Tristel has now released their full year results for 2013.

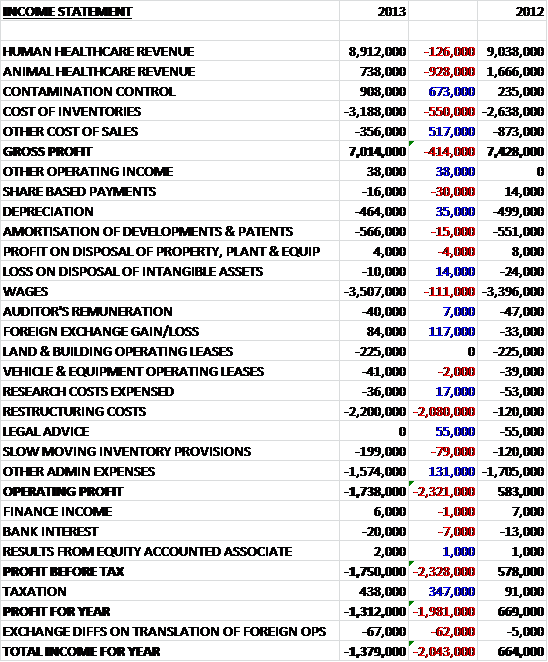

Falling revenues in Human Healthcare and Animal Healthcare were partially mitigated by a hike in Contamination Control revenue. During the year the agreement with the distributor in the Animal Healthcare segment was terminated and the group sold direct to the customer. One consequence of this was that some of the sales that used to go through the distributor were actually found to be going into the other two segments and the Animal Healthcare revenue reductions show this. Costs of sales were also marginally higher to give a gross profit of £7M, which was £400K lower than last year. Wages were £111K higher during the year and remain the largest single cost but this year also saw a £2.2M restructuring charge which drove last year’s operating profit to a £1.7M operating loss. The restructuring costs included costs involved in reducing headcount and impairments to assets after a review of the balance sheet, so they are mostly non-cash items. At least there was a tax rebate on the (mainly) non-cash losses so the loss for the year was just under £2M worse off at £1.3M.

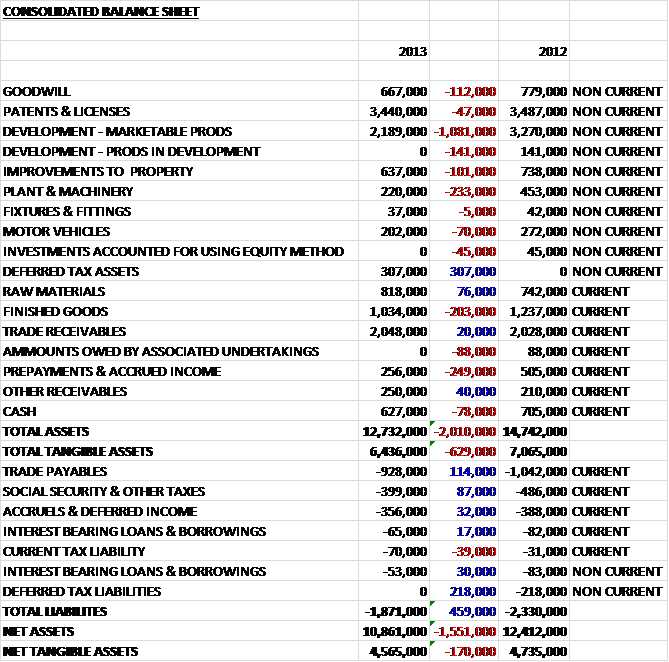

Assets at the year-end were down just over £2M to £12.7M with almost all individual assets suffering a decrease. The largest fall was the reduction in the intangible development assets which declined by more than £1M and relates to Stella disinfectant wipes as the recoverable value of sales was deemed to be less than the asset value on the balance sheet resulting in impairments. Due to the loss making year, the only asset to substantially increase is £307K of deferred tax asset. Liabilities, however, also declined during the year with the wipe-out of the £218K deferred tax liability and the £114K reduction in payables being the biggest fallers. This meant that liabilities were down £459K and net tangible assets had a small reduction of £170K to £4.6M.

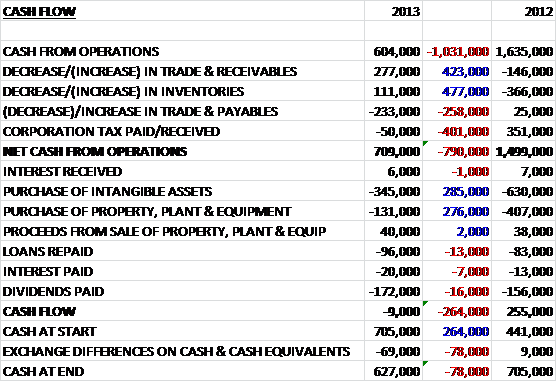

The cash profits for the year collapsed by over £1M to be just £604K. There was a favourable movement in working capital, however, with a decrease in receivables and inventories not being fully mitigated by a decrease in payables. Corporation tax was £50K to leave the net cash from operations at £709K, less than half the figure last year. A lot less was spent on capital expenditure this time and after a loan repayment of £96K and £172K of dividend spend, the cash outflow was only £9K, £264K worse off than last time but considering the poor profit levels, the increased loan payments and the small hike in dividend, this is actually quite a good cash flow, mainly due to the reduced capital expenditure.

