QinetiQ has now released their interim results for the year ending 2018.

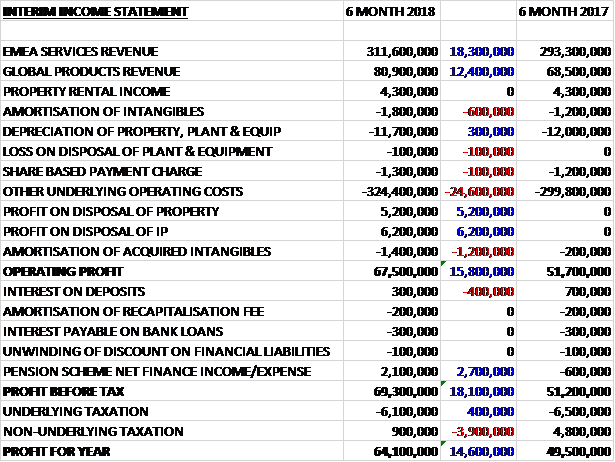

Revenues increased when compared to the first half of last year due to an £18.3M increase in EMEA Services revenue and a £12.4M growth in global products revenue. Amortisation was up £600K and other underlying operating costs grew by £24.6N. The amortisation of acquired intangibles increased by £1.2M but there was a £5.2M profit on the disposal of a property, and a £6.2M profit on the disposal of IP to give an operating profit £15.8M higher. There was a £400K reduction in interest income but there was a £2.7M positive swing to pension scheme income and after tax charges increased by £3.5M the profit for the period was £64.1M, a growth of £14.6M year on year.

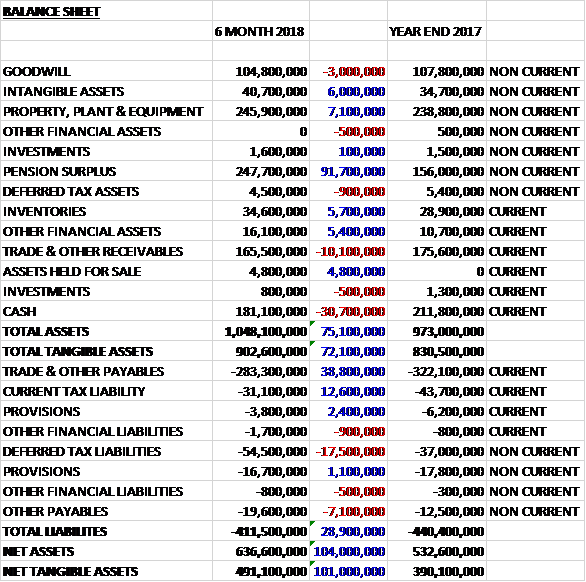

When compared to the end point of last year, total assets increased by £75.1M, driven by a £91.7M increase in the pension surplus, a £7.1M growth in property, plant and equipment, a £6M increase in intangible assets and a £5.7M growth in inventories, partially offset by a £30.7M reduction in cash and a £10.1M fall in receivables. Total liabilities declined during the period as a £17.5M increase in deferred tax liabilities and a £7.1M growth in other payables was more than offset by a £38.8M decline in trade payables and a £12.6M decrease in current tax liabilities related to the timing od the recovery of the R&D expenditure credit. The end result was a net tangible asset level of £491.1M, a growth of £101M over the past six months.

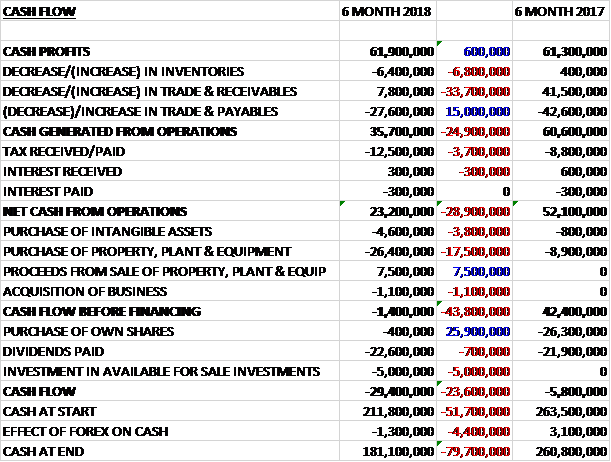

Before movements in working capital, cash profits increased by 600K to £61.9M. There was a cash outflow from working capital, mainly due to a fall in payables and after tax payments increased by £3.7M the net cash from operations was £23.2M, a decline of £28.9M year on year. The group spent £26.4M on property, plant and equipment along with £4.6M on intangible assets and £1.1M on acquisitions, but they did get back £7.5M from the sale of assets to give a cash outflow of £1.4M before financing. They then spent £22.6M on dividends and £5M available for sale investments to give a cash outflow of £29.4M for the period and a cash level of £181.1M at the period-end.

