Ricardo has now released its interim results for the year ending 2016.

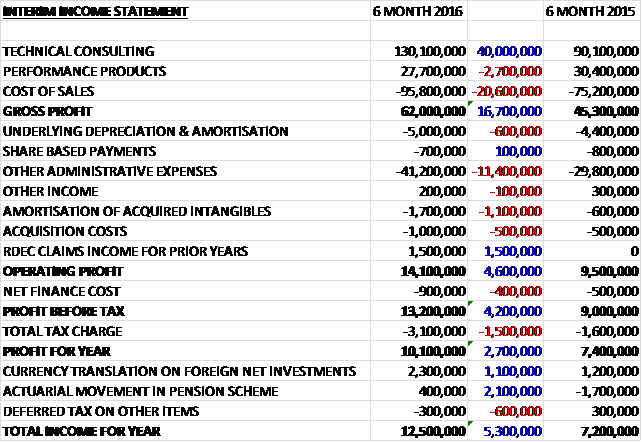

Revenues grew when compared to the first half of last year as a £2.7M decline in performance products revenue was more than offset by a £40M growth in technical consulting revenue with £25.5M of this coming from acquisitions. Cost of sales also increased to give a gross profit £16.7M above that of last time. Depreciation and amortisation increased by £600K and other admin expenses grew by £11.4M with a £1.1M growth in the amortisation of acquired intangibles and a £500K increase in acquisition costs being offset by a £1.5M RDEC claims income relating to prior years. This gave an operating profit some £4.6M above that of the first half of 2015. Finance costs grew by £400K due to higher borrowings and tax was up £1.5M due to the changes in the R&D tax allowance to operating profit, which meant that the profit for the first half of the year came in at £10.1M, a growth of £2.7M year on year.

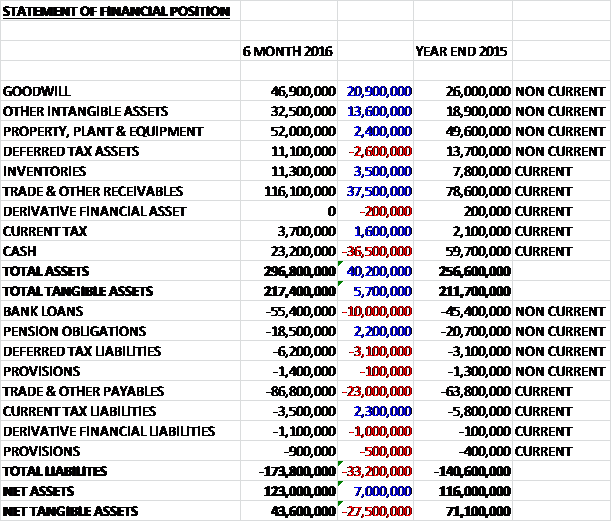

When compared to the end point of last year, total assets increased by £40.2M driven by a £37.5M growth in receivables, a £20.9M increase in goodwill, a £13.6M increase in other intangible assets, a £3.5M growth in inventories and a £2.4M increase in property, plant and equipment was partially offset by a £36.5M decline in cash and a £2.6M reduction in deferred tax assets. Total liabilities also increased during the period as a £23M growth in payables, a £10M increase in bank loans and a £3.1M growth in deferred tax liabilities were partially offset by a £2.3M reduction in current tax liabilities and a £2.2M decline in pension obligations due entirely to the £2.2M cash contributions paid into the scheme. Overall the net tangible asset level was £43.6M, a decrease of £27.5M over the past six months.

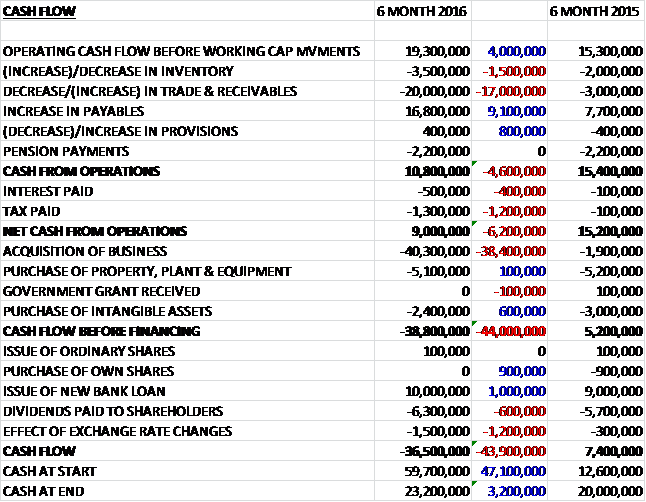

Before movements in working capital, cash profits increased by £4M to £19.3M. There was a cash outflow though working capital, with an increase in inventories and a particularly large growth in receivables which meant that after a £400K increase in interest paid and a £1.2M growth in tax paid the net cash from operations came in at £9M, a decline of £6.2M year on yea. The group spent £5.1M on property, plant and equipment along with £2.4M on intangible assets but the £40.3M spent on acquisitions meant that before financing there was a cash outflow of £38.8M. The group received £10M of new loans and after a £6.3M payment of dividends there was a cash outflow of £36.5M for the period and a cash level of £23.2M at the period-end.

