Solid State has now released their interim results for the year ending 2018.

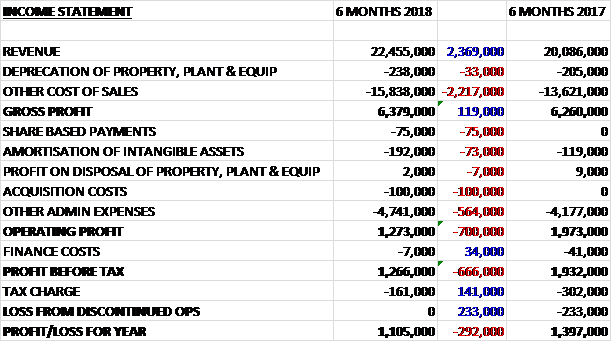

Revenues increased by £2.4M when compared to the first half of last year. Cost of sales grew by £2.4M to give a gross profit £119K higher. Share based payments grew by £75K, amortisation increased by £73K, there was £100K of acquisition costs and other admin expenses grew by £564K reflecting the planned investment in sales staff and the full period cost contribution from Creasefield, which meant that the operating profit was down £700K. Finance costs declined by £34K, however, and tax charges fell by £141K to give a profit for the period of £1.1M, a decline of £525K year on year.

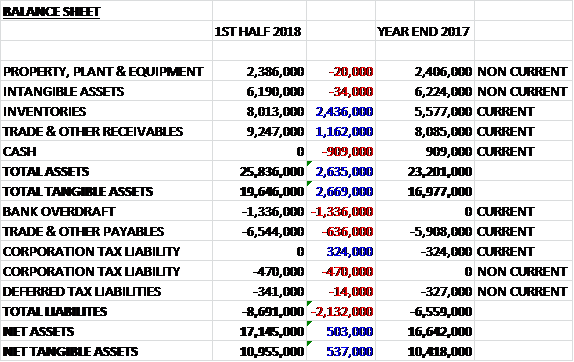

When compared to the end point of last year, total assets increased by £2.6M, driven by a £2.4M growth in inventories and a £1.2M increase in receivables, partially offset by a £909K decline in cash. Total liabilities also increased during the period due to a £1.3M increase in the bank overdraft, a £636K growth in payables and a £146K increase in the corporation tax liability. The end result was a net tangible asset level of £11M, a growth of £537K over the past six months.

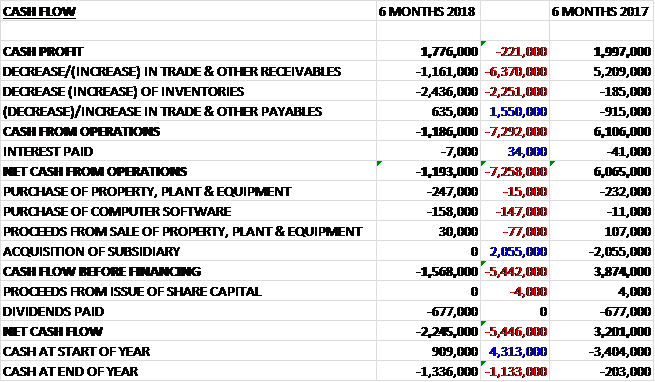

Before movements in working capital, cash profits declined by £221K to £1.8M. There was a cash outflow from working capital and after interest payments declined by £34K, the net cash outflow from operations was £1.2M. The group also spent £247K on property, plant and equipment along with £158K on intangible assets to give a cash outflow of £1.6M before financing. They also spent £677K on dividends to give a cash outflow for the period of £2.2M and a cash level of -£1.3M at the period-end.

There was strong organic growth in the distribution division of 20% and a 7% increase in manufacturing revenue but changes in product mix have affected the overall gross margin and the combination of the increased proportion of distribution sales and a change in mix of sales within the manufacturing business resulted in a near 3% reduction in the gross margin.

As can be seen there was a strong cash outflow from working capital due to some strategic investments including: within the distribution division they have taken £400K of new product line into inventory to support a multiyear space customer in an obsolescence management programme. In addition they have spent £500K in inventory for a customer specific product to secure supply and pricing for committed orders. In the manufacturing division they have spent £900K on work in progress in relation to an ongoing project which is currently scheduled to ship in the second half. In addition they have made investments to secure supply and pricing as lead times are increasing in a number of areas such as battery cells, memory and component assemblies and the distribution division.

