Victoria oil and gas has now released its final results for the year ended 2015. This only includes the months since the previous year end in May and sadly they have not included any seven month comparisons so many comparisons to last year are rendered useless.

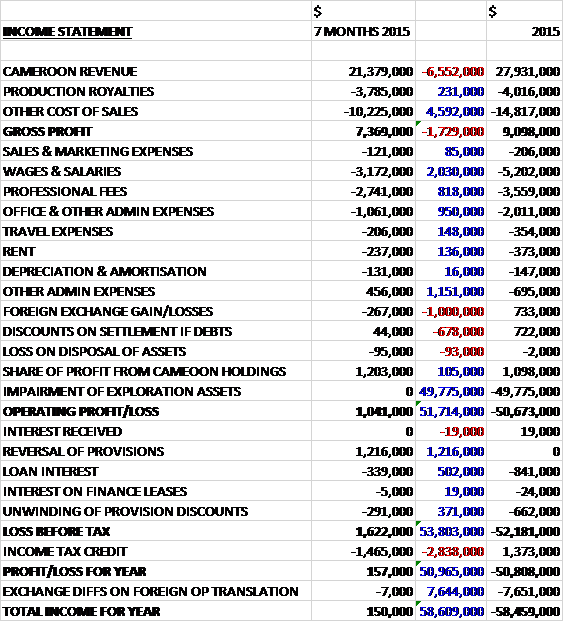

Cost of sales declined less than revenues which meant that the gross profit was down by $1.7M. Wages and salaries reduced by $2M, professional fees declined by $818K and office and other costs decreased by $950K. A $1.2M decline in other admin expenses was mostly offset by a $1M detrimental forex movement and before last year’s impairment, the operating profit came in at $1M, an improvement of $1.9M year on year. We then see a $1.2M provision reversal and loan interest fell by $502K. After a $1.5M tax charge, mainly relating to the deferred tax relating from a change in estimate, the profit for the period was $157K.

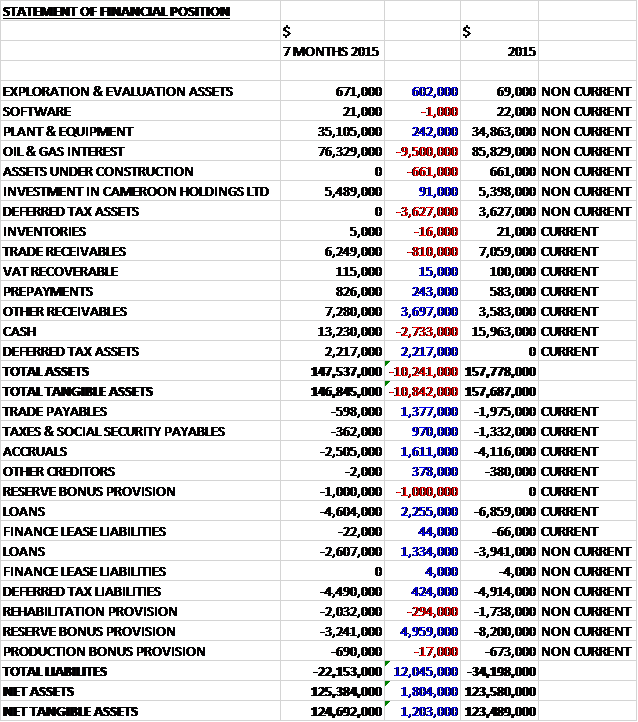

When compared to the end point of last year, total assets declined by $10.2M driven by a $9.5M fall in oil and gas assets, a $1.4M decline in deferred tax assets which should be utilised in the coming year and a $2.7M decrease in cash, partially offset by a $3.7M growth in other receivables, mostly relating to RSM receivables. Total liabilities also declined during the period due to a $4M fall in the reserve bonus provision, a $3.6M decline in loans, a $1.6M decrease in accruals and a $1.4M decline in trade payables. The end result was a net tangible asset level of $124.7M, a growth of $1.2M over the period.

