Trifast has now released their interim results for the year ending 2018.

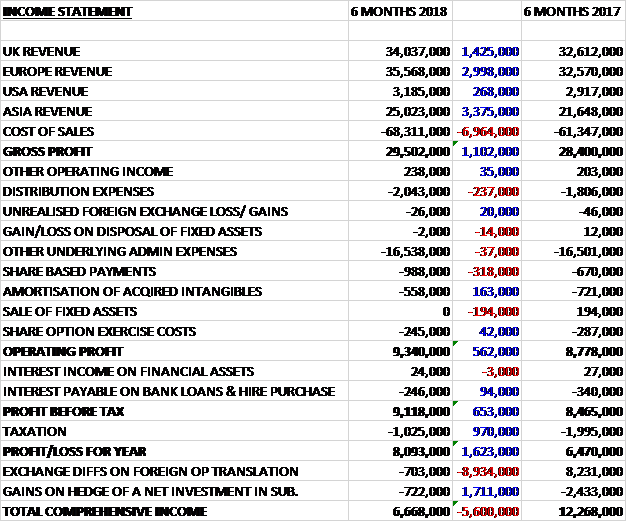

Revenues increased when compared to the first half of last year with a £3M growth in European revenue, a £1.4M increase in UK revenue, a £3.4M growth in Asian revenue and a £268K increase in US revenue. Cost of sales increased by £7M to give a gross profit £1.1M higher. Distribution expenses increased by £237K, share based payments were up £318K and there was no sale of fixed assets, which brought in £194K last time. The amortisation of acquired intangibles declined by £163K, however, and other admin expenses were broadly flat to give an operating profit £562K higher. Interest payments fell by £94K and tax charges were down £970K due to a deferred tax asset not recognised last year for trapped tax losses in the UK as a result of the share option exercised in the year, which meant that the profit for the period was £8.1M, a growth of £1.6M year on year.

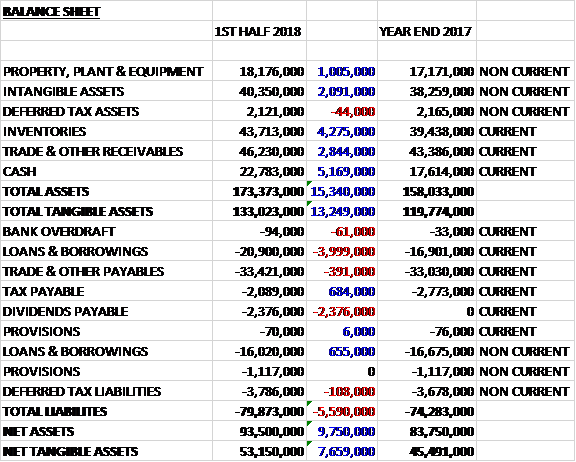

When compared to the end point of last year, total assets increased by £15.3M driven by a £5.2M growth in cash, a £4.3M increase in inventories, a £1.8M growth in receivables, a £2.1M increase in intangible assets and a £1M growth in property, plant and equipment. Total liabilities also increased over the past six months due to a £3.3M increase in borrowings and a £2.4M growth in dividends payable. The end result was a net tangible asset level of £53.2M, a growth of £7.7M over the period.

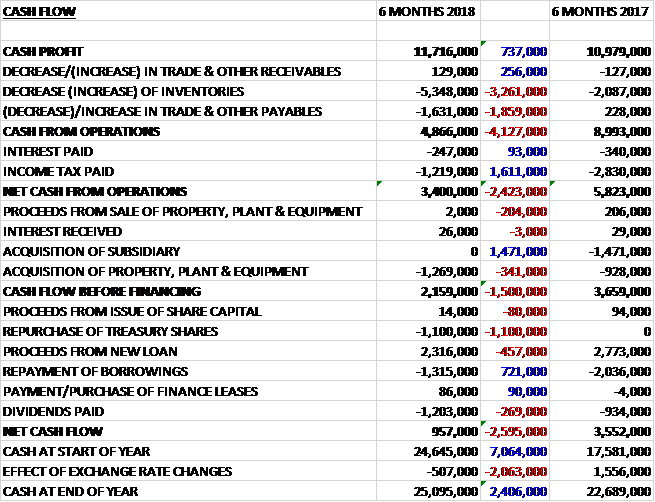

Before movements in working capital, cash profits increased by £737K to £11.7M. There was a large cash outflow from working capital, mainly due to an increase in inventories but tax payments fell by £1.6M to give a net cash from operations of £3.4M, a decline of £2.4M year on year. The group spent £1.3M on property, plant and equipment to give a free cash flow of £2.2M. Of this, £1.2M was paid out in dividends, and £1.1M went on purchasing treasury shares – presumably for director pay. The group took out new loans of £1M which gave a cash flow of £957K and a cash level of £25.1M at the period-end.

