![]()

Ricardo has now released its full year results for 2012. As usual I will start the analysis with the Income statement.

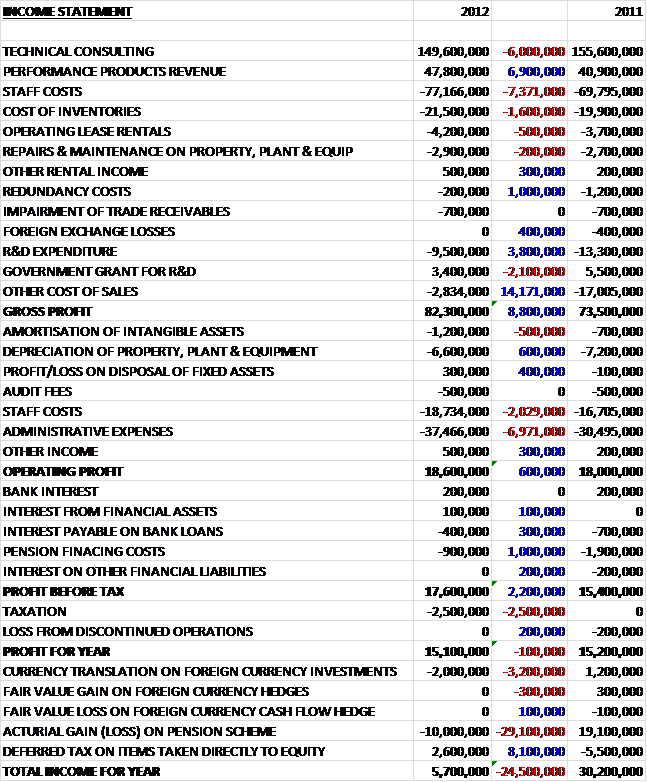

The profit for the year of £15.1M was virtually unchanged on the profit for last year. The reporting segments seem to have changed from last year but we can see that total income was not much different either, with increased revenues from performance product sales counteracting the reduction in technical consulting revenue (blamed on tough conditions in the US). Cost of sales, however, fell quite a bit partly due to reduced R&D expenditure to leave the Gross profit some £8.2M higher than last year at £82.3M.

Admin expenses increased, partly driven by higher staff costs where the group is strengthening the business development department and giving bonuses to a wider range of staff, which caused the operating profit to be just £600K higher than last year. Next we see less money spent on finance considerations, with less being spent on pensions in particular counteracted by a much higher taxation level (it was zero in 2011) due to a reduction in the R&D credit received from the Government, which gives us the static profit after tax levels mentioned above. Unfortunately a huge acturial loss on the pension scheme caused the total income for the year to be £24.5M lower at £5.7M.

Next the balance sheet analysis:

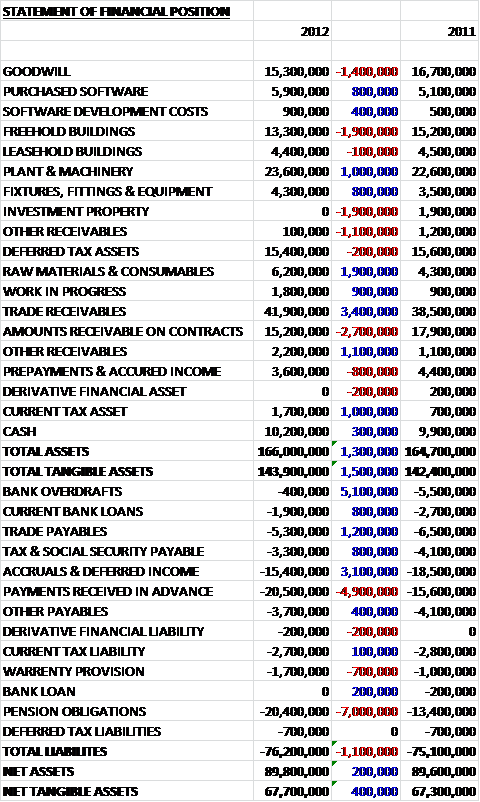

Much like the profit for the year, the net assets have hardly changed when compared to last year. The assets themselves were £1.3M up from 2011 at £166M, which can be mainly attributable to an increase in the value of inventories. Likewise, liabilities were £1.1M higher where reductions in bank loans and overdrafts were more than counteracted by a £7M increase in pension obligations.

Of those trade receivables, £12M were overdue, compared to £13.3M last year, £1M of which were over 180 days overdue (£0.7M in 2011). Ricardo is currently struggling somewhat with its pension scheme. Currently it covers 81% of the needed amount and £4.3M was added this year to cover the deficit, which is now £20.4M. The group hope to eliminate this deficit by 2016.