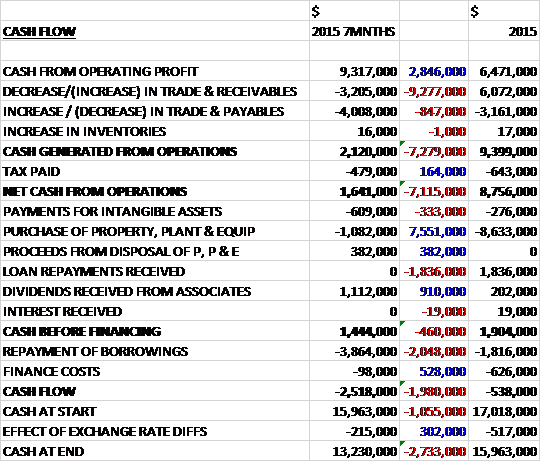

Before movements in working capital, cash profits increased by $2.8M to $9.3M. There was a large working capital cash outflow, however, with an increase in receivables and a decline in payables which meant that after tax the net cash from operations was $1.6M, a decline of $7.1M year on year. The group spent $1.1M on fixed tangible assets and $609K on intangibles but a dividend from the Cameroon royalty company meant that there was a free cash flow of $1.4M. This did not cover the $3.9M of debt repayments, however, and the cash outflow for the period was $2.5M and the cash level at the year-end was $13.2M.

During the period the group produced an average of 8.57mmscf per day of gas compared to 3.95mmscf in the same period of last year, with both the ENEO power stations consuming gas for grid power for the whole period. Condensate sales were 16,055bbls compared to 13,598bbls last year.

Dangote was commissioned in June 2015 and both Sic Cacaos and New Foods were commissioned in May with all three companies consuming consistently since. Both New Foods and Sic Cacaos are consuming at their expected levels while Dangote continues to increase production at its new clinker plant. The newly established sales team is focused on increasing the group’s reach into the Bonaberi area and during the period, eleven new thermal gas connections were signed.

The group has a contract price bracket of $9 to $16 per mmbtu for its gas sales and a sales price for its condensate based on the Brent oil price. The fall in the market price of alternate products to their gas has made them more price competitive than previously which has resulted in a small number of customers switching away from gas.

As far as the grid power is concerned, during the period the short-term genset equipment rental contracts with the industrial power customers came to an end, as did the related contract with the provider of the gensets although the group remains a gas supplier to these customers.

The phase II Bonaberi line extends the existing pipeline from Magzi 2 Industrial Estate to Maya Oil factory, a distance of about 8km. The two material customer connections on this phase are Maya & Cie and SMS Shal. The larger of the two is Maya & Cie, a cooking oil and soap producing company located on the Bonaberi road. Their initial estimated consumption is expected to be 380,000scf per day but demand is expected to increase. At the current time, 3.7km of pipe has been laid and an additional 1.3km of pipe has been welded and is ready to be laid. The customers on this phase are expected to come online during Q3 2016.

Beyond Maya Oil, upon completion of Phase II, the Phase II pipeline will start. This is planned to add an additional 5.5km to five new customers with 130,000scf per day of expected consumption. These customers are expected to be online by late 2016.

During the period the group has been preparing to drill two wells onshore at the Logbaba field to supplement the two existing production wells. The new wells are required to meet the demand for gas, to develop the Logbaba reserves and to move some of the 2P reserves into the 1P category. One of the wells will twin the La-104 well drilled in 1957 and the other well will be a step out well that will be drilled into a target that is intended to add to the probable reserves. Both of the wells will be drilled directionally from the one drilling pad adjacent to the Logbaba gas plant and they are to be tied into the production facilities immediately after they are completed. The La-104 well is almost vertical but the step out well will be drilled to intersect a target that is about 1,100m to the SE of the pad.

In addition to developing the gas reserves in the Logbaba formation, the La-104 twin has an optional additional objective of an exploration tail which can be drilled from the bottom of the Logbaba formation (at about 3,200m) down to 4,200m below the surface to test the hydrocarbon potential of the Mundeck formation which had gas shows in well La-104.

The group has sourced a drilling rig which is currently en-route to Cameroon. Petrofac is providing well design and project management services and they are now working on the design and programme preparation. Major site preparation work is underway including slope stabilisation, levelling for drilling rig tracks and drilling pad preparations. New warehousing for rig supplies, storage and camp civils are also under construction with long lead time orders being placed. The budget for the two wells is less than $40M, excluding the optional exploration tail.