The underlying operating profit in the Technical Consulting business was £10.5M, a growth of £3.6M when compared to the first half of last year with £1.6M of this coming from the acquisitions. The European technical consulting division was a key driver of profit generation with profits growing significantly as a result of an internal reorganisation undertaken at the end of the prior period to reduce costs. The performance of the US business improved on its result in the first half of last year whilst maintaining an encouraging order pipeline as they enter the second half. In Asia they continue to grow their activities and enter the second half with a stronger order book too. The environmental consulting business has performed as expected and is reducing its reliance on the public sector where ongoing price cuts are being experienced.

In Automotive the group experienced increasing levels of activity in their major markets. Fuel economy, alternative fuels and CO2 reduction remain top global industry priorities. The group have secured a range of large multi-year programmes in vehicle systems, hybrid and electric systems and the core powertrain areas of their business, focused on both new and existing product upgrades. Vehicle lightweighting remains an area of growth and they continue to invest in advanced combustion and other key technologies in areas related to improvements in overall vehicle efficiency such as intelligent driveline and electrification. The future of mobility solutions including connected and autonomous vehicle technology in particular, is attracting significant interest in North America.

The rail business has grown significantly with the acquisition of LR Rail. Integration activities are progressing well and they have won significant levels of new business in the UK, the Netherlands and Asia. The largest win was for a multi-year rail project for the independent validation and verification of a transit railway in Asia. The order book remains very strong and the business also saw its “PanMon” pantograph monitoring systems formally approved by the Network Rail for use across the UK national rail network.

In Commercial Vehicles, the group has secured a number of large engine and transmission projects across the medium and heavy duty sectors and continue to see strong interest across Asia, in particular. The future pipeline is based around a broad mix of largely engine and transmission opportunities. In the US, greenhouse gas and low NOx standards are driving interest in powertrain and trailer efficiency, emissions control and use of alternative fuels.

Growth in the environmental consulting business is focused on private sector and international expansion. Key practice areas are energy and climate change, air quality, resources and waste, sustainable transport, chemical risk and water. The recent additions through acquisitions have provided further opportunities for growth into the electricity networks and water sectors. In power generation the focus remains on growing large scale generator sets business and across the renewables sector, they continue to pursue a range of opportunities in offshore wind, tidal and energy storage applications.

In Defence, the group established Ricardo Defence Systems in the US last year which is enabling them to deliver US classified projects and expand the range of opportunities that they can pursue across future land platforms. In the UK, they have broadened their network within the MOD and have continued to grow key relationships with defence contractors and in Asia they have secured a contract to design a new defence vehicle. The off-highway market is currently very challenging as a number of large OEMs are managing business cost reduction programmes in response to global challenges in the mining, construction and agriculture markets.

The underlying operating profit in the Performance Products business was £2.8M, a decline of £900K year on year which was as expected. The result in the current period was driven principally by two key programmes being in a transitional phase as customers prepare to launch new products into the market. The expansion of the engine build facility is now complete which enables a doubling of capacity and the capability to deal with increased engine variants. Production of engines for the 650S, 675LT and the McLaren P1 supercar continue in line with expectations and full production of engines for the new 570S has been added.

The group remains a key supplier to the motorsport sector having commenced deliveries for two new GT3 clients and an R5 Rally works team. They also continue to manufacture for Formula 1 and products such as the transmissions for the Japanese Super Formula 14, Indy Lights and the Renault World Series. Production continues for the Porsche Cup and Bugatti transmissions in line with the long term supply agreements. In Defence, as part of a teaming agreement with a leading defence Tier 1, the group has developed and provided retrofit kits for the Cougar family of vehicles for the MOD.

The closing order book grew from £140M this time last year to £201M at the end of the first half of this year, of which £55M was acquired with the LR Rail and Cascade businesses, resulting in a 4% increase in the order book on a like for like basis.

During the period the group made two acquisitions. In July they acquired the Lloyds Register Rail business of Lloyd’s Register. LR rail is a rail consultancy and assurance business and is a partner to a wide range of international clients with services ranging from rolling stock design, signalling and train control, intelligent rail systems, operational efficiency improvement, training and independent assurance services. The initial cash consideration was £40.6M and the acquisition generated goodwill of £17.7M. As part of the acquisition, the group agreed to acquire the interests of a joint venture operation in China for £1.9M but the completion has been delayed and completion is expected in March 2016. The business generated an underlying operating profit of £1.4M during the period.

In August the group acquired Cascade Consulting for a total cash consideration of £3.2M. Cascade is an environmental consultancy business specialising in the UK water sector which provides additional capability and reach in water resource management, ecosystem services and environmental impact assessment. The acquisition generated goodwill of £2.3M and generated profits of 200K during the period.

