Portmeirion has now released their interim results for the year ending 2019.

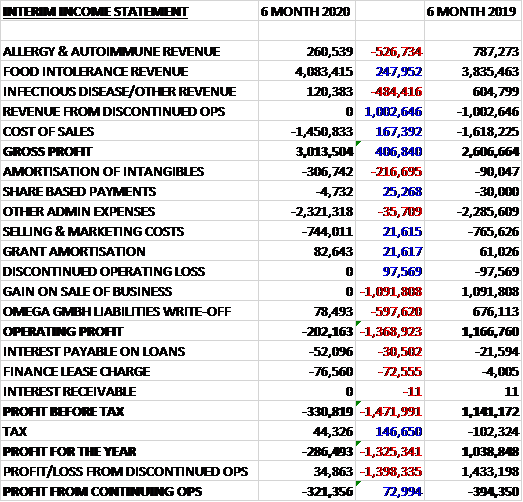

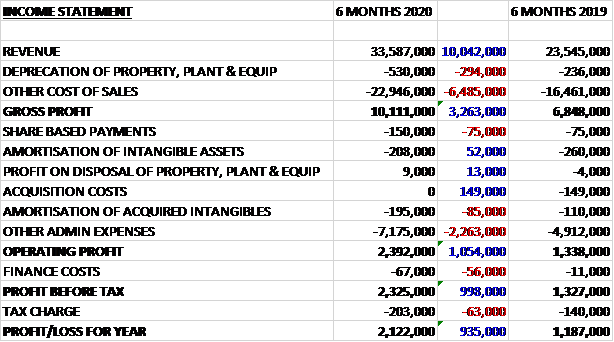

Revenues declined when compared to the first half of last year as a £1.1M growth in UK revenue, a £1.1M increase in Korean revenue and a £174K increase in US revenue was more than offset by a £4.4M decline in ROW revenue. There were £395K of acquisition costs but other operating costs were down £536K to give an operating profit £1.9M lower. There was a slightly lower profit from an associate but tax charges declined by £351K to give a profit for the period of just £26K, a decline of £1.6M year on year.

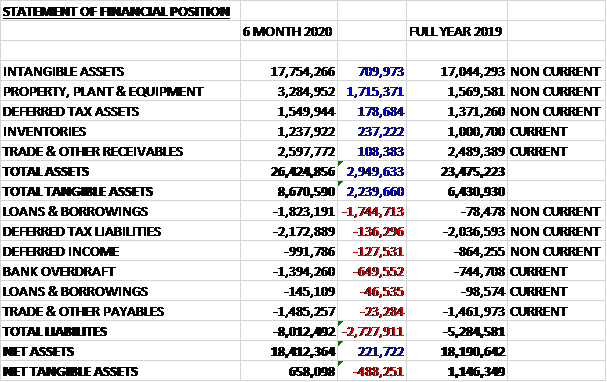

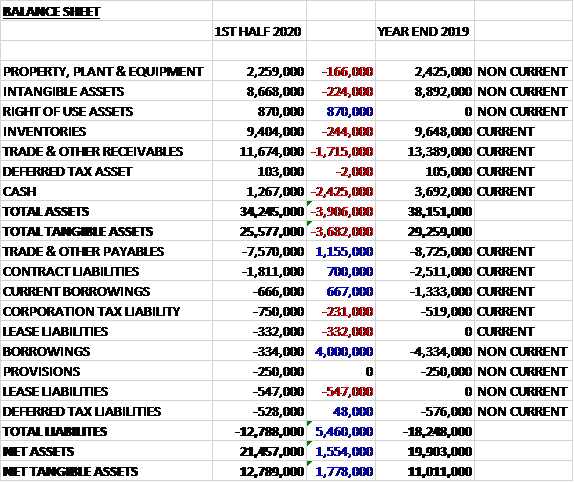

When compared to the end point of last year, total assets increased by £3.1M driven by a £5M growth in inventories and a £4.8M recognition of right of use assets, partially offset by a £5M decline in cash and a £2.7M decrease in receivables. Total liabilities also increased during the period as a £1.3M decrease in payables was more than offset by a £3M growth in borrowings and a £4.8M recognition of lease liabilities. The end result was a net tangible asset level of £32.8M, a decline of £3.9M over the past six months.

