GVC has now released their interim results for the year ending 2017.

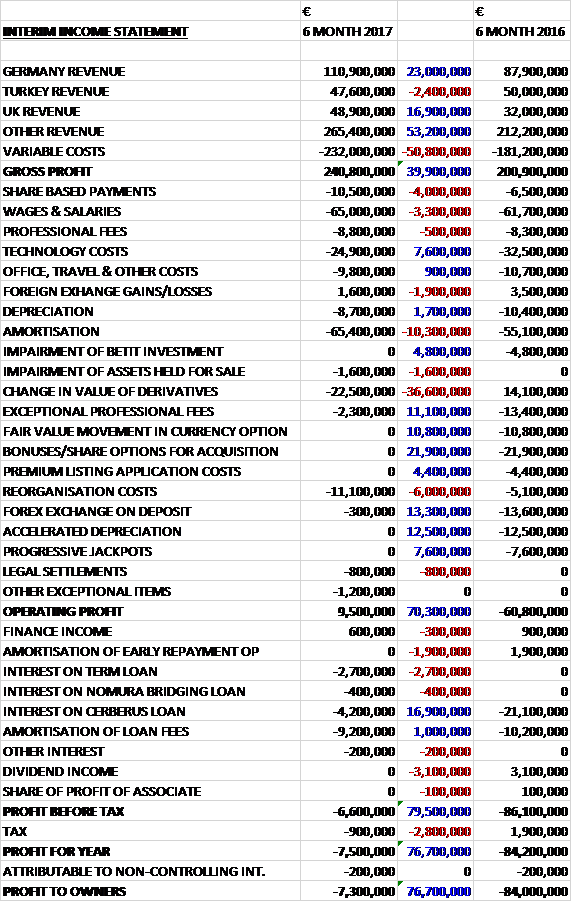

Revenues increased when compared to the first half of last year as a €2.4M decline in Turkish revenue was more than offset by a €23M growth in German revenue, a €16.9M increase in UK revenue and a €53.2M growth in other revenue. Variable costs also increased to give a gross profit €39.9M ahead. The already-substantial share based payments increased by €4M, wages and salaries were up €3.3M and amortisation increased by €10.3M but technology costs declined by €7.6M, no Betit impairment which was €4.8M last time, an €11.1M reduction in professional fees, a €13.3M fall in the cost of forex on the deposit and no fair value movement of the currency option, bonus share options relating to the acquisition, premium listing costs, accelerated depreciation or progressive jackpots. There was a €6M increase in reorganisation costs and a €36.6M detrimental movement in the value of derivatives, however, all of which gave a €70.3M positive swing to an operating profit. The interest on the Cerberus loan fell by €16.9M but there was €2.7M interest on the new term loan and no dividend income, which was €3.1M last time, and after tax charges grew by €2.8M the loss for the period was €7.3M, an improvement of €76.7M year on year.

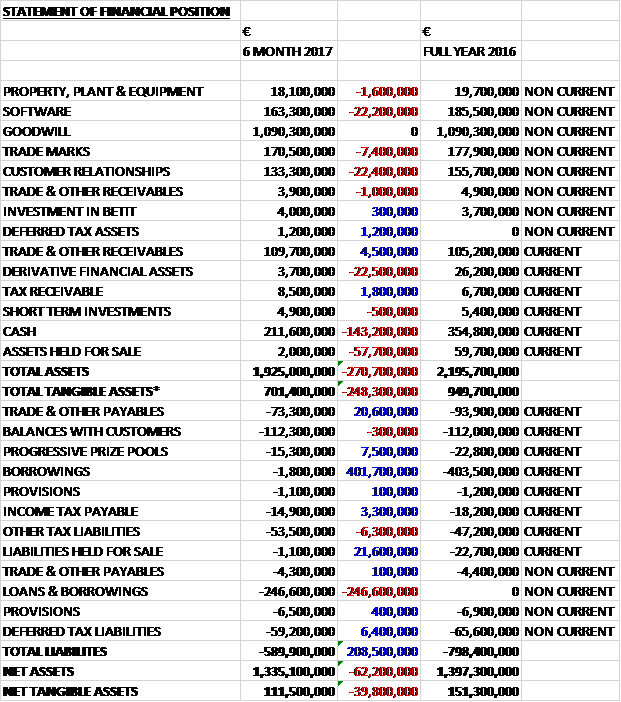

When compared to the end point of last year, total assets declined by €270.7M, driven by a €143.2M decrease in cash, a €57.7M fall in assets held for sale, a €22.5M decline in derivative financial assets, a €22.4M fall in customer relationships, and a €22.2M decrease in software. Total liabilities also decreased during the period due to a €155.1M fall in borrowings, a €20.6M decrease in payables and a €7.5M decrease in the progressive prize pool. The end result was a net tangible asset level of €111.5M, a decline of €39.8M over the past six months.