Following the purchase of the gas processing plant in May 2015, the expansion study has been completed. Stage one of the expansion, from 20mmscf per day to 25mmscf capacity is in the preliminary engineering phase and with further expansion phased being tied in with the well results.

In February 2016, the group reached an agreement with Glencore to acquire a 75% participating interest in the Matanda Block. The group, as operator, will assume responsibility for carrying out a proposed work programme, to be agreed by the Cameroon government. There was no consideration for the acquisition but they group has assumed the work programme obligations which includes seismic work to be performed in the near term in a range of $8M to $10M to be spent over a two to three year period. The acquisition comes with some assets, which the directors estimate to have a value of over $4M.

The block is adjacent to the Logbaba operation and covers an area some sixty times the size of the Logbaba concession. It is highly prospective for significant natural gas and gas condensate resources. The North Matanda field is estimated to hold a P50 gas in place volume of 1.8tcf and condensate in place of 136mmbls. The remaining 25% interest is controlled by AFEX, a Bahrain based company and the first phase of seismic data acquisition is expected to start in Q4 2016. The existing Logbaba gas network infrastructure will allow for fast track development of any new discoveries made.

The board have stated that they are looking for other opportunities within Africa and they continue to assess some projects. The plan is to focus on the development phase of projects and enter at a point after the discovery of gas and prior to the development of the field. I have to say that I think it is a bit soon for that – I would rather they got to the point where Cameroon is consistently profitable and cash generative first. They have also stated that they continue to seek a partner or purchaser for the Russian asset (which has been fully impaired already).

It is very relevant that RSM will start to receive their 40% of revenues from the Logbaba concession from May, although there is still $2.6M of receivables not yet paid so in reality they probably won’t start getting anything straight away, but going forward this is going to be very significant.

The group is liable to pay a bonus determined four years after commencement of production by reference to the reserves of the field. The directors have previously provided $10M for this, being the bonus payable based on the expected reserves four years from first production. During the period the counterparty has initiated arbitration proceedings over the timing of the reserve bonus payments. Based on proceedings to date, management are of the opinion that the reserve bonus provision should be just $5M, a portion of which ($1M) is reflected as a current liability. A contingent liability of $5M exists, therefore, should the arbitration ruling favour the counterparty.

In March 2016 the group received a land claim amounting to $1.6M. This claim states that certain property rights have been infringed by the pipeline network laid by the company. The directors believe the claim is without merit and it is being challenged.

At the year-end, the group had a cash balance of $13.2M. In April 2016 the group secured a debt facility with BGFI of $26M to support the capital expansion and exploration programme planned for 2016. The facility is repayable over five years, bears interest which currently stands at 7.15% per annum. At the year-end, the group had spent $500K relating to the drilling programme in 2016. Since then, they have spent a further $4.9M, including $2M of mobilisation costs to get the selected drill rig to the Logbaba site. They have a further commitment of $12.2M which is expected to be spent during 2016.

The group has a net cash position of $6M as of the end of the year compared to $5.1M at the previous period-end. At the current level of profitability the shares look very overvalued with a PE ratio of 424.5 and unfortunately I can’t find any analyst forecasts.

Overall then this was a period of some progress for the group. They made a small profit compared to a small loss last time, their net assets increased and although the operating cash flow declined, this was due to movements in working capital and cash profits increased. Despite the fall in operating cash flow, some free cash was generated. The group have been hit by some customers moving away from gas as the declining oil price has meant some alternatives are better value, so this must be kept in mind.

The upcoming drilling programme also adds some risk here with the budgeted cost of $40M just about covered by the cash reserves and new $26M debt facility, although this does not leave much room for error. The Matanda acquisition looks to be a great opportunistic deal and the concession looks promising, although the $8M to $10M commitment is something else the company will need to spend cash on.

In conclusion, progress is being made but there remains some uncertainty.

On the 31st May the group announced that Deputy Chairman Grant Manheim has retired and current part-time finance director Robert Palmer was also stepping down, to be replaced with the group financial controller, Andrew Diamond.

On the 23rd June he group announced that CEO of GDC Ahmet Dik was promoted to CEO of the whole group – this has been coming for a while I think.