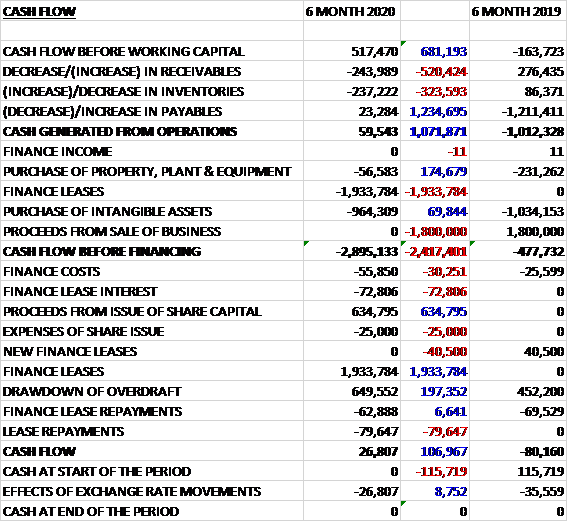

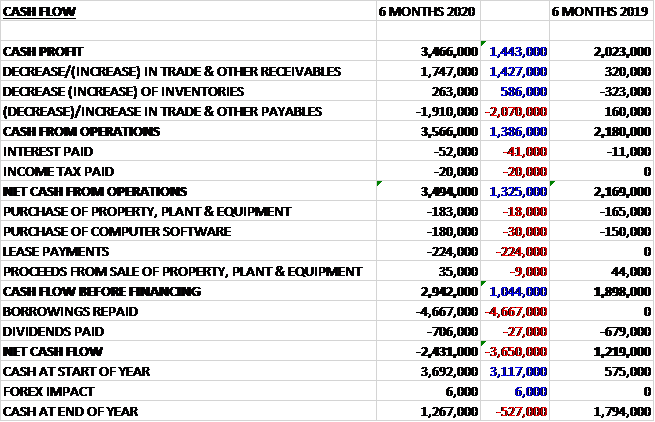

Before movements in working capital, cash profits declined by £1.5M to £1.6M. There was a cash outflow from working capital and despite tax payments reducing by £101K there was a £3.7M outflow of cash from operations, a deterioration of £5.4M year on year. The group spent £363K on an associate, £793K on fixed assets and £135K on intangible assets to give a cash outflow of £5M before financing. They took out £3M of new loans to pay the £3.1M of dividends so there was a cash outflow of £5M for the half year and a cash level of £2.2M at the period-end.

Trading in the period was impacted by challenges in export markets including Korea but they delivered strong growth in the UK and there are positive signs for healthy growth in the US markets through the key seasonal trading period.

Revenue in the UK grew by 9%. The UK retail sector remains challenging due to the uncertainties over Brexit. The US saw a revenue decline of 3.7% in local currency (although there was actually growth in GBP terms). This decline is largely down to the timing of shipments. The order book is ahead of last year. Online sales grew 13%. Sales from the home fragrance division increased by 0.5%. They had to anniversary a large account win with initial pipefill orders in the first half of last year (not sure what that means!) The board expect good full year growth for this business buoyed by new markets and product development.

Going forward, early signs for the remainder of the year are positive and the board expect to meet full year market expectations.

After the period-end the group acquired Nambe for a cash consideration of $12M. The business is a branded US homewares business with an EBITDA of $1.1M. Their sales are largely concentrated on the US. There are considerable sales and cost synergies to be achieved and the acquisition will be earnings enhancing in the full year of ownership. The business has net assets of $9.6M

At the current share price the shares are trading on a PE ratio of 10 but this rises to 13 on the full year consensus forecast. After the dividend was kept the same the shares are yielding 5.2% which is predicted to remain the same for the full year. At the period-end the group had a net debt position of £5.8M compared to net debt of £1.3M at the same point of last year.

On the 30th September the group announced that it sold its 44.5% stake in Furlong Mills, a supplier of clay and glazes. The sale is for £3.3M and will give rise to a profit of £900K. The group will continue to source its raw materials for the Stoke factory from the business and has signed a long term supply contract that closely mirrors their historical trading relationship with the mill.

On the 14th November the group released a trading update. Sales into the Korean market, specifically for the Botanic Garden ranges, continue to be weaker than expected. It is clear that the significant historic demand has led to other markets re-shipping into Korea, resulting in overstocking of the market.

Since May they have developed nearly 1,000 new products for the Korean distributor to create a fresh differentiated product in the market. These ranges have started to sell positively. They have increased due diligence of their distributors to ensure greater visibility of sales tracking; they have signed a new distribution contract with a major Korean retailer to drive growth from other premium brands in their portfolio. First shipments are expected to start in late 2019 with significant growth in 2020.

The clearing of the overstock in Korea combined with a more disciplined focus on exports has resulted in a larger than expected short term reduction in their Botanic Garden range sales. This, combined with the development cost and manufacturing processes for the new products will have an impact on the financial performance this year. As such the board now expect profit in 2019 will be materially behind market expectations.

The board are, however, encouraged by online sales, expansion in their home fragrance division and new product development to celebrate the Spode brand’s 250th anniversary. In addition the integration of Nambe is progressing well. There is no anticipated change in dividend policy.

On the 16th January the group announced that it expects pre-tax profit for the year will be in line with revised market expectations. Revenue will increase by 3% which includes the contribution from Nambe in July. Like for like revenues are down 5% as previously reported. The UK market grew by 5% despite the difficult retail backdrop.

Total online sales in the UK and US grew by 17%. Excluding the Nambe acquisition, sales in the US declined by 12%. This was driven by the strategy to reduce re-shipping into Korea and this market should return to growth in 2020.

They have taken a long term view to protect their brand in the Korean market. This has caused some short term pain through reduced export sales of the Botanic Garden range and increased costs and disruption to their factories from developing a large number of new ranges. They believe they have now made good progress stabilising this market, however.

Overall then this has been a pretty terrible period for the group. Profits were down, net assets declined and the operating cash flow deteriorated with a cash outflow at the operating level. This was being blamed on a collapse in exports to Korea brought about by overstocking. The UK seems to be doing well, however, and the group could be over the worst in Korea. The shares are not too expensive with a forward PE of 13 and yield of 5.2% but they are reliant on a recovery.