Ricardo has now released their results covering the full year end 2013. Technical Consulting provides services in relation to the development and implementation of engineering projects and in relation to management and operational consultancy, this segment contains the newly acquired Ricardo-AEA. Performance Products generates income from manufacturing, assembly, software sales and related services.

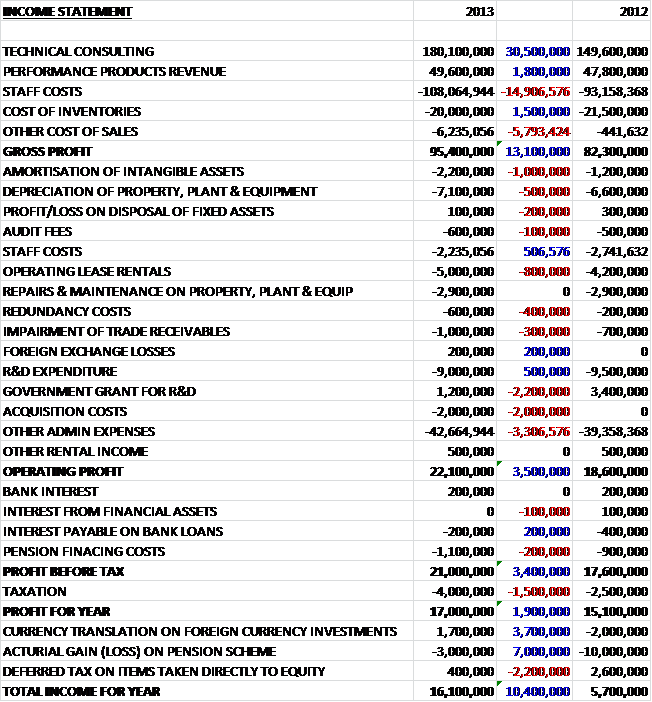

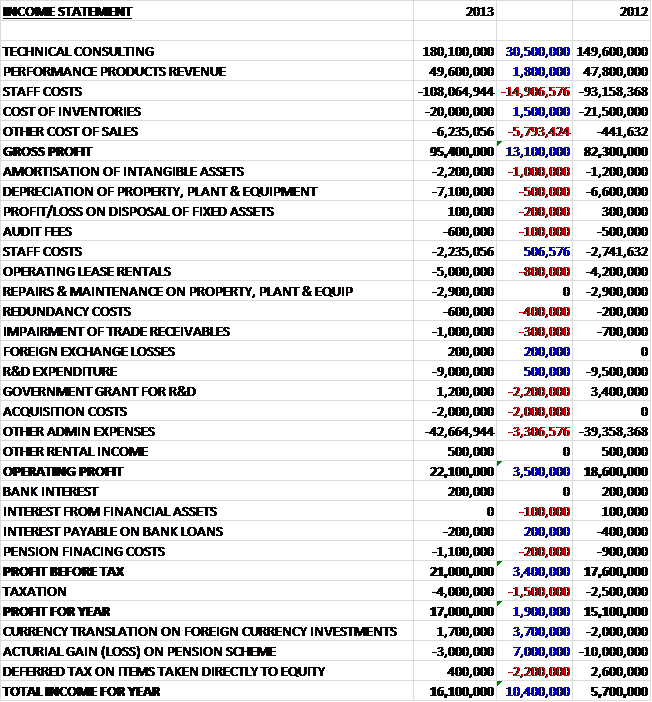

Revenues in the Technical Consulting division were up by £30.5M, mostly due to the extra income from the AEA acquisition. Performance Products revenue also ticked up slightly to just under £50M. Staff costs, as would be expected for the larger group, were up by nearly £15M. This meant that the Gross Profit was £13.1M higher at £95.4M. Admin Costs also increased, as did Amortisation and acquisition costs. There was also a smaller government grant for R&D by the tune of £2.2M. The outcome of this is that Operating profit increased by £3.5M to £22.1M. Taxation was £1.5M higher, primarily due to a legislative restriction in Germany on the utilisation of tax losses so the Profit for the year was £1.9M up at £17M, which was a respectable result.