Moving on to the cash flow statement:

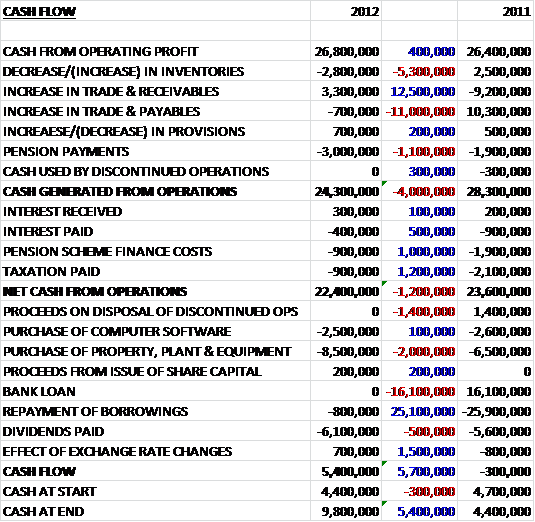

On the face of it a positive cash inflow of £5.4M in they year was fairly decent when compared to a negligible cash outflow last year. Let’s delve a bit deeper into those numbers. The cash received from profit was on a par with last year at £26.8M but there was £5M more tied up in inventories than in 2011 and a tighter control on receivables counteracted rather less money put towards payables suggesting that perhaps the order process has been streamlined or the group currently has less business. So, the differences in working capital pretty much cancelled each other out but a £3M payment into the pension pot means that the cash from operations was £24.3M, £4M lower than 2011.

More cash was paid out in finance costs, but quite a bit less than last year so the net cash from operations was just £1.2M down on last year at £22.4M. There was slightly more spent on capital expenditure than last year but the real difference was the lack of new borrowing and no major payback of money owed in loans. A one off receipt of £1.4M was received in 2011 from the sale of a discontinued operation (the German exhaust business). In the coming year, more cash should be raised by the proposed sale and leaseback of the German office.

So, although it is pleasing to see a positive cash generation, if the net repayments of the bank loans and the one off costs were striped out, the cash flow is slightly less than it would have been last year.

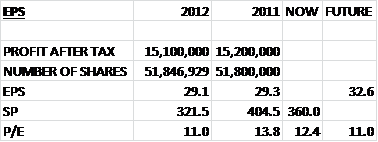

An EPS this year of 29.1 is very similar to that of last year and on the share price at the time of writing, the P/E ratio is given as 12.4 which is not that taxing. Future EPS is predicted to be 32.6 next year and if this was the case, the P/E of 11 seems pretty good value.

| ORDERS BY SECTOR |

2012 |

|

| CLEAN ENERGY & POWER GENERATION |

7,490,000 |

7% |

| DEFENCE |

11,770,000 |

11% |

| AGRIC & INDUSTRIAL VEHICLES |

7,490,000 |

7% |

| RAIL |

1,070,000 |

1% |

| MARINE |

2,140,000 |

2% |

| COMMERCIAL VEHICLES |

7,490,000 |

7% |

| HIGH PERFORMANCE VEHICLES & MOTORSPORT |

23,540,000 |

22% |

| PASSENGER CAR |

43,870,000 |

41% |

| GOVERNMENT |

2,140,000 |

2% |

| TOTAL |

107,000,000 |

I thought it would be interesting to analyse the future order book and from this we see that the vast majority of Ricardo’s orders are for motor vehicle projects – either everyday vehicles or motorsport. The work that the group does for the likes of McLaren is not just prestigious but actually makes up quite a lot of the orders. The clean energy and power generation is mostly related to Wind turbines but the group are also securing work in the tidal power sector. The order book value of £107M is exactly the same as that of last year.

| ORDERS BY PRODUCT | ||

| ENGINES |

52,430,000 |

49% |

| DRIVELINE & TRANSMISSION SYSTEMS |

22,470,000 |

21% |

| VEHICLE SYSTEMS |

21,400,000 |

20% |

| HYBRID & ELECTRIC SYSTEMS |

4,280,000 |

4% |

| INTELLIGENT TRANSPORT SYSTEMS |

1,070,000 |

1% |

| STRATEGIC CONSULTING |

5,350,000 |

5% |

| TOTAL |

107,000,000 |

Similarly here is a list of orders by product and almost half of the orders are for Engines which clearly makes up a very important part of what Ricardo do.

This year, Ricardo has entered into a contract with David Brown Gear Systems in offshore wind to design the turbine gearbox. In the rail sector, they have undertaken a collaboration with Scomi Rail in Malaysia designing drivelines for Monorail and Metro systems. In the UK, they have a contract with LH Group investigating upgrades for the power systems of diesel trains and the DTI have also commissioned Ricardo to study fuel efficiency in diesel trains.

