Safestyle has now released its final results for the year ending 2014.

When compared to last year, revenues increased by £11.2M and after cost of sales increased too, gross profits were some £4.5M higher than in 2013 at £49.7M. We then saw an increase in share based payments and other operating expenses relating to higher salary costs due to the annual pay award and auto enrolment; and marketing costs increased by £1.2M driven by inflation in TV advertising rates and an increased investment in digital marketing, more than offset by one-off costs relating to last year’s AIM listing and tax settlement so that operating profit increased by £7M which after finance costs and tax produced a profit for the year of £12.8M, pretty much double that of last year.

When compared to the end point of last year, total assets increased by £5.1M driven by a £3.2M increase in cash, a £921K growth in receivables and a £543K increase in property, plant and equipment. Conversely, liabilities fell during the year due to a £1M fall in payables to give a net tangible asset level of £6M, a decent £6.7M up on the negative value recorded last year.

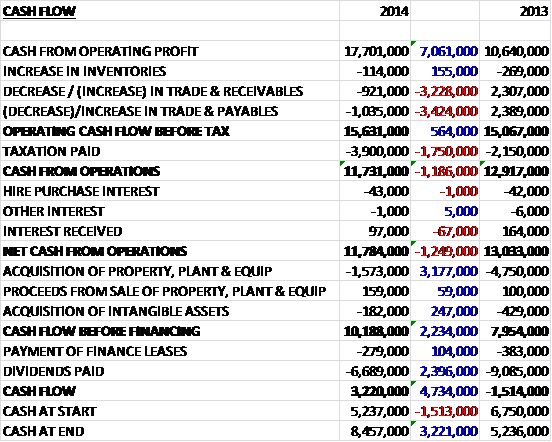

Before movements in working capital, cash profits increased by £7.1M to £17.7M before modestly adverse movements in payables and receivables meant that before tax, the operating cash flow increased by £564K to £15.6M which became £11.8M after tax and interest were taken into account. This was easily enough to cover capital expenditure so that free cash flow was an impressive £10.2M, an increase of £2.2M when compared to last year. The bulk of this cash was spent on dividends and there was still a cash inflow of £3.2M to give a cash pile of £8.5M – pretty impressive stuff.

The group has continued to increase market share, up from 7.85% last year to 8.48% in 2014 with the medium term target being 10%, and also maintained their position as the leading player in a fragmented replacement window and door market. The general economy and repair, maintenance and improvement market continues to recover which should be good for Safestyle as their geographic expansion into the South East and entry into the conservatory refurbishment market should lead to further growth. The overall market contracted 3.1% during the year with a 4.3% growth in the first half and a concerning 10% decline in the second half of the year. It is interesting, though, that Safestyle’s volumes increased 4.8% and 4.7% respectively during the year. It should be noted too that margins suffered in the second half of the year due to the cost of providing compulsory insurance backed guarantees to all customers and by the imposition of a 20% increase on the glass purchase price.

During the period the group carried out 57,682 installations, an increase of 4.7% on last year, consisting of 267,642 window and door frames. Average frame sales price increased by 1.6% to £504 and total average installed order value increased from £2,704 to £2,806. The focus on continued expansion into the South and South East resulted in sales growth of 17% in the region and the board believes there is scope for the group to gain further market share there. Two new sales branches were opened in Sittingbourne and Avon, both of which are performing well and a new branch has been opened in Watford with a further sales branch being planned for later in the year in Surrey. During the year, the group also opened a new installation depot in Crawley with a further depot planned for the Watford area in the new year.

The group has continued to grow its digital and internet presence and leads generated from direct response channels now account for 31% of all business and the increased focus on direct digital marketing should help the group grow market share and reduce average lead generation costs. During the year a significant investment was made to the Wombwell manufacturing facilities with an upgraded glass furnace, the installation of a new sash line and a new machining and cutting centre. Improvements in efficiency and quality have already been seen as a result of the investment. After a long period of flat prices, the group have made the decision to increase prices from the start of January 2015 to reflect some cost side price inflation, in particular glass prices; more stringent regulation and health & safety standards; and higher TV advertising costs. Despite the increase, the products apparently remain significantly cheaper than those of Safestyle’s national rivals.