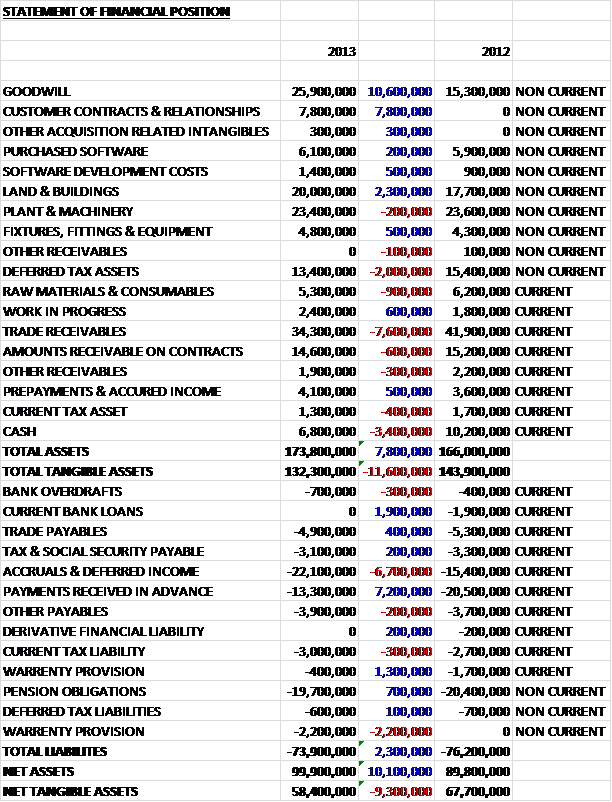

Total assets for the year were up £7.8M but a closer inspection shows that the increase was predominantly in intangible assets with goodwill up by £10.6M and customer relationships up £7.8M. This increase is clearly from the AEA acquisition. The only other major increase was land and buildings, up by £2.3M. A number of assets fell, with the largest fall being the £7.6M reduction in the value of trade receivables. There was also a £2.4M reduction in tax assets and a £3.4M fall in cash.

Liabilities actually fell during the year with the largest fall being a £7.2M reduction in advance payments. The other major fall was in bank loans, down by £1.9M to give a loan position of zero. There were a number of increases too, with accruals up £6.7M being the only major one. This all means that net assets were £10.1M higher than last year but due to the bulk of the asset increases being intangible, net tangible assets actually fell by £9.3M to £58.4M. Given the lack of debt, this is still a very comfortable figure, however.

Cash profits were fairly good, up £4.9M on last year and the movements in working capital were overall somewhat favourable with a decrease in receivables not being entirely mitigated by an increase in payables. There was a fairly hefty pension payment, however, which was £700K higher at £3.7M. In fact, the pension costs took their toll on the net cash from operations again, with the finance costs increasing by £200K to £1.1M. The net cash from operations finished £6.9M better than last year at £29.3M.

Capital expenditure was fairly high and the purchase of property, plant & equipment was up £1.8M to £10.3M and included the construction of the Vehicle Emissions Research Centre in the UK. The largest cost was the acquisition of AEA, however, which was £18M. This was slightly mitigated by £4M of sales of assets which included £3.7M received for the sale and leaseback of the offices in Germany and a £1.6M government grant relating to the Vehicle Emissions Research Centre. Although, a new £10M loan was taken out, this was actually paid back in full, along with £2M of historic borrowing. On top of all this, there was a £6.6M dividend payment. Overall, there was a cash outflow of £3.7M compared to a £5.4M in flow last year but when we consider that there was a net £14M paid on acquisitions, a net £2M reduction in borrowing and £6.6M of dividends paid, this small outflow seems like a very good performance indeed.