In the automotive sector, Ricardo have already delivered 1500 engines to McLaren and make the full transmission and driveline system for the Bugatti Veyron. The group also continued to supply transmission products to all leading manufacturers in the Japanese Super GT championships and designed the engine and transmission for the BWM K1600 motorcycle. The group have also worked with Petronas to develop a new turbo charged spray guided gasoline combustion system and an auto train convoy where cars are able to drive in a “train” on the road automatically (with Volvo) and are heavily involved in the development of the engine for the Chevrolet Beat’s entry to the Indian market. Ricardo also do a lot of work for Jaguar Landrover.

In aerospace, they work for IAI on a semi-autonomous aircraft taxi system which will create a significant reduction in the use of aircraft fuel (a lot of fuel burned by planes is actually done on the ground). In defence, the group continue to supply Foxhound vehicles to the UK MOD and they are now active in Afganistan.

Although the group does have a diverse array of projects and clients, there are five that account for about 10% of revenues each. One Technical consulting customer accounted for £31.4M in the year and another client accounted for £26.8M so if one of these were to be lost, there would be a bit of an issue.

During the year, most of the revenue was earned in the UK, and this was an increasing market. Other territories have rather disappointingly fallen, however. The group have formed Ricardo Asia to help expand there and they have already gained contracts in Malaysia, China and Korea. Germany and the EU have been difficult markets. New orders have been received but activity is generally subdued which Ricardo blame on the Eurozone issues. The US is down due to a slow start but the group received a strong defence order late in the year. Strategic consulting in general has been tough as customers cut back on discretionary spend and focus more on operations consulting.

Overall then this year has been a quiet one for Ricardo. The profit and revenues have been flat – albeit with a shift from consulting revenues to performance products and the strong UK market is masking difficulties in the EU and the States. Admin expenses are up slightly as the group concentrates on strengthening their business development, including a new office in Asia to concentrate on the market there.

Ricardo has a strong net asset base and along with a net cash position of £7.9M, this gives a very comfortable contingency and there is a positive cash flow here too. The current P/E of 12.4 is not bargain basement but I think it offers good value at the current share price. The dividend yield is 3.4% which is decent rather than spectacular and is covered 2.4 times. Also, I just like their products and what they do which helps on a personal level.

In the future as fuel emission regulation becomes more and more important, there should be plenty of opportunity for Ricardo. I see this as a fairly decent if unspectacular share and will hold onto the shares that I have.

In early November, Ricardo announced that they had completed the acquisition of AEA Europe for a cash price of £18M. AEA Europe was an environmental consultancy providing services to the UK public sector and the EC along with some private organisations. Along with the acquisition come 400 UK based members of staff.

The intention is to leverage Ricardo’s international network and AEA’s government agency contracts. While I can see that the businesses are very complimentary and Ricardo can afford an acquisition of this size, I am a little surprised they are moving further into the consultancy sector given in the statement above they noted how the discretionary nature of consulting has meant hard times in recession hit Europe. Also, the fact that AEA is UK and European based does not really allow Ricardo access to that many new markets. Overall then, I am not convinced by the value of this acquisition strategically but remain a holder as I still like the group as a whole.

On the 15th November, the group released an interim management statement covering the first four months of the year. The order book value is at a very similar amount to the end of the year (£108M). I am not sure if this included the recent acquisition or not (I hope not). Revenue for the group is up an encouraging 8% on the first four months of last year. Within technical consulting there is a mixed bag. The UK remains strong and the large defence project from the US has bolstered things there but a key German client has taken their consulting in-house which is a bit of a blow. Performance products continue to be strong, underpinned by defence, supercar engines and transmissions.

Overall not a bad update – the increase in revenue is encouraging but I will wait and see how the acquisition beds in before buying more I think. Remains a hold for me.

On the 4th December, a trading update was released. Within Technical Consulting, a good amount of new work has been secured in the UK and Japan, and there continues to be a good pipeline of work in China. However, the market in mainland Europe has continued to be difficult where work from an engine client and a Chinese motorcycle manufacturer has offset the reduction in revenues experienced in Germany. The US division retained a strong order book,

The Performance Products business continues to be busy, particularly in Motorsport, where more orders have been received from Bugatti. Other large projects include the defence vehicles and the Malaysian rail program. The acquisition, although still early days, is apparently delivering as expected and despite the acquisition, the group closed the end of December with only a marginal net debt balance.

A fairly decent update then, the reduction in German business is a shame but it is good to see sales in Asia improving. Still a hold for me.