Manufacturing revenues increased by 7%, driven by the full year impact of the Creasefield acquisition. Within the division, over £2.5M of rail printer revenue that occurred last year did not recur and has been replaced by new power and computing sales. Good progress is being made in implementing a margin enhancement strategy through additional added value services and operational efficiencies aimed at addressing certain low margin battery business inherited from the Creasefield acquisition. The benefits of this activity should start to be seen in Q4 and into next year.

The restructuring of the communications business unit and Leominster operations is now complete and has positioned the business for future growth but the lead time to win and deliver some of the complex antenna programmes has taken longer than expected, resulting in a performance below management expectations. The prospect pipeline remains encouraging, positioning the business for a stronger 2019. After the period-end, an important order for mesh radios was secured from the Government customer.

The power business is responding to strong levels of enquiries in varied applications. They are seeing evidence that the oil and gas sector is showing sustained recovery beyond just a restocking spike evidenced by a new battery pack project for a brand new well development in Africa. The harsh environment robotics project continues to progress well through the engineering phases, with the aim to complete the product development in H1 2018 and then move to review production opportunities.

The computing business unit had a strong performance in the first half with bookings and billing ahead of plan and product margins being maintained. This trend, which reflects a 9% improvement in billings on last year, is the result of investments in sales initiatives. They are actively targeting a number of new opportunities and programmes in the rail sector which they hope will be a good new market for this business.

The distribution business delivered close to a 20% increase in revenues to £9.5M, reflecting strong organic growth across their product rang. Order intake in the first half is up by 39% over the same period last year and the total order book is at record levels. The market remains sensitive, however. The business continues to improve its offering in the growth markets of wireless, cellular and internet of things whilst maintaining a strong offering in the specialist areas of military and aerospace. Investments in engineering support in these areas have led to significantly increased business levels in, for example, the Global Systems for Mobile arena.

Investments that have been made in the sourcing and obsolescence services operation are expected to start to bear fruit in the second half of the year and investment continues in this area to provide secure storage areas within the existing warehouse. Efficiency improvements are now well underway with a wireless warehouse project to speed productivity expected to complete before the year-end. Investment continues in personnel and the working environment with continuous training and infrastructure improvements including the conversion of all lighting to LED. The division expects to hit its second half organic growth targets and exceed order input targets.

At the period-end, the group order book was £20.1M, which is 38% up on the prior year. Order intake in October was at a record level with a good spread of customers and the board are pleased with the new business pipeline and level of new contract awards across the group. This gives them confidence that despite the reduction in the margin as a result of the mix of product sales, the markets that the group serves are resilient and that the group can deliver a strong second half performance and continue to deliver growth.

At the current share price the shares are trading on a PE ratio of 16.7 which falls to 14.8 on the full year forecast. After the interim dividend was maintained the same, the shares are yielding 2.6% which is expected to be maintained for the full year too.

Overall then this has been a bit of a mixed set of results. Profits declined due to the product mix and the resultant lower margins. Net assets did increased but the operating cash flow was down with a cash outflow, although this was not helped by working capital movements. The distribution business is performing well with a good revenue increase and record order books. The manufacturing business is more mixed, however, with the reduced profits due to no rail printer revenues this year, antenna delays and the Creasefield business still having low margins. There is supposedly some improvement in the latter two going forward and the pick-up in the oil and gas market is encouraging, though. This is starting to get interesting again but with a forward PE of 14.8 and yield of 2.6% I would like to see more evidence of profitable growth before buying back in.

On the 13th April the group released a trading update covering the year ended 2018. The adjusted group profit will be in line with market expectations at around £3M with revenue slightly above expectations at £45.5M. The distribution and value added services division maintained strong organic growth of close to 18% and the manufacturing division has delivered a 10% increase in revenues. The overall gross margin will show a reduction, however.

They are continuing to make progress with a significant development contract in their Power business and franchise discussions in the distribution division, both of which are expected to contribute to 2019 results. The lead time to win new business in the Communications business has been longer than expected.

A significant proportion of the sales in the Communication business are exports. Securing overseas opportunities is proving harder than expected, particularly in North America where it appears domestic suppliers are being preferred on contract awards. As a result, the group are reducing their expectations for this business for 2019 which will have a negative impact on margin mix for the group.

This update suggests there is little prospect for profit growth in the foreseeable future so I am steering clear for now.

On the 11th June the group announced that it had received orders to supply power units for autonomous robots operating in cold climate conditions with a combined value of £4.3M. They were commissioned to design and supply the power units for the end customer’s smart warehouses. Deliveries of the power units are expected to start during HS 201, contributing to the current year and continuing into next year. The contract will deliver additional recurring revenues through the supply of replacement cells in subsequent years as part of a support and maintenance agreement.