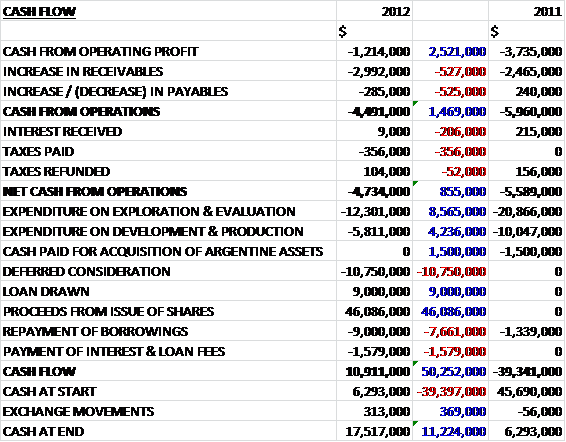

The cash outflow before movements in working capital was $1.2M, $2.5M better than last year. An increase in receivables led to cash from operations being $1.5M better than in 2011 at -$4.5M. After tax, the net cash outflow from operations was $4.7M. The group then spent $12.3M on exploration & evaluation, and $5.8M on development & production, both less than in 2011. They also spent $1.6M on loan fees and $10.75M of deferred consideration relating to the acquisition in Argentina, and in order to pay for all this, issued new shares to the value of $46.1M. For the year, the cash flow was $10.9M, a whole $50.3M better than last year for what it’s worth.

The group have a number of capital commitments going forward. They are committed to funding a three year exploration programme on each of the Matorras and Ocultar license areas in Argentina. They will have a modest seismic re-processing and new seismic acquisition commitment of $2M each. The group also intend to incrementally acquire up to 59% in the Pirity concession (from 12%) and 60% in the Demattei concession (from 3%), both in Paraguay. This will be done by funding agreed seismic work and three wells in each block. The anticipated cost of seismic acquisition, processing and interpretation is $9.5M.

The group is fairly exposed to movements in exchange rates with the USD/Argentinian Peso the most important – a 10% move would affect the profit or loss account by $576K.

After the end date of the balance sheet, the successful drilling of the A-54 well on the East White Lake Field in Louisiana provided additional production of about 50 bopd taking production is Louisiana as a whole to 250 boepd. The company has also completed a comprehensive seismic reprocessing exercise on the five fields in the Puesto Guardian Concession in Argentina. The work identified significant undrilled highs within the field, confirming the further development potential. In the Pozo Escondido field, STOIIP increased from 20mmb to 63mmb. Also in Argentina, a work over and frack campaign at the Pozo Escondido and Dos Puntitas fields are expected to give a lift to production there. In Paraguay, seismic acquisition operations have begun and were acquired over the high-graded areas of the Pirity and Demattei Concessions. The group are targeting an initial three well drilling campaign for 2014.

In September the group announced a farm in agreement for two blocks in the Pirity sub basin in Paraguay. An independent assessment gives a net mean risked recoverable prospective resources of 94 mmbbls of oil which could give a $2BN success case value to President, a huge premium on the current market cap. The results of the seismic operations should be available in Q4 2013 and the seismic exploration company, Global, has agreed a success based fee with the group in the form of a discovery bonus. Some progress has been made on infrastructure and planning has been commenced for the Q2 2014 drilling programme.

In Argentina, the group drilled three new wells. The DP-1001 well was brought on stream while the PEE-1001 and P-1002 wells are part of a future frack sidetrack and work-over programme. The group also commenced a three well fracking campaign targeting carbonate reservoirs in the Dos Puntitas and Pozo Escondido fields. If they are successful, it provides encouragement for a further sequence of fracks to target the large oil reserve in place at this reservoir. An exploration prospect in the Martinez del Tineo field was independently reviewed. The gas and condensate target at the site near the Bolivian border was assessed to have an unrisked prospective resource estimate of 570 bcf and 14.5M barrels of condensate. Based on this prospect, the group applied for three open exploration concessions and were awarded two blocks as operator, with three years to study the concessions on which only sparse data is currently available.

In Louisiana, operations in East White Lake and East Lake Verret continued to provide solid cash flow. Production was up 15% on last year at 183boepd and continued to rise after the end of the year after a successful new well. New exploration leads have also been identified in the area. The Australian assets are not core to the central strategy of the group with work continuing only at a low level.

As of the end of the year, the group is in a position of no debt and has a $15M, 24 month facility that it can draw on if needs be. The group currently has 2,306.3 mboe of proved reserves, a fall of 129.1 mboe due to production at Louisiana and Argentina. There are also another 4,566 mboe of provable reserves, a fall of 207.8 mboe on last year due to the decision not to proceed with the development of wells for which probably reserves were previously recognised in East Lake Verret.

The US assets provide some dependent cash flow and the Argentinian fields seem to be increasing production to a decent level. It is the assets in Paraguay, however, that make President such an interesting proposition. Should they be successful there, there is real upside potential and should they not hit black gold there, there are still the Argentinian and US assets to fall back on. It would be nice to see some more exploration areas in the pipeline but I am happy with the risks involved given the potential in Paraguay. I have taken a small position here.