On the 29th June the group announced that the rig had arrived at Douala port and is ready for customs clearance. The schedule is to commence drilling in early Q3 and complete by the end of 2016.

On the 14th July the group announced the appointment of Roger Kennedy at a non-executive director with immediate effect. He is currently chairman of KPC, a family owned company investing in public and private equity. He has also served as a director and head of business development for Star Petroleum.

On the 26th July the group released an update covering Q2. During the quarter, revenue declined by $300K to $12.5M and the net cash position at the end of the period stood at $1.7M compared to $4.6M at the end of Q1, with gross cash reserves of $13.9M.

Total gas sales were 1,151.2mmscf , an increase of 31.2mmscf year on year as a 66.2mmscf decline in retail power sales was more than offset by a 4mmscf increase in thermal power and a 93.4mmscf growth in grid power. The amount of condensate sold declined by 1,010bbls to 12,457bbls. The quarter marks the second half of the dry season which enjoys higher gas consumption than in the wet season.

As of the start of June, the group had received all of the income to satisfy RSM’s portion of the initial exploration costs carried out at the Logbaba gas project. As a result, RSM will now receive 40% of Logbaba revenues which will be net of their 40% contribution to all operational and capital expenses including well drilling, pipeline construction, gas delivery and operating expenses. Through this year it is expected that all revenues from the project will be expended on operational and capital expenses, including the drilling programme. The group has also secured at debt facility with BGFI Bank of up to $26M which it can draw upon at any time to fund ongoing operations.

As previously stated, the group will be drilling two wells to move some of their 2P reserves into the 1P, proven, reserve category. One of the wells will twin the La-104 well drilled in 1957 and the other will be a step-out well that will be drilled into a target that is intended to prove up more of their probable reserves. Both wells are intended to be production wells at depths of up to 3,200m. The budget for these wells is less than $40M and the schedule for the full drill programme is expected to be 187 days from spudding.

The rail-mounted drilling platform has now arrived in Douala and has been offloaded, cleared through customs, transported to site and assembly is now underway. A major task to remove the cliff at the end of the drill pad and stabilise the surface as completed at the drill site; drill pipe levelling and preparation was completed together with three cellars, one for each of the two wells plus a spare were also driven in preparation for spudding. All storage tanks for mud and cuttings were established together with treatment pits. Fly camp and main camp areas have been prepared and both camps were delivered to site and installation has been completed. New warehouse facilities, secure perimeter fencing and upgraded access controls for site have all been installed and completed.

Significant progress was made on the 8km phase 2 Bonaberi pipeline extension during the quarter, adding to the 2.1km of pipe laid in Q1. This follows the commissioning of the phase 1 expansion last year that currently supplies gas to three thermal customers. During the period the phase 2 pipeline was extended with a further 4.7km trench completed and pipe laid.

The group has also started the phase 3 pipeline extension. This is a 5.5km extension reaching out to Bekoko junction. During the period 2.3km of trench was completed and pipe laid. Both phase two and three are on target for commissioning by the end of 2016 and expected to connect a total of twelve additional customers who have already signed gas sales agreements.

So, progress is certainly being made but it has been made clear that there will be no income after capital and operating costs over the coming period.

On the 26th August the group announced that RSM filed a request for arbitration with the ICC regarding the rig and drilling contractor selected by the group to conduct the drilling of two new wells at the Logbaba project. They also filed a complaint and application for injunction with the US District Court in Texas in which they sought a temporary court order to halt the drilling operations while the arbitration proceeds. The group pointed out that RSM has approved the operations including the rig and drilling contractor and therefore RSM withdrew the request for injunction.

The arbitration is still pending, however and the group is well placed to continue funding these operations and the drill programme with project revenue and bank debt until such a time as the arbitration with RSM concludes. This is all a bit ridiculous, I can only assume that RSM has run out of cash and is trying to stall the drill as they can’t afford it.

On the 8th September the group announced that it entered into a settlement that resolves all outstanding issues concerning the previously disclosed Reserve Bonus Payment Agreement and a 1.2% royalty due pursuant to the CPA agreed prior to the group’s involvement with the Logbaba gas project. The commercial terms are not materially different from the combined provision and contingency announced in the accounts of 2015.