During the year the group has conducted a feasibility study into the launch of a new product offering focused on the conservatory market and management have been encouraged by the initial feedback and as a result will begin the roll out of the new service across an initial eight sales branches in April. The service will focus on conservatory refurbishment where they will replace the roofs and frames of poorly performing conservatories onto existing bases. The roofs will be sources as complete units from an external manufacturer and the frames will be produced in the group’s own manufacturing facility. It is estimated that the refurbishment market totals about 20,000 conservatories a year with further growth expected to be driven by new glass and insulation technology that has vastly improved the energy efficiency of a traditional conservatory. The market is highly fragmented with little brand awareness so represents quite an opportunity and the board expect to be able to secure a similar percentage of the total conservatory refurbishment market to that which it has in the retail replacement market.

There does seem to be a large number of share options that have been granted with some four million outstanding at the end of the period with the only vesting conditions being that the individual must remain an employee of the group for a minimum period, so that may be something to take into account.

After introducing a price increase in January 2015 the first 11 weeks of the new year has seen a strong order intake, with the order book at the end of 2014 some 3% ahead of the previous year and trading in line with expectations. The CEO has hinted that an acquisition may be on the cards when he states “our robust cash generation and strong financial position enables the group to retain the flexibility to balance shareholder returns with the ability to take advantage of our leading position within a fragmented market should the opportunity arise”.

At the current share price the shares trade on a P/E ratio of 11.3 which seems pretty good value and this reduced to 10.4 on next year’s forecast. The shares also seem good value with regards to the dividend yield which is a fully covered 5.2% increasing to 5.3% on next year’s forecast. The group has a net cash position of £8.5M compared to a net cash position of £5.2M last year.

Overall then this seems like a good update. Profits improved even when the IPO costs of last year are discounted and net tangible assets are now positive after a good year of cash generation which has given rise to plenty of free cash to pay dividends. The operational cash flow was slightly lower than last year but this is only because tax increased and there were unfavourable movements in working capital. Operationally, there were increased installations, particularly in the South East and the average price per installation also improved. The 10% decline in the overall market in the second half of the year is slightly worrying and no real reason was given for this, although it has to be said that Safestyle’s sales did not suffer. There is also some pressure on costs with the glass price rising considerably during the year which has given rise to some price increases, so hopefully they will stick. Going forward, the order book seems decent and the continued expansion into the South East along with the conservatory refurbishment market seems quite exciting. The shares trade on a low P/E and there is an excellent dividend on offer so I am happy to hold despite the glass price inflation and may look to buy more funds permitting.

As Safestyle has now released its annual report I thought I would see if that gave any more information. Both the income statement and the balance sheet now have a bit more detail.

We can see that part of the increase in operating expenses was due to the £638K growth in operating leases and the £340K increase in share based payments, partially offset by a £562K decline in rent payable.

As far as the balance sheet is concerned, the increase in property, plant and equipment is entirely due to the assets under construction and the increase in receivables is across the board. The fall in payables is due mainly to the decline in tax and other payables. I suppose the most relevant piece of extra detail is the fact that there is £11.6M worth of operating leases on non-cancellable contracts which takes some of the shine off the fact the group are now net tangible asset positive. Overall though, my conclusions based on the prelim results are unchanged.

On the 21st May the group released an AGM statement. The year has started well with the company trading in line with expectations. Order intake for the first four months of the year grew by 2.7% year on year and the price increase introduced in January is helping to absorb the impact of glass price increases and regulatory costs. With the positive momentum in order uptake and continued opportunities to increase their geographic penetration, the board is confident that the group will deliver growth in revenue and profit through the year. This all sounds decent enough.

On the 16th July the group released a half year trading update. The company has continued to trade well with revenue during the first half of the year expected to be £74M, an increase of 6.8% year on year despite a strong comparator with Q1 2014. This increase reflects both further growth in market share and the price increases introduced in January. The board expects a continuing strong sales performance in the second half and remains confident of achieving full year results in line with their expectations.

Order intake grew by 7.1% during the period compared to FENSA statistics which show that the market contracted by over 10%. The group express surprise at this figure and personally I am very surprised. Are these stats reliable? Anyway, if that are it means that Safestyle enjoy a record 9.5% market share. Cash flow was strong during the half year and the group now has net cash of £14.9M compared to £10.8M at the same point of last year. Early evidence from the conservatory refurb business launched in April is encouraging but it is still early days.

All of this sounds very positive to me and I am thinking about adding to my position here.

On the 17th July it was announced that CEO Stephen Birmingham purchased 5,000 shares at a value of £11.8K giving him 3,893,889 shares representing 5% of the total issued share capital. It is always good to see director buying but this is quite a modest amount.