President Energy has finally released its final results for the year ended 2015.

Revenues fell during the year as a $940K growth in Argentina revenue was more than offset by a $3.4M decline in US revenue. Depreciation was down somewhat but well operating costs increased by £1M which meant there was a small gross loss, a detrimental movement of $3.2M year on year. Staff costs fell by $944K but other admin expenses grew by $2M reflecting lower levels of capitalisation last year and a $600K legal cost relating to the dispute over the Pirity concession which meant that the operating loss increased by $4.2M before impairments and revaluation gains. After no gains were made this year and impairments remained roughly the same, the actual operating loss saw a $33M detrimental movement. There was then a $499K growth in realised gains on forex translations and a $762K reduction in loan fees, offset by a $1.2M increase in loan interest. This all meant that the loss for the year was $18.5M, a detrimental movement of $33.1M year on year.

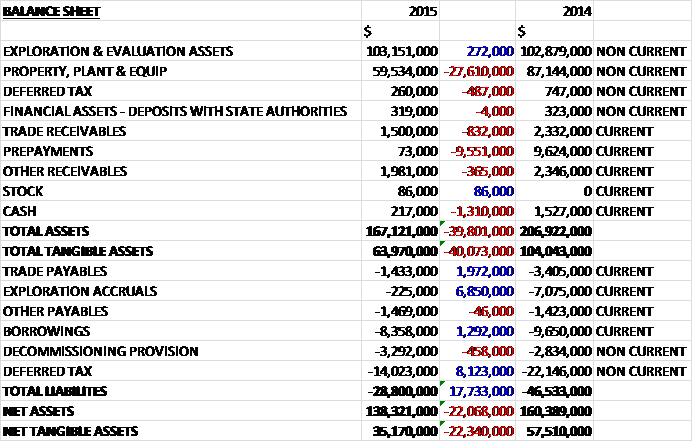

When compared to the end point of last year, total assets declined by $167.1M, mainly as a result of forex differences and driven by a $27.6M decline in property, plant and equipment, a $9.6M fall in prepayments following the end of the Paraguay drilling programme, and a $1.3M decrease in cash. Total liabilities also declined during the year due to an $8.1M fall in deferred tax liabilities, a $6.9M decrease in exploration accruals, a $2M decline in trade payables and a $1.3M fall in borrowings. The end result is a net tangible asset level of $35.2M, a decline of $22.3M year on year.

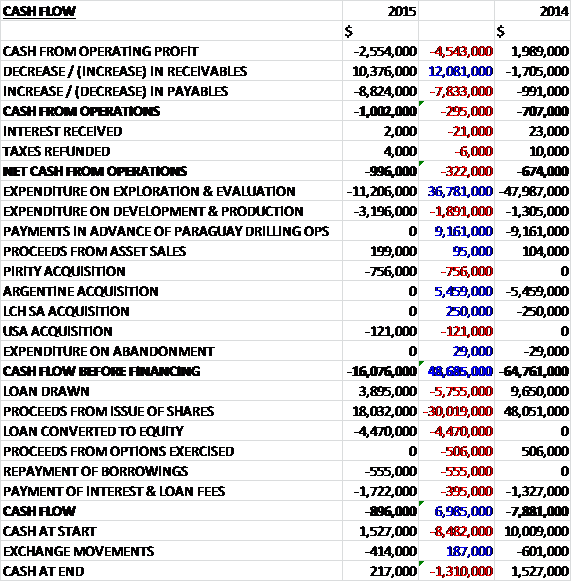

Before movements in working capital, cash losses were $2.6M, a detrimental movement of $5.4M over last year. There was a cash inflow from working capital due to a decline in receivables and the net cash outflow from operations came in at $996K, an increase of $322K year on year. The group spent $11.2M on exploration and evaluation relating to the Pirity drilling and Hernandarias seismic survey, along with $3.2M on development and production relating to workovers in Argentina with a further $756K being spent on the Pirity acquisition to give a cash outflow of $16.1M before financing. The group then received $18M from share placings and after loan fees and interest, along with a portion of the loan being converted into equity meant that there was a cash outflow of $896K for the year and a cash level of just $217K at the year-end.

Overall production at Puesto Guardian in Argentina increased by 23,925bbls to 98,781 due to the consolidation of the remaining 50% not already owned at the concession in July 2014. In the US, oil production at East Lake Verret increased by 9,723bbls to 14,846bbls with natural gas production up 39.8mmcf to 45.6mmcf. Conversely, oil production at East White Lake declined by 19,604bbls to 44,652bbls but natural gas production increased by 14.9mmcf. This production was offset by a 1,967mboe increase in Argentine reserves following the extension of the license term and the latest reserve report, to give a total proved reserves of 11,192.8mboe.