The underlying profit in the EMEA Services division was £47.3M, a growth of £4.3M year on year due to non-recurring trading items such as a £5.3M credit relating to the release of engine servicing obligations as the group invests in new aircraft for test aircrew training and retire their legacy fleet. Excluding these, the Rubikon acquisition and forex movements, the underlying operating profit fell by £3.6M, half of which was driven by the lower baseline profit rate for single source contracts in line with expectations.

The group reported orders of £153.9M, a reduction of £130.4M with the decrease due primarily to last year’s award of the £109M eleven year renewal from the MOD of the Naval Combat system Integration Support Services contract. Excluding this, the Rubikon acquisition and forex movements, orders fells by £30.1M. Around a third of this reduction was the result of the aggregation of smaller aircraft engineering orders into the Strategic Enterprise contract awarded two years ago with the rest relating to a lower level of MOD commitments during the period. On an organic basis, revenue grew by 4% in the period.

In Air and Space the group continue to make good progress under the Strategic Enterprise contract for air engineering services. The contract delivers significant savings to the MOD by aggregating smaller contracts together and the group expects to increase the amount of work brought under the framework. Following the signing of the amendment to the LTPA, they have been transforming test aircrew training and opening up courses to a broader set of international customers, including those in the civil market. During the period they purchased two new Grob G120TP aircraft as part of the upgrade to their fleet to meet growing customer requirements for the evaluation of mission systems.

During the period they reinforced their relationship with Boeing, who use the wind tunnel facility to evaluate their commercial aircraft, with a £25M contract to provide wind tunnel services until 2024. Working with BAE and MBDA, they integrated the Brimstone precision strike missile onto Typhoon, as part of the programme to transfer capabilities from the Tornado GR4; and the business continues to deploy significant resources to develop the gridded ion engine propulsion system to be used on ESA’s Bepi Colombo mission to Mercury. It remains scheduled to launch in October, though various issues with the electric propulsion system still need to be resolved before the launch is formally given the green light to proceed.

In Maritime, land and weapons, in September the group signed an £8M order from the MOD to provide naval combat systems expertise for Type 26 Global Combat Ship which added to the £109M eleven year NCSISS contract agreed with the MOD last year. The German Air Force has placed a £2M contract with the group for an advanced medium range air to air missile trial at the MOD Hebrides range and the group, in collaboration with MILREM, was awarded Defence and Security Accelerator funding for the Last Mile programme which addresses the robotic delivery of supplies to a combat outpost or troops in the field.

In September the Cyber, Information and Training business enabled the connection of the RAF’s Rivet Joint Squadron’s own simulator to the training centre at RAF Waddington for the first time. The milestone is part of an ongoing programme to achieve savings by transforming operational training through the application and integration of synthetic technologies. During the period the business led a multi-industry team from the Secure Information Infrastructure and Services research programme to deliver a low size, weight and power communication information system to 30 users as part of the Exercise Joint Venture 2017.

The Australian business delivered a strong first half with a record level of orders. They signed a contract to manage the explosive ordinance engineering and logistics services at the mine warfare maintenance facilities in Sydney. The business will assume design authority to maintain, update and operate exercise mines and other equipment in support of Australian naval training and readiness requirements.

They signed a contract to design and build a number of engine change cranes to enable safe removal of engines from the Australian Air Force’s C27J aircraft which will also be suitable for use with other aircraft. Their AIR7000 contract acquired through the purchase of Rubikon received an increase in contract ceiling value from $24M to $35M.

In Canada the group completed a project for the coast guard to provide advice that will assist decisions that shape a future fleet for the next fifty years; they were awarded a $5M order from the Canadian Navy for over forty Hammerhead unmanned surface vehicle targets and various payloads. The order was placed under an existing five year $35M framework contract with the Department of National Defence and the order brings total worldwide Hammerhead orders to over 425. They introduced a new service to the Canadian Navy, conducting a live demonstration to emulate the threat of drones to large naval vessels.

