Solid State supplies specialist electronics equipment which include high tolerance and tailor made battery packs, specialist electronic components, specialist antennas, industrial computers and secure communications systems. The market for their products is driven by the requirement to address needs in harsh environments where durability and resistance to extreme temperatures is vital. Drivers in their markets include efficiency improvement, cost saving, environmental monitoring and safety.

The distribution division comprises Solid State Supplies and the manufacturing division includes Steatite and Q-Par Angus. Steatite is a supplier of electronic equipment. It designs, manufactures and supplies products that include lithium battery packs, rugged mobile computing solutions, secure communications systems, industrial computer hardware and software. Q-Par designs and manufactures antennas. It provides commercial grade and bespoke microwave antennas, subsystems and associated microwave components. Solid State Supplies is a distributor of components to the UK OEM community, selling semiconductors, related components and modules for embedded processing, control and communications switches, power management units and LED lighting.

Solid State has now released its final results for the year ended 2015.

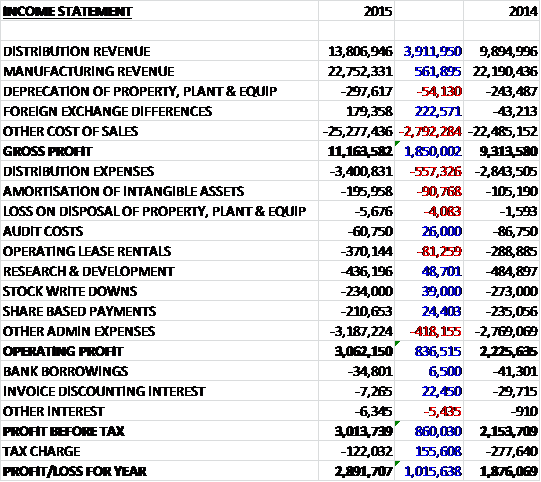

Revenues increased when compared to last year with a £3.9M growth of distribution revenue and a £562K increase in manufacturing revenues. Cost of sales also increased to give a gross profit £1.8M ahead of last time. Distribution expenses increased by £557K and “other” admin costs were up £418K, partially offset by a £223K positive swing in forex differences and a £49K decline in R&D costs which meant that the operating profit was £837K above that of 2014. There was then a decline in invoice discounting interest and the tax charge more than halved, mainly due to enhanced tax relief on R&D expenditure that will not be repeated going forward, so that the profit for the year was £2.9M, an increase of £1M year on year.

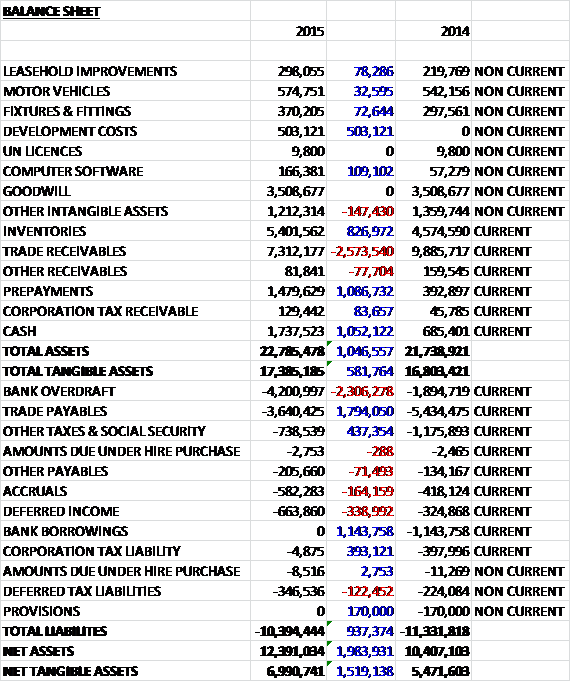

When compared to the end point of last year, total assets increased by £1M driven by a £1.1M growth in prepayments, a £1M increase in cash, an £827K growth in inventories and a £503K increase in development costs partially offset by a £2.6M decline in trade receivables. Total liabilities fell during the year as a £1.8M decrease in trade payables, a £1.1M fall in bank borrowings and a £437K decline in other taxes and social security payables were partially offset by a £2.3M increase in the bank overdraft. The end result was a net tangible asset level of £7M, an increase of £1.5M year on year.