The operating profit for Technical Consulting is £16.8M and the profit from Performance Products is £6.1M. This is up from £14.7M and £5.8M respectively last year. Ricardo does seem to be quite exposed to two very large clients. One customer accounted for £36.3M of revenue in Technical Consulting and another customer accounted for £24.3M of revenue split between the two business segments. The failure of one of these clients would be very damaging to the group. The majority of revenues were earned in the UK and this increased further during the year, up £20.4M. Revenues earned in the rest of Europe also increased considerably, up £11.8M. Also doing well was Japan, up £3.8M with the US (up £2.4M) and Malaysia (up £1.5M) performing well too. The only major region to reduce revenues was Germany, where they fell by a very disappointing £5.8M.

On 8th November, the group acquired AEA Technology PLC, which was in administration, for a total cash consideration of £18M which included a goodwill payment of just under £10M. Time will tell, but this looks like a fairly good value acquisition to me. The group is engaged in consultation and advice on environmental matters. Apparently the integration is performing above expectations and is making considerable synergy savings.

Although revenues overall were up 16% in the year, if the contribution from AEA is discounted, this falls to a 3% increase. The order intake in the year was £218M, discounting AEA it was £192M which was a £5M fall on last year. The order book at the end of this year was £121M which is £14M up on the end of last year but £13M down discounting Ricardo-AEA. Within technical consulting, it was noted that more passenger car companies were willing to commit to externally resourced development programs. The group is generally involved in around 400-500 projects at any one time ranging from a few thousand pounds to multi million pound projects.

There has been some change at the board level as Group Finance Director, Paula Bell resigned in May and is now CFO of John Menzies. It sometimes worries me when finance directors unexpectedly resign but at just 46 I guess she must have felt Menzies was the next step up. She is replaced by Ian Gibson who is a chartered accountant with thirty years of commercial experience and was previously CFO at Cable and Wireless Worldwide PLC (albeit he only held that post for just over a year before it was taken over by Vodafone).

Some of the varied projects that the group has been working on over the past year include assistance to Cox Powertrain to develop their engine concept of a new engine that has approximately half the fuel consumption of a state of the art diesel engine. Ricardo worked very closely with Cox, so much so that Cox relocated to the Ricardo Technical Centre site in Shoreham. Typical applications for the new engine would be ferries, coastal patrol boats, motor cruisers and supply vessels for the offshore wind sector. There is also significant military interest, with the Royal Navy ordering a prototype. Cox has now matured as a business and relocated again to its own premises but Ricardo continues to provide engineering consultancy to the group. Ricardo was named a strategic partner for Jaguar Land Rover to help bring its new model line up to launch which included work on the integration of engines, advanced drivelines and chassis systems. The impetus for this project was targeted at the Chinese market which expects luxury sedans powered by downsized engines to avoid the higher rates of tax on large engined imported vehicles. Ricardo’s responsibilities included component design and development, vehicle package management, simulation, testing and the management of the prototype fleet. The resulting cars won significant numbers of new customers in China and were deemed a success.

The newly acquired Ricardo-AEA worked with the Gibraltar government on an on-going project to help the outpost meet EU legislative limits for ambient air quality and to fulfil public information obligations. The group also entered into a three year contract in 2013 with the city of Riyadh (Saudi) to support their air quality policy by providing analysis, measurement, modelling and advice to the city. In the UK, the group has worked on low emission schemes in London and Oxford. Another project was with Aggreko (a provider of industrial generators) providing engineering support to develop a more fuel efficient, cost effective generator. The group has a similar collaboration with Cooper Corp from India to provide a lighter, more fuel efficient, cost effective and quieter generator. The focus for Ricardo’s rail business is on fuel efficiency and exploring alternative fuels and Ricardo has worked with GE Transportation on more fuel efficient locomotives, including a study to determine the efficiency of using natural gas a locomotive fuel source. Ricardo already had a long collaboration with BWM motorcycles and was chosen to assist on the new BWM scooter. By basing the resulting engine on globally produced components and BMW standard parts, there was a lower materials bill with no compromise on quality.