In 2013, legislation was enacted to allow UK companies to elect for the Research and Development Expenditure Credit on qualifying expenditure incurred since April 2013, instead of the existing super-deduction rules which will be abolished from April 2016. Management has decided to adopt the RDEC regime as of July 2015 which also allows claims to be made on qualifying expenditure under RDEC in excess of the tax relief received under the legacy scheme since July 2013. The credit relating to claims made for the excess in RDEC over the tax relief received under the legacy scheme in prior years is recorded as other income as it is non-recurring. In previous periods the tax relief received under the legacy scheme was recorded as a reduction in the income tax expense. In short, the R&D credit is no longer a tax incentive that benefits the tax line but is instead treated as grant income within operating profit to offset R&D expenditure.

During the period Laurie Bowen joined the board as a non-executive director following the retirement of Hans-Joachim Schopf. Furthermore David Hall stepped down from the board at the AGM as a non-executive director after nine years in the role and Malin Persson joined the board in January as a non-executive director. Going forward the group continue to trade in line with board expectations and they remain confident of further progress in the full year.

At the end of the period the group was in a net debt position of £32.2M compared to a net cash position of £11M at the same point of last year. At the current share price the shares are trading on a PE ratio of 22.2 falling to 18.6 on the full year consensus forecast. After a 9% increase in the interim dividend, the shares are yielding 1.9% which increases to 2% on the full year forecast.

Overall then this was a strong period for the group. Profits increased both organically and through acquisitions although net tangible assets did decline due to those acquisitions. The operating cash flow also fell but this was due to a large increase in receivables and cash profits grew year on year. There was a modest amount of free cash flow generated before acquisitions but not enough to cover the dividends, although I suppose this is a seasonal working capital issue.

The technical consulting division performed well, driven by the European business with all markets performing well apart from the public sector environmental market and the off-highway sector. The performance products division has a less successful period but this was due to two key programmes being in a transitional phase and was flagged up by management previously. There is a good order book, although the increase is mainly due to the acquisitions, of which LR Rail is the more material. It looks a bit expensive but seems to be contributing well. With a net debt position, a forward PE of 18.6 and dividend yield of 2% these shares are not cheap but this is a quality business that is performing well so the premium is probably justified and I continue to hold.

On the 19th May the group released a trading update for the first ten months of the year. During the period they have seen good revenue growth and profit is tracking in line with board expectations. Revenue was 32% higher than in the same period in the prior year and was up 9% on a like for like basis.

The Technical Consulting business continued to perform well. Within this segment, the European business is showing good growth following the integration of the operations in the UK and Germany in the prior year. The Rail and Energy businesses both continue to perform well and they continue to win a good level of work in Asia. In the US, trading continued to be difficult with reduced levels of work in Detroit and Chicago partially offset by increasing work in California.

In the Performance Products segment they now expect profits in the second half of the year to be lower than in the same period last year as increased volumes in respect of the new engine supply contract of McLaren are expected to be more than offset by lower one-off software license sales and a reduced level of high performance and monorail transmissions in the period.

Order intake in the period was £278M, which is £62M higher than the same period last year. On a like for like basis, order intake is £11M higher. The total order book at the end of April was £207M compared to £152M at the same point of last year. Overall the board remain confident of continued progress over the rest of the year and I am happy to continue holding.

On the 1st July the group announced that non-executive director Malin Persson purchased 1,500 shares at a value of £11.5K. This represents here maiden share purchase. It was also announced that Chairman Sir Terry Morgan purchased 5,000 shares at a value of £35K. Sir Terry now owns 15,000 shares in the company.

On the 5th July the group announced that it is acquiring the Italian motorcycle, urban mobility and industrial design and engineering business, Exnovo. This is a continuation of the relationship that has existed between the two businesses since February 2014 when a MoU was signed to jointly collaborate in pursuing major motorcycle business opportunities. This acquisition will significantly expand Ricardo’s full product development capability in the rapidly growing scooter, motorcycle and urban mobility market.

Based in Italy, the business has specialist styling, design, chassis, vehicle, electrical and prototype build expertise. It also brings complementary customer relationships in Asia and Southern Europe. The business has revenues of €3M and was acquired for an undisclosed sum and as such, it is rather difficult to analyse the acquisition!

On the 13th July the group announced that non-executive director Laurie Bowen purchased 4,000 shares at a value of £30.6K. This represents his first share purchase.

On the same day the group announced that it had received a £35M order to supply an advanced DCT for a new supercar. This multi-year order will see the performance products division supply an advanced dual clutch transmission that it has designed and developed in collaboration with a leading OEM for a luxury supercar that will enter production later in 2016. Deliveries of the new transmissions will start later this year and will continue over the life of the vehicle.

On the 19th July the group released a trading update where they stated that overall customer activity in the last two months has been positive leading to a strong year-end order book and a good pipeline across different segments. The board expect profit for the year to be in line with their expectations and the business is well positioned as it enters the new year.

The Brexit vote has clearly caused some uncertainty in the wider market but the board do not expect it to have any significant impact on their performance. The international spread of their customers and operations is helpful and they have had confirmation that the recently awarded EU research funding through the Horizon 2020 framework will remain in place.

The Lloyds Register and Casade acquisitions completed in the period have both performed in line with expectations.

Overall, this slew of information seems positive to me and I think these shares are now pretty decent value – I have bought back in here.