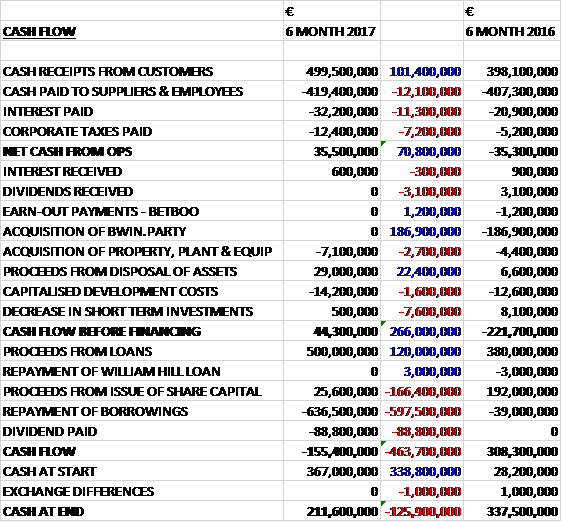

Cash receipts from customers increased by €101.4M and with cash paid to suppliers and employees increasing by only €12.1M, interest payments increasing by €11.3M, mainly due to the redemption of the Cerberus loan, and tax payments growing by €7.2M, there was a €70.8M growth in net cash from operations. The group spent €7.1M on property, plant and equipment along with €14.2M on development costs but they also received €29M in proceeds from the sale of assets to give a free cash flow of €44.3M. This was used to pay back a net €136.5M of borrowings and with €25.6M in proceeds from the issue of new share capital being more than offset by the €88.8M dividend payments, the cash outflow for the period was €155.4M and the cash level at the period-end was €211.6M.

The contribution from the Sports Brand business was €194.2M, an increase of €36.6M when compared to the first half of last year. The period saw a continuation of the positive momentum reported last year across all segments of the business despite the absence of a major football tournament. Amounts wagered were flat but the sports gross win margin increased from 9.1% to 9.8%, broadly in line with the expectations of a 10% long-term average. Sports NGR rose 6% to €172.2. Gaming NGR from sports brands continued to grow strongly, driven by improved product and more effective CRM as during the period gaming NGR rose 16% to €182.4M. Marketing spend as a percentage of NGR was 19% which is expected to rise in H2 as they return to more normalised levels of investment.

Looking ahead, they have continued to add new games content. Sports product development will be a particular focus going forward with a significant pipeline of enhancements. Their new tennis product was launched during the summer and this was well received by customers. They are now less than a year away from the World Cup in Russia and product development roadmaps are very much focused around the run up to this event.

August saw the launch of a new marketing campaign for the bwin brand. Early results are encouraging with new sign ups and first time deposit values up 113% and 98% respectively in the DACH region. The campaign in the regulated markets of Belgium, Italy and Spain have also worked well with FTDs rising by between 50% and 200%. The combination of an increasing number of new customers together with product enhancements should deliver material long-term benefits to the group.

The contribution from the Games brands business was €39.2M, a growth of €1M year on year after many years of decline. The strongest performance came from Party Poker, where NGR rose 32% whilst the value of deposits increased 48%. A combination of factors are behind this growth, including product development, increased marketing, localised market focus and improved player experience. The board expect to see the benefits of the increased investment in Party Poker on a contribution basis to come through in the second half of the year and Q3 has seen a further acceleration in deposit value and NGR growth.

Casino brands also achieved positive growth with Casino Club, Gioco Digitale and Party Casino all delivering improved top line performances. Casino Club continued to benefit from one of the most loyal customer bases in the industry, with more than two thirds of revenues coming from those that have been with the brand for five years or more. Deposits at Gioco Digitale grew strongly in the first half.