Activity in the Government sector was down on last year due to the cyclical nature of major programmes. During the year, some contracts won included an award by the California Energy Commission to perform a survey of the plug-in electric vehicle marketplace and a project for the US Advanced Research Projects Agency for support of advanced electric motor design. For Ricardo-AEA, the UK Government sector remained its largest market and despite increasing pressure on budgets the group won contracts for the Combined Heat and Power Quality Assurance Programme, the Climate Change Agreements Programme, Resource Efficient Scotland and the Scottish Air Quality Database. The group also expanded internationally with the Riyadh air quality programme.

The Passenger Car business remained a very important sector for Ricardo and project demand was strong with orders from the US, Japan and China as well as the UK from customers such as Jaguar Land Rover. Order intake was well balanced and the need for continued fuel efficiency and lower carbon emissions continued to be an important driver. The High Performance Vehicle sector tends to straddle both technical consulting and performance products and demand remained positive in both motorsport and luxury road cars. In the Motorcycle business new projects were won in both China and Japan in addition to wins from the long standing European customers. Projects include base engine & transmission development, emissions reduction programmes and hybrid & control systems. Activity in the Commercial Vehicles sector was lower than in prior years due to Europe being towards the end of the product development cycle for Euro Vi emissions legislation and North America being yet to define future emissions legislation changes. The focus in Europe this year was on fuel economy improvements and in the US the focus has been on cost reduction and quality improvement programmes. Projects were completed a Japanese OEM and a Chinese manufacturer in Asia. Significant new business wins included engine testing, manufacturing site assessment and power drive unit analysis for US customers and the completion of the European ERTOC project

A slowdown in the Chinese construction industry and the delay of any new legislation in emerging markets has led to lower activity in the Industrial Vehicle sector. There was a continuation of the TaxiBot programme in Israel, which is a vehicle that allows planes to taxi without using their own engines and there were a number of base engine programmes awarded in Europe, Asia and North America. Ricardo’s performance in the Defence sector was very good despite government austerity measures affecting their defence budgets and the group experienced increased penetration into European, Asian and Middle Eastern markets. New contracts included a programme with a European defence vehicle engineering company to develop hybrid technology for an eight wheel drive platform. In the US a contract was secured with DARPA and a test of the new Ricardo engineered vehicle for TARDEC showed that it had a 70% improvement in fuel consumption.

The Rail sector business remained buoyant during the year with order intake doubling on the figure of last year and there is now a very good geographical spread of orders with new clients being won including Bombardier, CNR Dalian and GE Transportation. The new projects have focused on increasing fuel efficiency and looking at alternative fuels. The Power Generation sector experienced increased demand during the year where major areas of activity were large engines for power generation, combined heat, power and energy storage systems and offshore wind generation. Contracts included the previously mentioned work with Aggreko and the support of Atlantis Resources on their tidal energy system. Ricardo-AEA recorded contracts with a large property developer looking at greenhouse gas emissions, air quality monitoring for an airport group, benchmarking the carbon footprint for a food manufacturer’s products, assisting a major global bank to support green investment and waste flow analysis for a services outsourcing provider.

Demand in the Marine sector is being fuelled by the international marine emissions regulations and the introduction of low sulphur fuels. Contracts were completed on several gas engine development programmes and new contract wins included gas engine design, new high speed diesel engines for European and Chinese customers and a European R&D programme aiming to develop new heat recovery and turbo charging systems for marine applications. The Technical Consulting sector started 2014 with a solid order book and a growing order pipeline which includes significant opportunities within the passenger car market.

The Performance Products sector accounted for about a quarter of group profits and the segment continued to deliver growth in terms of order intake, revenue and profits, which were up £300K to £6.1M. Order intake for the year increased £3M to £46M. Activity for the performance products segment is currently based in the UK. In Defence, assembly of the Foxhound used by British forces continued with the successful delivery of the first two tranches of 300 vehicles. During the year, new orders from General Dynamics Land Systems took the total manufacturing commitment to date to 376 vehicles. In High Performance Vehicles, demand from McLaren for new engines for their supercars continued and a further order was received from Bugatti for an extension to the long standing contract to supply the dual clutch transmission for the Veryon supercar. In Motorsport, there were orders from Formula 1 customers, Super GT, GT3 and the Renault World Series. The positive growth in Technical Consulting in the Rail sector fed through to orders for Performance Products and a contract was completed to manufacture prototype units of Scomi’s monorail transmission