The operating loss in Argentina was $2.1M, an increase of $1.1M year on year on gross production that decreased by about 33boepd to 271boepd with the average in the second half of the year reaching 312bopd due to the subsequent workovers. This increased further to 500bopd after the workovers in March 2016. During the year the group averaged $67 per barrel compared to $76 last year and it now stands even lower, down at $58 per barrel, although the full effect the reduction has been cushioned by the recent depreciation of the Argentine Peso but well operating costs were still high at $64 per boe.

During the year the 2P oil reserves in these fields were assessed to be 18.1mmbls, of which 11mmbls were proven reserves with a 2P NPV10 value of $329M representing an increase of 28% in 2P oil reserves over the prior year. During the year two sets of workovers of old wells were completed and the improvements in the Argentine economy along with the improving international perception of the country to investors gives the board confidence in building on the work carried out this year.

The operating loss in Paraguay was $461K, an increase of $421K when compared to last year. The main work carried out in the year was the 607km of new 2D seismic acquired over the Hernandarias block the results of which identified several drillable Palaeozoic prospects at 2,500m to 3,000m depth (about 1,000m shallower than the two exploration wells drilled in 2014). The first candidate for a well has been determined to be the Boqueron prospect.

In January 2016 the time for fulfilment of the exploration work programme at the Pirity concession was extended to September 2017 with the possibility of a further extension of six months. The Hernandarias concession, in line with legal requirements, was narrowed down to an area of about 7,982 km2 with the balance of 2,455 km2 being hived off into a new Don Quijote contract area for which President is the contracting party. The group has further been awarded a prospection contract for a small 610 km2 area between Hernandarias and Pirity named Pilcomayo.

In April 2016 the term of the Dermattei concession expired with no extension being granted. The group had previously relinquished its right to further farm in to that area and whilst on expiration they hold 10%, they do not consider this to be a material event. It is understood that the operator of that block has made certain claims in the Paraguay courts against the government in relation to the concession but President is not party to any such litigation. The $10.9M spent on the concession has been fully impaired during the year. After the upcoming drilling programme in Argentina gains traction, the group will once again re-focus on exploration activity in Paraguay.

The operating profit in the US was $971K, a decline of $1.6M when compared to 2014 with the average price of oil in Louisiana falling from $43 per boe compared to $85 last year and the production remaining broadly flat at 219boepd. At the time of writing the sales price has fallen further to $40 per barrel but well operating costs remain low, at $15.4 per barrel. This level of production was supported by small accretive acquisitions of production and revenue interest in the operated Simmons well and the processing facility. Natural declines occurred in all wells in the East Lake Verret and East White Lake fields which was in part mitigated by those small acquisitions and the revenue interest in the Eagle Crest well starting in mid-2015.

The profitability in the region was materially impacted by the fall in oil prices. Oil prices remain volatile and the reduced contribution to the group from Louisiana is set to continue as natural field decline rates continue. With increased focus on Argentina, the group is no longer considering Louisiana a core contributing asset in the medium or longer term.

No material events took place in Australia, although the PEL82 license term was extended to March 2017. Whilst this is not a core asset and it has been written off on the books, it may have a potential future value to the company in a recovering market environment.

The litigation claims by the group’s former partners in the Pirity concession in Paraguay were settled and subsequently the group acquired their residual 36% ownership in the concession for $500K and the time for completion of the exploration work on the block was extended.

During the year the group raised $18M in a placing to fund new seismic acquisition in Paraguay, work in Argentina and for other general costs.

At the end of the year, the group had cash balances of just $200K. In addition they had $5.6M in undrawn loan facilities, although it should be noted that because the lender is owned by the executive chairman and CEO, it is likely to remain supportive.

The year has seen the departure of John Hamilton, Ben Wilkinson, Richard Hubbard, David Jenkins, David Wake-Walker and Alistair Burt from the board, and the appointment of Rob Shepherd and Jorge Bongiovanni as non-executive directors and Peter Levine becoming CEO as well as executive Chairman. Whilst this doesn’t seem great on a corporate responsibility point of view, it should help save money.

The Q2 2016 workover campaign raised Puesto Guardian production to an initial level of 500bopd with a further workover programme currently being conducted on another two producing wells. Planning continues for the drilling of three new production wells in the second half of 2016, targeted to materially uplift production with loan funding in principle in place. The emphasis in 2016 will be to increase production, cash generation and margins so the focus is on the new drilling programme in Argentina in H2.

The company is still loss making so an analysis of PE ratios wouldn’t reveal much.