Bingo is the smallest product for the group and a deliberate decision was made to reduce marketing spend in the period. Accordingly, whilst revenue declined, profits increased. During the period Foxy was launched with actress Heather Graham and the second half started well with Cashcade returning to top line growth. Although there has been an improvement within Games brands, there is much more yet to come in terms of product and the overall customer experience. All the acquired bwin.party brands have been reinvigorated and further progress is expected in the second half of the year.

The contribution from the B2B business was €7.7M, an increase of €2.2M when compared to the first half of 2016. At the end of last year the group expended their relationship with MGM to launch new brands in the New Jersey online market, beyond the existing Borgata offering. A new MGM branded casino and poker offer was launched in August 2017. They continue to evaluate further B2B opportunities in the US as further states such as Pennsylvania look to regulate online gambling. In June they announced a partnership with one of Russia’s leading media group, Rambler Media, to launch a licenced online sports betting proposition. The group will provide technology and associated services, along with licensing the bwin brand to the venture. The new site is expected to go live before the end of the year. In addition, they continue to have an active pipeline of B2B opportunities.

The loss from the non-core business was €300K, an improvement of €100K year on year. Following the disposal of Kalixa in May, the division solely consists of Inter Trader, a financial spread betting and CFD business. Inter Trader revenues at constant currency grew 62% with last year being impacted by the migration to a new platform.

During the period around 68% of group NGR was derived from territories where they are licensed or currently pay gaming taxes. During the period, they withdrew their license application in the Czech Rep. They believe the opaque process falls someway short of being compliant with the principals of EU law. Poland also introduced new legislation in 2017, which creates an online casino monopoly, which in their opinion, is clearly contrary to EU law. In Germany, following elections, the state of Schleiswig-Holstein has said it will not ratify proposed amendments to the state gaming treaty that were proposed in November last year. They key amendment was the removal of the ceiling of the number of sports licenses but with no change to the inability to gain licenses for poker and casino. It is currently the only state in Germany that licenses all gaming verticals and is calling for other states to adopt this structure.

The Cerberus loan was repaid in January and an alternate bridge financing facility of €250M was provided by Nomura. All associated fees were charged to the income statement at this time including the remaining value of the early repayment option on the Cerberus loan of $22.5M. The bridging loan was then replaced with a long term institutional loan in March comprising of a €320M senior secured term and revolving facility, composed of a €250M term loan and a €70M revolving credit facility which was not drawn down during the period.

The group sold most of its digital payments company Kalixa in May. They realised an initial consideration of €29M together with deferred consideration of €2.6M which will be receivable in the second half of the year after paying down certain balances owing between the business groups. As a result of fees and other trading movements, an impairment charge of €1.1M was recorded prior to the disposal of the business. The remaining Kalixa business was disposed of after the period-end in August, realising consideration of €900K. An impairment charge of €500K was recorded during the period to reflect the net realisable value.

Going forward, the strong trading reported in the first half has continued into Q3. Daily group NGR is up 12% for the period up to 10th September and as a consequence of this, together with the performance achieved in the first half, the board now expects clean EBITDA for the current year to be comfortably ahead for the current forecast of €255.9M.

As the group made a loss last year there is no historic PE ratio but based on forecasts for the 2017 full year, they are on a forward PE of 27.6. At the current share price the shares are yielding 3.2% which increases to 3.5% on the full year forecast. At the period-end the group had a net debt position of €150.7M compared to €170.3M at the end of last year.

Overall then this was a decent period of progress for the group. Losses improved and the group only now seems to be loss making due to the change in the value of derivatives, net assets reduced but the operating cash flow improved with some free cash generated. The sports brands made good progress despite no football tournament this year with an increase in the win margin and the gaming NGR from sports brands also improved. Gaming Brands did fairly well, driven by improvements in Party Poker, and B2B also saw a decent performance.

As always, there are potential regulatory and licensing issues and the shares don’t look particularly cheap on a forward PE of 27.6 and yield of 3.5% but there seems to be good progress being made and I remain a holder.

On the 25th September the group announced that non-executive director Norbert Teufelberger sold 300K shares at a value of £2.5M.