The underlying pre-tax profit increased by 9.7% but this has benefited from favourable exchange rates and at constant currency the growth was 4.5%. Gross margins have been maintained close to the target of 30% but they have fallen when compared to the first half of last year reflecting the Euro weakness against the dollar.

The underlying profit in the UK business was £3.9M, a growth of £832K year on year with revenues increasing by 4% due to increased distributor revenues and an increase in contract sales to several key OEMs. The underlying operating margin has improved strongly due to several high margin sales in the period. Forex gains made on the Euro distributor sales have to date been able to offset the negative impact of inflationary pricing pressures following the Brexit vote. The rest of the increase reflects a reduction in the overhead spend.

The underlying profit in the European business was £3.9M, a decline of £1.4M when compared to the first half of last year despite revenues increasing by 2%. The automotive sector experienced growth, most specifically in the Netherlands and Sweden with increases of 11% and 9%. In Italy, the importance of the automotive sector is building, with sales in this sector increasing by 27%, albeit from a small base. Volume reductions at one of the group’s largest domestic appliance OEMs have partly offset other increases, however. Trading volumes with that customer had been abnormally high in the first half of last year as the group supported a significant global product recall programme.

The decline in profits is due to a fall in margins, particularly a reduction in gross margins in the Italian business where the impact of increases in purchase costs at the end of last year has continued into this period. This has been in addition to a planned increase in fixed production costs in Italy as they invest for future growth. Whilst investment costs to get the new Spanish Greenfield site up and running represent most of the overhead led decrease in the region’s operating margin.

The underlying profit in the US business was £116K, a decrease of £50K when compared to the first half of 2017 with revenues increasing by 4%, which was lower than anticipated. This reflects a reduction in their sales to the electronics sector, largely because of the manufacturing issues some of their key customers are experiencing after Hurricane Harvey. The start of production on new automotive wins in the region has helped to offset this negative impact, however. Underlying operating margins have fallen sharply reflecting lower gross margins due to the lower electronics sales following the hurricane.

The underlying profit in the Asian business was £4.4M, an increase of £1.1M year on year with revenues increasing by nearly 11%, largely driven by increases in the domestic appliances business in Singapore and automotive wins for the Chinese, Malaysian and Taiwan operations. In Malaysia, the increase in intercompany co-operations put in place following the downturn in the domestic economy has continued to bear fruit with revenues up 7%.

During the period the group committed to a plan to sell a factory in Malaysia. A buyer has been identified for the asset and management are expecting the transaction to complete before the year-end. The group is expecting to receive around £1.6M for the factory which is higher than the £1M held on the balance sheet for the asset.

In Asia, over the course of the year the group will be investing £1M in the construction of a mezzanine level at their Singapore facility to expand capacity, initially by 25%, and to increase R&D capabilities. In Shanghai they have just expanded their warehousing and inspection facilities to support growth being seen in the Chinese domestic market and the recent expansion into the Japanese market.

In Europe, the Greenfield site in Spain is now up and running. First orders have been processed, stock is on the shelves and the pipeline is looking strong. In Italy, the investments they have made in the heat treatment plant last year are beginning to pay back, bringing an end to the production bottlenecks that were limiting their ability to expand capacity at the plant. Looking ahead they have further investment planned to support the ongoing growth in the European distribution sites, including a warehouse expansion in the Netherlands and a TR innovation and technical centre situated in Gothenburg.

In the UK they are in the process of expanding their warehousing facilities in Northern Ireland to support the strong ongoing growth they are seeing at the site whilst in the US, despite the immediate difficulties following Hurricane Harvey, they plan on investing to build the local team and to support future growth in this important market.

The group continues to search for acquisitions. Since the year-end they two larger international targets were thoroughly investigated over several months but both were rejected due to future revenue growth risk.