In Sweden the group secured contracts with four new customers for training at the flight physiological centre that they operate on behalf of the Swedish defence department. At the period-end, the group announced that they are establishing a new joint venture company in the UAE to manufacture aerial targets for use locally in the acceptance and evaluation of new equipment and the training of armed forces.

Going forward, the board reiterate their guidance for the full year. In EMEA Services revenue under contract is broadly in line with the prior year and the division is expected to deliver modest growth this year, although the lower baseline profit rate for single source contracts represents a headwind for operating margins.

The underlying profit in the Global Products division was £10.2M, an increase of £1.3m when compared to the first half of last year. Orders grew by nearly £30M to £122.4M due to a £13.2M contribution from the QinetiQ Target Systems acquisition, favourable forex movements and the €24.2M spacecraft docking mechanism order with the ESA. Reported revenue was up 18%, driven by the acquisition and favourable forex movements. It was flat on an organic basis at constant currency. At the start of the second half the division has 80% of its full year revenue under contract compared with 98% last time.

The North American business received significant orders in the period, especially in the maritime market where orders totalled $45M. Building on previous work, they were awarded a further significant contract for electromagnetic launch and recovery equipment for the new class of US aircraft carriers. Separately, and in a potential new growth area, the business performed a demonstration of its Dolphin acoustic undersea communication technology.

In land systems, notable achievements included the demonstration of their open architecture Universal Tactical Controller, directing unmanned systems in a shared network operating environment. They supported extensive US government trials with their Titan unmanned ground system to deliver soldiers’ equipment transportation needs. They also received key orders for their air armour and Q-Net RPG protection product lines.

In September they learned they were unsuccessful on the Man Transportable Robotics System INC II programme. The business is currently competing for two further robotics programmes for the DOD and while unmanned systems remains a very competitive field they are confident in their propositions for the remaining programmes.

Optasense performance improved in the period as the business started to see returning confidence in oil field investment combined with the benefits of diversification into adjacent markets. In support of this performance, the business has introduced a more customer-aligned organisation and focused on effective commercial delivery.

They are involved with the delivery of the Trans Anatolian Natural Gas Pipeline Project. During the period they delivered equipment to their partners in Turkey which is the latest milestone of a multi-year effort to secure and deliver a significant international pipeline project. The relative stability of the oil price has resulted in increased capex commitments in specific regions while the interest in the technology by more operations gains pace. They have seen increased adoption and future commitment across the Middle East for both oil and water transport assurance. Security opportunities have become increasingly evident during the period with perimeter and linear asset protection solutions for power facilities and rail lines attracting interest.

The Space Products business signed a €24.2M contract with the ESA to produce a new docking mechanism for the ISS. Under the three year deal, the group will qualify and produce the first model of its International Berthing and Docking Mechanism, designed under a previous ESA contract.

Within EMEA Products, the group’s AS3 communications intelligence system has been added as a payload for Thales’ Watchkeeper unmanned aerial vehicle. It enables the operator to detect signals from military communications devices and then locate, identify and listen to the individuals using them. They developed a counter-unmanned aerial vehicle solution that is being trialled with a number of customers both in the UK and abroad.

Going forward the board reiterate their guidance for the year as a whole. The business’ performance is dependent on the timing of shipments of key orders. As a result of its contracted orders and pipeline of opportunities, as well as the anticipated full year contribution from the Target Systems acquisition, the division is expected to continue to grow in 2018.

In the UK the MOD is under pressure to reduce costs and the impact of Brexit, notably the weakness of Sterling, has put further pressure on defence budgets given the significant amount of dollar denominated programme procurement. The US is expected to show moderate growth. Despite public statements to increase spending, the political environment remains challenging, however. Unpredictability exists in both the budgeting process itself and uncertainty beyond the current Continuing Resolution underwhich the DOD is currently unable to fund new programmes.

In Australia, defence budgets are expected to grow to 2% of GDP by 2021 and in Canada the 2017 review highlighted a significant increase in defence spending through expansion, modernisation and recapitalisation of the Canadian armed forces. In the Middle East, Saudi, the UAE and Qatar are all expected to increase their defence spending by between 0.8% and 2.9% per annum. As governments in these markets grow more sophisticated in their approach to defence, their need for military capability evaluation, assurance and trading are also expected to increase.

