Safestyle has now released their interim results for the year ending 2017.

Revenue increased by £1.1M when compared to the first half of last year but cost of sales grew by £1.8M so the gross profit fell by £667K. There was no LTIP exercise charge, which was £947K last time but share based payments were up £56K, depreciation and amortisation grew by £229K and other operating expenses were £679K higher so the operating profit declined by £684K. Interest income fell by £37K and tax charges grew by £37K which gave a profit for the period of £6.9M, a decline of £756K year on year.

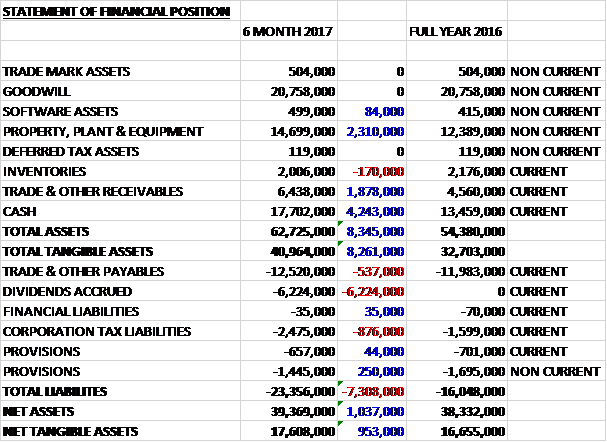

When compared to the end point of last year, total assets increased by £8.3M driven by a £2.3M growth in property, plant and equipment, a £4.2M increase in cash and a £1.9M growth in receivables. Total liabilities also increased during the year, mainly due to the £6.2M of accrued dividends. The end result was a net tangible asset level of £17.6M, a growth of £953K over the past six months.

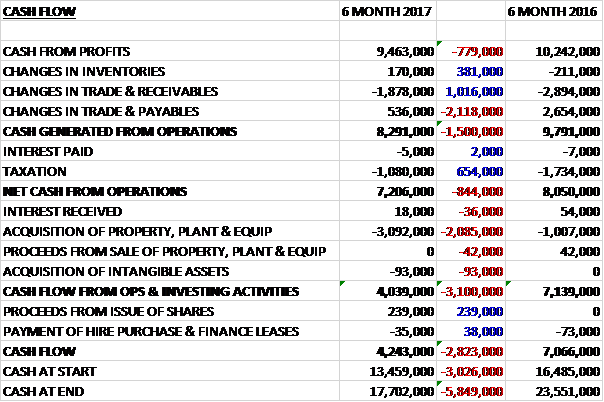

Before movements in working capital, cash profits declined by £779K to £9.5M. There was also a cash outflow from working capital but tax payments reduced by £654K to give a net cash from operations of £7.2M, a decline of £844K year on year. The group spent £3.1M on property, plant and equipment, of which £2.4M related to the new factory, along with just £93K on intangible assets to give a free cash flow of £4M. No dividends were paid but this doesn’t cover the £6.2M accrued. Due to the fact that the dividend payment wasn’t made in the period there was a cash flow of £4.2M and a cash level of £17.7M at the period-end.

Overall the volume of frames installed fell by 6.8% to 139,612 but the average unit sales price was up 6% to £599. The price list increase implemented at the start of the year to counterbalance the additional raw material costs resulting from the reduction in the value of Sterling has been secured and unit prices were further boosted by growth in higher value items including conservatory upgrades, composite doors and coloured frames.

The price list increase more than offset the inflation in raw material prices but other direct costs have also seen increases which has led to a reduction of the gross margin. In particular, online marketing costs have seen a significant increase with the cost of lead acquisition increasing by 19%, reflecting increased competition for leads in a tough market. In addition, manufacturing costs were higher as a result of the planned disruption during the transfer of equipment to the new factory, which won’t be repeated in the second half.

FENSA statistics show the rate of market decline in the period accelerated from a Q1 reduction of 2.4% to 17.2% in Q2 and the board believe that this steeper rate of decline has continued into the first two months of Q3. The response has been to protect revenues and gain market share which was up from 10.2% at the end of 2016 to 11.2%. This was achieved due to an increase in the cost of lead generation, reflected in the fall in profits, and order intake was up 1.8%.

The group have completed their factory extension at Wombwell on time and budget. It is now fully operational and they expect to deliver manufacturing productivity gains throughout the remainder of the year. With the investment in the factory now complete, they are announcing that they will start to buy back shares at a cost of up to £2.5M.

So far in H2 they have maintained their order intake in line with the previous year and have already started a number of initiatives to reduce their cost base. The expectation is that the market will continue to be weak for the rest of the year and consumer confidence has declined. They expect to continue to gain market share in H2 but sales will continue to be expensive to win and they expect operating margins to be challenging.

At the current share price the shares are trading on a PE ratio of 10.6 which rise to 12.7 on the full year consensus forecast. After the interim dividend was kept the same, the shares are yielding 5.6% which is expected to remain the same this year.

Overall then this has been a difficult period for the group. Profits are on the slide due to a poor market which means that leads are harder to come by. Net assets did improve but the operating cash flow fell with the free cash not covering the dividends. Volumes have declined but not as much as the market as a whole as the group is paying more in marketing to improve market share. The manufacturing costs should improve but otherwise the second half is looking just as bad as Q2, which was worse than Q1 meaning there is no immediate light at the end of the tunnel. With a forward PE of 12.7 and yield of 5.6% these offer decent value but the market really could go either way and I am not brave enough to jump back in until I see some signs of stabilisation.

On the 13th December the group released a trading update covering Q4. Since the last update, demand has weakened further and in the quarter sales have been 0.3% lower by value and 6.8% lower by volume than in the same period last year. For the first eleven months of the year, sales are 0.8% down.

With sales in December not helped by severe weather disruption to the planned installation programme, it is clear that Q4 sales will now be below expectations. At the same time, those sales have come at an increased cost of acquisition due to higher lead generation expense in a competitive landscape and a higher proportion being made on extended finance terms, negatively affecting margins. As a consequence, the full year outturn is now expected to be below current market expectations at around £15M.

The group continues to be cash generative and expects to have a cash balance of around £12M at the year-end. They also remain committed to the dividend policy. They are reviewing all costs and seeking operational efficiencies where they can and have already implemented savings across the business including a restructure of the sales and canvass function.

Looking ahead, the board expect market conditions to continue to be very challenging in 2018 so they have lowered their expectations for performance next year. The benefits of the cost saving programme will fall mainly in 2018 and should help mitigate the impact on profitability of any further fall in market demand so they expect modest earnings growth over this year.

It is clear that the market here is very difficult but as some point these shares might look cheap if one expects a pick up at some point and the current yield of 6.8% may act as a floor in the price. Tricky. I am staying clear until the dust settles at least.

On the 18th December the group announced that CEO Steve Birmingham sold 1,400,000 shares at a value of £2.2M. Apparently this is for personal financial reasons and he still owns 2,799,846 shares but the timing does not show a good vote of confidence.

On the 3rd January the group announced that CFO Mike Robinson sold 105,000 shares at a value of £175K. He now owns 211,499 shares – this does not look good!

On the 28th February the group released a trading update. The activities of an aggressive new market entrant have added to an already competitive landscape and impacted the group in certain areas of its operations. As a result the order intake in 2018 to date has been below expectations. The group has reviewed and reduced its cost base and carried out the planned restructure of its sales and canvass functions.

Guidance for 2017 remains unchanged but the board now expects group profit for 2018 to be materially below 2017 levels and below current market expectations. They continue to be cash generative and the board expect the benefits of their cost savings programme to take effect in the second half of 2018.