During the year a provision was made against certain inventories against slow moving and obsolete stock with £204K being taken off the value of Tristel Stella equipment and £206K taken off Shine equipment. It was also mentioned that the amount owed to the group by Tristel Italia was considered doubtful and provided against (this is another component of the non-recurring items). It is not clear why the receivables are considered doubtful and whether the associate will continue trading with Tristel – a little more information about this would have been useful. Tristel continues to pay royalties to the company belonging to one of their directors, Bruce Green which I still find a little uneasy about.

The main issue that has faced Tristel during the past year is the collapse of the legacy Endoscopy sales that have had to be replaced by new products. During the year, the group has worked hard to make sure these products were available and to get the overseas offices to become cash generative. This has generally happened and the results this year have been characterised by a poor first half of the year followed by a decent performance in the second half as management seem to have been caught out by the severity of the fall-off in endoscopy sales which more than halved during the period.

Another major issue has been the termination of manufacturing for the distributor (Medichem) of the animal healthcare products. The group now sell their own brand to the market, which is named Anistel. This has led to higher margins but they have found it difficult to market these products directly as they are outside the traditional products that Tristel sell. There seems to be some traction being made as 16 overseas distributors have now switched over to Tristel and 2014 should be a little better for this product. The Crystel range has been selling more slowly than was anticipated but client wins in industry and NHS aseptic units have given rise to a 286% increase on last year’s sales. Sales for next year are expected to substantially increase.

By far the most profit is still currently made in the Human Healthcare segment but profits in the Contamination Control business is also on the up. Geographically about 2/3 of sales are made in the UK. There were a number of customers that made up a large proportion of revenues, with the largest accounting for 19.4% although this has reduced from 33.2% last year so some progress seems to have been made in diversifying revenue sources.

The Wipes system is used to decontaminate nasendoscopes, cardiology and ultrasound probes. They have been approved for use by the Australian regulatory body and the Chinese Ministry of Health and are recognised by many professional bodies. Sales from overseas offices (New Zealand, China, Hong Kong and Germany) increased by £600K year on year. Tristel NZ sells the Stella decontamination system and supplies the New Zealand and Australian hospital infection control market, sales more than doubled to £735K. The Chinese subsidiary sells the wipes system, Stella and Fuse, the surfaces range. Sales here fell by 42% to £305K but the restructuring work undertaken at this office meant the business was cash break-even. The German office serves the hospital infection prevention market and sales here nearly trebled to £623K. The Russian branch is still in formation and no activity has yet started there.

In the instruments sector, Multi channelled endoscopy fell by more than half but this was counteracted by a small increase in UK Single Lumened endoscopy and a £500K increase in sales of overseas singles lumened endoscopy. The board feel that they are some way off reaching market saturation point and that women’s health and ophthalmology offer particularly good growth prospects and it is expected sales will continue to grow strongly. Sales of surface products increased by less than 1% with an increase in UK sales being mitigated by a 5% fall in overseas sales. It is anticipated that the upward momentum in sales will be restored next year. In the Water sector, Tristel is the exclusive European distributor of Bio-Cide products used to control the Legionella bacterium. This agreement was renewed for 20 years in 2008. Sales of these products were down £64K and fell both in the UK and in export markets – this sector is not considered a growth opportunity but a consistent stream of cash.

Revenues overall were down on last year due to the fall-off of the legacy endoscopy product and the termination of the distributer agreement for animal healthcare. There was a £1.75M loss before tax but considering there was a one-off charge of £2.2M, this indicates that the group would have made a similar amount of profit to last year without these charges. Nat tangibles nudged down due to impairments of some plant and machinery and certain inventory. There was a small cash outflow which was kept low due to reduced capital expenditure. Apart from the endoscopy products, the other products seem to be gaining traction and the board have a rather bullish view of next year’s prospects (although this is not the first time I have heard this). Although the group made a loss this year, things do seem to be looking up for next year but the future P/E ratio is predicted to be 17.2 according to analysts, which seems a bit pricey for the moment. The current dividend yield is 1.2%, which is not that stellar either so I am reluctant to rely on forward looking management statement so I do not see these as a buy at the moment.

On the 10th December the group released an AGM statement. It was noted that the strong trading had continued and in the first half of the year revenues were up by 36% to more than £6M and profit will come in at £600K, which is £100K above the profit for the whole of last year. They have seen growth from all areas of the business and there was a significant increase in sales of Tristel wipes. It was also noted that the pattern of growth should continue into the second half and full year results are likely to be ahead of market expectations. It does seem that Tristel has turned a corner and I have topped up with some more shares.

On 22nd January the group released a trading update covering the first half of the year. They reported that they had enjoyed a strong first half and that a better than expected December has led to a performance ahead of expectations. Revenue will be in excess of £6.4M, pre tax profit will be more than £700K and the group is now in a net cash position. Particular growth was seen in sales of products used to disinfect non & single lumened instruments, hospital surfaces and within aseptic units. Overall, a very reassuring statement.