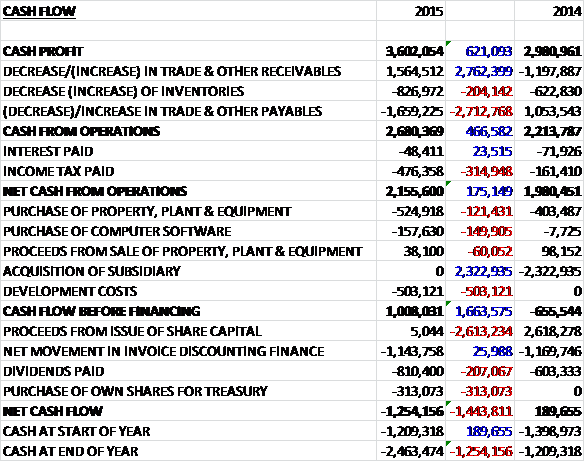

Before movements in working capital, cash profits increased by £621K to £3.6M. There was a cash outflow from working capital due to an increase in inventories and a decrease in payables, however, and after a £315K growth in the tax paid, the net cash from operations came in at £2.2M, an increase of £175K year on year. The group then spent £503K on development costs relating to the development of a new electronic monitoring unit to enable them to expand the operations of their manufacturing division into this new area, £525K on fixed tangible assets and £158K on computer software to give a free cash flow of £1M. The group then paid £810K on dividends and £313K on the purchase of treasury shares which meant that after a £1.1M repayment of the invoice financing which has now ceased, the cash outflow for the year was £1.3M and the cash level at the year-end was -£2.5M.

The pre-tax profit at the distribution division was £661K, a growth of £264K when compared to last year. The year saw the completion of the integration of the 2001 Electronics business into Solid State Supplies. After adjusting for the previously reported exit from the very low margin commodity LED business, the enhanced customer base and product ranges have delivered organic growth of about 4% which is apparently above the industry average for the sector. Margins also improved by 1.6% year on year. The business’ move towards a range of own brand products continued during the year, with the introduction of a number of high output LED modules enabling lighting companies with little experience of electronics and thermal management to benefit directly from high power LEDs. The value added services operation provided a useful contribution to the increase in gross margin throughout the year and a minor capital investment resulted in the award of a £1M contract for programmed devices from a major UK innovator in the field of Metrology.

The pre-tax profit at the manufacturing division was £3.4M, an increase of £500K year on year. Steatite performed well during the year with a 9% increase in pre-tax profits with improving market share. They are also entering new markets in the electronics industry such as green energy and security products. The business has grown export sales, aided by a new range of communications systems.

Steatite was awarded a contract by the MoJ in July 2014 for an initial three year term worth an estimated £34M for the supply and maintenance of offender tagging technology. The development of tagging devices for the government is progressing well under a dedicated management team with its own bespoke facility. The contract is progressing with expectations for a strong performance in the second half of next year. Beyond the initial MoJ contract, this new team is developing a range of devices for applications in the medical and home care sectors as well as enhanced justice platforms which the board expect to lead to opportunities in new market sectors both in the UK and abroad.

Q Par saw order intake grow and pre-tax profits were up some 142% compared to last year. Further investment will be made in the year ahead with new purpose built facilities planned, along with significant investment in test and measurement facilities that will apparently bring benefits to the whole group.

The group is somewhat susceptible to increasing interest rates and if it had been 1% higher, interest payments would have been £19K higher this year. They also have some exposure to foreign exchange changes. A 10% weakening of Sterling against the US dollar end Euro would reduce profits by £36K.

After the end of the year, the group acquired Signregion and its subsidiary Ginsbury Electronics for a cash consideration of £2.125M. Ginsbury Electronics specialises in the supply of high quality display components, monitors panels, signage and power components in the commercial, retail, industrial and military markets in UK and the rest of Europe. The consideration paid on completion was £1.6M with further payments of £175K due six, twelve and eighteen months after the date of acquisition and £525K of goodwill was generated.

After the start of the new year the group have an order backlog of £19.4M compared to £15.1M at the same point of last year. The board are continuing to see potential acquisition opportunities and this is an area that they are going to progress further going forward.

At the current share price the shares trade on a PE ratio of 18.2 which falls to 18 on next year’s consensus forecast which is not exactly cheap. After a 41% increase in the dividend, the shares yield 2% which is expected to remain the same for the year as a whole. There is currently an undrawn overdraft of £1.4M available to the group.

Overall then this has been a good year for the group. Profits were up, net assets an increased and operating cash flow was also up on last year with some free cash produced, although not quite enough to cover the share purchases and the dividends. The distribution business seems to be performing fairly well with a slow but steady improvement and the manufacturing business also had a good year that culminated in the awarding of the very material MoJ contract which should add to revenues substantially when it is up and running.

It is hard to form an opinion on the acquisition as there are no details for the profitability of the business but the price paid is not huge. So, this is a decent company with growing businesses and little in the way of debt but with a forward PE of 18 and yield of 2% the market is certainly taking this into account.