On the 12th October the group released a trading update covering Q3. Group daily NGR was up 10%, sports brands daily NGR increased by 11% and games brands daily NGR was up 15% with B2B and non-core falling by 29%. This is a particularly good performance given the lack of any major football competitions.

Within sports brands, the gross win margin was 11.2%, ahead of expectations of the long term average of 10%. Daily wagers were 4% ahead at constant currency, reflecting the success of a new bwin marketing campaign launched in August.

Within games brands, Party Poker NGR grew by 48%, continuing to benefit from product improvement and increased marketing investment. Casino brands NGR also grew whilst bingo returned to underlying growth. The decline in B2B and non-core reflects the disposal of Kalixa in May. The group has also enjoyed a strong start to Q4. All of this sounds fine, I continue to hold.

On the 2nd November the group announced the sale of the Turkish facing operations to Ropso Malta for a performance related earn-out consideration of up to €150M in cash, receivable on a monthly basis over a five year period. The business generated €35M of EBITDA last year and had gross assets of €21M.

The decision to sell the business has been taken against a backdrop where the board concluded it is now appropriate for the group to focus on regulated markets and following the disposal the group will earn around 75% of its NGR from regulated markets.

The strong start to the quarter continued and daily NGR was 26% ahead of the same period last year, boosted by an exceptionally high sports gross win margin and a positive response to new marketing campaigns.

On the 3rd November the group announced that a non-executive director sold 400,000 shares at a value of £3.8M. He now owns 755,276 shares.

On the 7th December it was announced that the group had made an offer to Ladbrokes Coral for the entire share capital of the company. Ladbrokes shareholders would be entitled to 32.7p in cash and 0.141 GVC shares for each Ladbrokes share and a potential further value of up to 42.8p depending on the outcome of the current government review of Gaming Machines relating to the fixed odds betting terminals. The offer values Ladbrokes Coral at £3.1BN or £3.9BN depending on the outcome of the review. Kenneth Alexander would be CEO of the enlarged group.

The board believes that the transaction would be double digit EPS accretive from the first full year post-completion and following all reasonably expected outcomes of the Triennial Review.

On the 22nd December the group announced that they have reached agreement on the terms of an offer to acquire Ladbrokes Coral. Under the terms of the acquisition, for each Ladbrokes share, shareholders will be entitled to 32.7p in cash, 0.141 GVC shares and a contingent entitlement of up to a further 42.8p in principal value of loan note. The offer price values Ladbrokes Coral at around £3.2BN up to a contingent total of £4BN.

The enlarged group will be one of the largest listed sportsbook operators in the world by wagers and the largest listed online-led betting and gaming operator by revenue. It will have top three market positions in the UK, Germany and Italy plus a significant business in Australia and exposure to the US.

Cost and revenue synergies have been identified and the board believe the enlarged group will be able to achieve recurring annual pre-tax cost synergies of at least £100M. Around £7M will be achieved in the first calendar year, £33M in year two and £56M in the third year. The board believe that the acquisition will be double digit EPS accretive from the first full year.

This is a major acquisition and one that dramatically changes the nature of the group. I suspect they will probably make it work but I am thinking about selling out to concentrate my efforts elsewhere.

On the 11th January the group released a trading update covering Q4 and the year as a whole. NGR for the year is expected to be €1BN, a growth of 18% on an underlying basis. The board expects clean EBITDA to be at the top end of management expectations. The underlying NGR growth in Q4 was 31%, the strongest quarter since the Bwin acquisition.

Sports brands daily NGR grew 24% and on an underlying basis increased by 37%. The gross win margin in Q4 was 13.1%, significantly ahead of the expected long term average of 10% with daily sports NGR up 54% on an underlying basis. The well above average gross win margin meant that wagers were down 11% in the quarter but this was predominantly due to Turkey and wagers on an underling basis were just 1% lower. Sports brands gaming revenues rose 21% on an underling basis with the benefits of improved product and cross-sell continuing to be important factors.

Gaming brands daily NGR increased 24% and on an underlying basis was up 18%. All verticals put in a solid performance, with partypoker maintaining its impressive growth. B2B and non-core revenues grew by an underlying 4%, adjusting for Kalixa which was sold in the first of 2017.

Overall this all looks OK but I do wonder whether perhaps the group has reached the end of its journey now. It is certainly a very different beast to the one I invested in initially and I am considering taking profits.