A three well drilling programme is expected to start before the end of July. The programme is currently planned to be completed with the wells being brought on stream in stages throughout H2 2016. The results will then be analysed with a view to considering a further drilling programme in 2017. The wells will be side tracks from existing shut in wells with horizontal producing sections, will comprise one well each from the Dos Puntitos, Pozo Escondido and Puesto Guardian fields, and will target both proven and provable oil reserves. Planning is advanced and discussions with contractors ongoing with long lead tie items in the process of being ordered. There is an agreement in principle with the lender to provide the entire financial support for the programme by way of an unsecured senior debt facility.

Overall then, this has been a very difficult year for the group as the oil price continued to tumble. They were loss making and losses increased year on year. Net assets declined and the operating cash outflow deteriorated further with cash levels of just $217K at the year-end. The Argentinian business was loss-making as high production costs mitigated the $67 per barrel the group is receiving for their oil. With average production of 312bopod in the second half, production has now increased further to 500bopd since the year-end so at some point hopefully the business will break-even, although I am not sure where that point is. The uptick in reserves is very pleasing, however.

Progress in Paraguay was slow and it seems as though the Demattei costs have been wasted. The US is still profitable due to the low cost of production, with production levels remaining flat. In the short term, however, the investment case here is based on Argentina. Production is definitely being increased here so it really depends on how profitable that is. Another point to note is the cash levels. These were very low at the year-end and the group is having to spend more money on new wells. The financing is being provided by the Chairman and CEO but at what cost us currently unclear.

On the 28th June the group released an operating and funding update. In Argentina the drilling rig is currently being readied and will then be mobilised on sire with drilling of the first well planned to start at the end of July. The first well will be at Dos Puntitas with a 500m horizontal section and the subsequent two wells will be at Pozo Escondido Este and Puesto Guardian. It is estimated that each well will take about one month to drill and complete with the first two wells being drilled back to back and the third to be drilled in the autumn after the rig is used by a neighbouring operator.

To finance the drilling programme, the group have entered into revised funding arrangements with the Chairman’s investment group. This will be an increased facility of $20M comprising an additional $5M to the company’s existing loan facility of $10M and a $1M extension to the existing convertible loan of $4M.

Interest on the enlarged convertible loan will accrue but will not be payable until June 2017. In addition, a 3% net profit interest based on profits over the life of the three new wells will be payable! Ouch, that is a bit of a kicker!

On the 11th July the group announced that Chairman Peter Levine purchased 503,750 shares at a value of £37.6K and then on the 18th he purchased a further 150,000 shares at a value of £11.8K. He now owns 122,488,336 shares in the company equal to about 23% of the total share capital.

On the 26th July it was announced that Chairman Peter Levine purchased another 300,000 shares at a value of £28.5K and now owns 122,788,336 shares in the company.

On the 8th August the group released a drilling update. Drilling of the DP1002 S/T development well at Dos Puntitas in Puesto Guardian has now commenced with the estimate drilling time considered to be about one month.

The group also announced that drilling of the A55 S/T well at the 22% owned East White Lake field in Louisiana has taken place. Results of the logs and side well cores show good quality sand with aggregate net oil pay in excess of forty feet with one sections being 28 feet of Y2 sand at a depth of between 9,360 and 9,390 feet with 25% porosity. The well is now being completed as a producer and is expected to be online in September. The well will make a positive contribution to the group’s net production in the region. They expect initial production to be in line with similar wells which have had initial gross flow rates of at least 250bopd.

On the 2nd September the group released an operational update. In Argentina, drilling operations are ongoing, albeit with certain delays. Five days were lost due to electro-mechanical issues relating to the drilling rig. This is substantially at zero cost to the group and after the issues were resolved, the rig has delivered drilling rates of penetration ahead of expectations.

The well reached 3,475m before a material metal failure in a drill pipe of the drilling contractor caused loss of the bottom hole assembly, for which the group has in place insurance cover. A cement plug is now being set and the well will continue to be drilled out from 2,920m. Up to the date of the failure the well was being drilled on plan with oil based mud and with no material surprises in the geological formations encountered.

The side track out from 2,920m will be drilled to the casing point at the start of the Yacoraite section being at 3,850m. On casing, the horizontal leg will be drilled, the well tested and then hooked up with full production targeted for the first half of October. The base case initial projected production for this well is 500bopd, which would double the existing production levels at the concession.

Current daily production in Puesto Guardian is now at 510bopd having had an average of 440bopd in July. A workover of four old shut in wells will start in September and are designed to achieve a helpful increment to overall production as well as to expand the group’s inventory of producing wells to give a more stabilised field production rate.

Having suffered from well declines and shut-ins in the year to date, Louisiana production is projected to be back in the region of 200 to 250boepd by the end of September as a result of two wells coming on stream. The business continues to generate free operating cash flow despite the prevailing low oil price.