The group currently have access to around half of the UK market for defence test and evaluation and they believe that with appropriate investment they can access a greater share of this market, particularly repatriating evaluation work currently undertaken overseas. In addition, there is further opportunity for the group in attracting overseas customers to use their UK-based facilities and expertise, as well as supporting international customers with the development of their own indigenous capabilities.

During the period a deferred tax asset of £1.7M representing UK non-trading losses has been recognised.

The group has a lot of capital commitments. As of the period-end they are contracted for £176.4M with £175M in relation to property, plant and equipment that will be wholly funded by a third party customer under a long-term contract arrangement, mainly relating to investments under the LTPA contract. The additional capex this year will also be recovered in full.

During the period the group announced a joint £17M investment programme in two new tracking radars and upgrades to existing radar facilities at MOD Hebrides. This investment will reduce overall operating costs of the ranges and ensure they provide the capabilities required to support UK defence, defence exports and attract international customers. As part of the LTPA amendment they are investing around £85K over eleven years to test aircrew training at MOD Boscombe Down to purchase eight new aircraft, replacing the oldest aircraft in the fleet, and to introduce a new test pilot syllabus from 2019.

Going forward, overall the board are maintaining their expectations for the group performance in 2018.

At the current share price the shares are trading on a PE ratio of 11.5 which increases to 11.7 on the full year consensus forecast. At the period-end the group had a net cash position of £181.1M compared to £211.8M at the year-end. After a 5% increase in the interim dividend, the shares are yielding 3% which increases to 3.2% on the full year forecast.

On the 8th February the group released a trading update covering Q3 2018. Underlying trading for the group was as expected and the board maintain their expectations for overall performance in 2018.

In EMEA Services trading for the period was in line with expectations. The group is bidding for a number of new opportunities with the UK government that will enable enhanced capability while also driving cost efficiencies. Although the UK environment continues to be challenging, this environment creates opportunities. Internationally the group continued to make good progress, particularly in Australia with positive organic growth and in the Middle East where they have seen strong demand for their advisory services. Trading in Global Products for the period was in line with expectations with good order performance in North America.

During the period the group delivered the first flights of their new aircraft and signed their first multi-year £6M contract with the Royal Netherlands Air Force to train Dutch test pilots and flight engineers until 2022. Under the LTPA contract they received a £9M order to modernise and develop Electro Magnetic Open Sea Ranges.

In the US they won $8M of orders for TALON robots from key defence customers. In Australia an additional $16M has been allocated to their Air 7000 strategic support partner contract which supports the acquisition of airborne maritime surveillance capability. They signed their first £3M contract for the supply of aerial targets and services to a customer in the Middle East, building their presence in the region.

Following the latest triennial valuation and discussions with the pension scheme trustees, the group has confirmed a pension surplus of £140.5M as of the end of June 2017. Consequently, they will cease making cash deficit recovery payments of around £10.5M from March 2018.

On the 9th February the group announced that CFO David Smith purchased 10,188 shares at a value of £20K.

Overall then this has been a fairly steady performance. Profit increased somewhat, net assets were strong, mainly due to the good performance of the pension scheme, but the operating cash flow reduced due to working capital movements – the cash profits were up modestly. There was no free cash generated but this was due to the increased capex requirements of the new framework contract.

Although profits were up, this was mainly due to forex movements and the effect of the acquisition. Organically, profits in Global Products were broadly flat and profits in EMEA Services declined, partly due to the lower profit on single source contracts. Going forward, the lower margins on the single source contract will continue to drag but with a forward PE of 11.7 and yield of 3.2% the shares are not that expensive. Whether it is worth investing here given the lack of organic growth is another question.

On the 24th April the group announced that they had entered into an agreement to acquire EIS Aircraft Operations, currently part of EIS Aircraft group, for €70M. Aircraft Operations is a leading provider of airborne training services based in Germany, delivering threat representation and operational readiness for military customers. It generated €20.1M of revenue and €5.4M EBITDA last year. They deliver airborne training systems using a fleet of 14 leased Pilatus PC-9 and PC-12 aircraft.

They have been the exclusive provider of low speed aerial training services to the German armed forces since 1999 and deliver aerial training services to the US Air Force in Europe. The also modify aircraft for special missions through the integration of sensors and digital systems used in intelligence, surveillance and reconnaissance.

The acquisition is expected to enhance the group’s EPS in the current year and will be funded from available cash resources. It is subject to certain regulatory approvals and is expected to close towards the end of H1 2019.