Excluding Ricardo-AEA, underlying operating profit in Technical Consulting increased by 7% and the contribution of Ricardo-AEA was £2.8M during the year. The existing UK technical consulting business had a strong year and despite a strategic partner taking certain work in-house, a good stream of new business was secured. The German business had a difficult year as demand softened and a key client here took some work in-house too. The business improved in the second half of the year, however, with some multi-year contract wins and tight cost controls improving performance. In the US, the business performed solidly in a difficult market. A number of small contracts wins were made with the “Detroit 3” and profits were underpinned by Defence and Passenger Car work.

Overall, this is a very positive update. Income was up across both operating segments and the net cash outflow of £3.7M was very impressive considering the net £14M spent on acquisitions and the £2M net reduction in debt. Indeed, there are now no loans at all at Ricardo and whilst net tangible assets fell by £9.3M, they are still a healthy £58.4M in total. Operationally things seem to be going well, particularly in the passenger car and rail sectors but commercial vehicles and the German office don’t seem to be doing so well. It would be nice to see some major new contracts in the Performance Product business to cover the end of the Foxhound production cycle though and the dependence on two very large customers is a slight concern.

The group currently has a net cash position of £6.1M, which was £1.8M worse than at the same period of last year but considering the net £14M on new acquisitions, there is actually a very strong underlying position here indeed. Current P/E ratio is a hefty 18.2 (16.7 on an underlying basis) but it is predicted to fall to 15.6 next year, which is not so expensive considering the strong underlying performance of the company and lack of debt. The yield at the current share price is 2.3%, which is decent but not stellar. It is fairly well covered, though (2.3 times). Having bought a few more of these shares after the last update I am continuing to hold.

On 14th November, Ricardo released an interim management statement covering the first four months of the year. Order intake was up 17% and 6% excluding the acquired Ricardo AEA. The order book closed 6% up on the level at the end of the June and contained a good mix of business. Significant orders included a further order for monorail transmissions for a second installation in Brazil; a motorcycle project for a customer in Asia; a further DARPA order for the US defence sector; and passenger car content in the UK, US and Asia. Another exciting new announcement was that the group was selected to partner with Thailand’s Defence Technology Institute on the development of its Black Widow Spider 8×8 armored vehicle programme.

The UK business performed well during the period but the German and US businesses continued to face a challenging market backdrop with a performance similar to last year but below historic levels. Strategic Consulting and Ricardo AEA contined to perform in line with expectations. Looking forward, the group has a strong order pipeline with opportunities including a European motorcycle programme; further power generating activity in Europe and Asia; two multi-year assembly projects for supercar manufacturers; passenger car, defence and commercial vehicle opportunities in the US and a decent number of passenger car programmes in China and Japan. Overall, this is a good update. The business seems to be doing well and there are a number of interesting projects in the pipeline.

On the same day, the group announced that Chairman Michael Harper would be retiring at the AGM next year. It has been decided that Terry Morgan will join the board as deputy chairman at the start of next year with a view to him succeeding Michael when he steps down. Terry is currently Chairman of Crossrail Ltd and the Manufacturing Technology Centre for Railway Engineering. It is good to see such an orderly succession plan in place here, which is rather unlike many other companies. This is a great company currently and I will look to top up on any macroeconomic falls.

On 20th December the group announced that they had signed a contract with McLaren to supply engines from their Shoreham facility to 2020, worth £40M a year. This is the largest order that Ricardo have ever received and although they already have a strong relationship with McLaren, this will had a substantial amount of earnings for the group and I have added a few more here.

On 16th January, the group announced a trading update covering the first half of the year. It was stated that since the last update, business performance continued in line with expectations and they gained contract wins in both Technical Consulting and Performance Products. These wins include a European motorcycle programme, further power generation activity in Europe, further government consultancy, and passenger car programmes in the US, China, Japan and the UK. It is particularly pleasing to see new orders for the previously struggling German and US offices. Overall a good update.