Going forward, the second half has started well and with a robust pipeline in place, the board remain confident of delivering their expectations for the full year. There remain some macroeconomic factors at play, however, including the ongoing volatility in forex and raw materials markets, input cost pressures in the UK due to protracted sterling weakness and the wider potential implications of Brexit on the UK economy.

At the current share price the shares are trading on a PE ratio of 25 which falls to 18.8 on the full year consensus forecast. At the period-end the group had net debt of £7.9M compared to £6.4M at the prior year-end, not helped by currency movements. After a 10% increase in the interim dividend, the shares are yielding 1.4% which increases to 1.5% on the full year consensus forecast.

Overall then, this has been another decent period for the group. Profits and net assets both grew, although the former has been favourably impacted by forex movements. The net cash from operations did decline, but this was due to working capital movements and cash profits increased with some decent free cash flow generated.

Operationally it has been a bit of a mixed bag. The UK and Asian businesses have performed well with the former enjoying more higher margin product sales and Asian demand being strong for both appliances and automotive. The European business struggled somewhat due to higher costs in Italy and the set-up costs for the new Spanish division and in the US, the performance was hampered by Hurricane Harvey. The shares aren’t cheap with a forward PE of 18.8 and yield of 1.5% but I remain happy to hold on to this good quality company.

On the 15th February the group released a trading update covering Q3. The global visibility and order pipeline is very encouraging and the business is matching management expectations in revenue and margins with the US business continuing to recover following the hurricane season.

The capital investments made to the manufacturing operations in Italy and Taiwan are already delivering ongoing benefits and the significant expansion of the Singapore facility is on track with phase one expected to complete by the year-end.

Overall the board remain confident that the group will deliver its expectations for the year as a whole.

On the 5th April the group announced the acquisition of Precision Technology Supplies, a supplier and distributor of stainless steel fastenings in the UK to the electronics, medical instruments, petrochemical, defence and robotics sectors. There is an initial cash consideration of £8.5M with a contingent consideration of £2.5M and the acquisition is expected to be earnings enhancing in 2019 and made a profit of £720K last year. The business will run as a stand alone business in the group.

On the 19th April the group released a trading update for the year ended 2018. The European operations have benefited from a stronger second half of underlying organic growth. They have witnessed good growth across a number of key market sectors, particularly in the automotive sector with double digit growth across both the Dutch and Swedish operations. In addition the newest new location in Spain and the new innovation and technical centre in Sweden are both providing good prospects for future growth. On the domestic appliances side, they have seen an expected return to more normal trading levels over the year following the abnormally high sales volumes as they supported a significant global product recall programme for a key customer.

Following a stronger second half, the UK also experienced robust organic growth reflecting a targeted approach aimed at growing both core multinational OEM customers and European distributor sales. Looking ahead, recently announced changes in planned production volumes in the diesel automotive sector could influence activity in the region although to date the expected impact is relatively minor.

Asia has performed well. They have seen a solid year on year growth particularly across the domestic appliances and automotive sectors. As expected the strong double digit growth experienced in the first half of the year was not sustained into the second half, however. This was largely due to the ongoing reduction in demand at one of the region’s key automotive customers as a result of its own restructuring programme, coupled with the impact of deliberately reduced volumes following an e-bidding process at an electronics multinational OEM customer.

Looking ahead, the new warehouse in Shanghai is already providing additional support for the ongoing strong automotive growth in China and Japan. Furthermore, the significant capital investment they have made to their manufacturing facilities in Singapore will also start to feed through into margins over the coming year.

In North America, the TR operation is recovering well following the impact of Hurricane Harvey with strong year on year growth being driven from new automotive wins in the region. They plan to carry on investing to build the local team and to support future growth in this market and they are opening a larger TR warehouse in Houston this month.

Overall, following an encouraging finish to the year, the underlying profit is slightly ahead of management expectations. All of their main geographies, excluding the US, have delivered growth in profits.

During the year the group have initiated a number of significant capital investment projects. Their previous investments, specifically into their Italian manufacturing operations are already delivering capacity benefits and the completion of the mezzanine expansion in Singapore was achieved just ahead of the year-end. Further warehouse expansion plans are underway in the Netherlands and the US.

Overall this looks fine and I continue to hold.