Empresaria is an international specialist staffing group, with a strategy to be diversified and balanced across geographies and sectors. They follow a multi-branded business model operating in 18 countries. The group has a philosophy of management equity to align the interests of shareholders and key management through the sharing of risk and reward with operating business management teams investing directly in their own businesses with the group taking a controlling interest. There is a decentralised structure with local management retaining operational autonomy.

Nearly half of all revenues are derived from the Technical and Industrial sector with the group also active in IT, Finance, Retail, Executive Search and Healthcare. They operate in the UK, Germany, Austria, Finland, Estonia, Japan, Indonesia, India, Australia, Chile, UAE, Thailand, Singapore, China, Hong Kong, Philippines, Malaysia and Mexico.

The group earns revenues from permanent recruitment when a candidate is placed in a role with a client, with the fee typically being a percentage of the candidate’s total salary. Revenues are earned on temporary recruitment for the time worked by the candidate as a percentage of the salary earned in the period. The group also provides training services in SE Asia and offshore recruitment services in India.

The group has now released its final results for the year ended 2014.

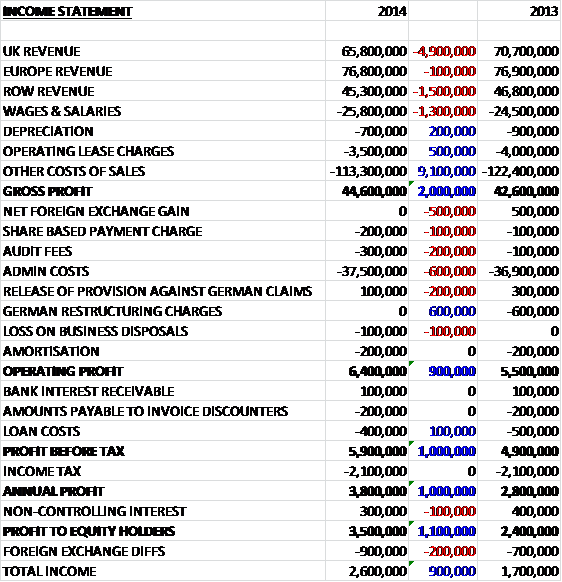

Revenues declined across all regions year on year with a £4.9M fall in UK revenue due to the end of a large airport contract, a £1.5M decrease in ROW revenue and a £100K fall in European revenue due to adverse currency movements. Operating lease charges declined too, however, as did other cost of sales to give a gross profit £2M above that of 2013. We then see an increase in admin costs and the lack of a forex gain that occurred last time, partially offset by no German restructuring costs so that operating profit was some £900K above that of last year. There were slightly lower loan costs and slightly less profit was attributable to non-controlling interests so the profit for equity holders was £3.5M, an increase of £1.1M year on year.

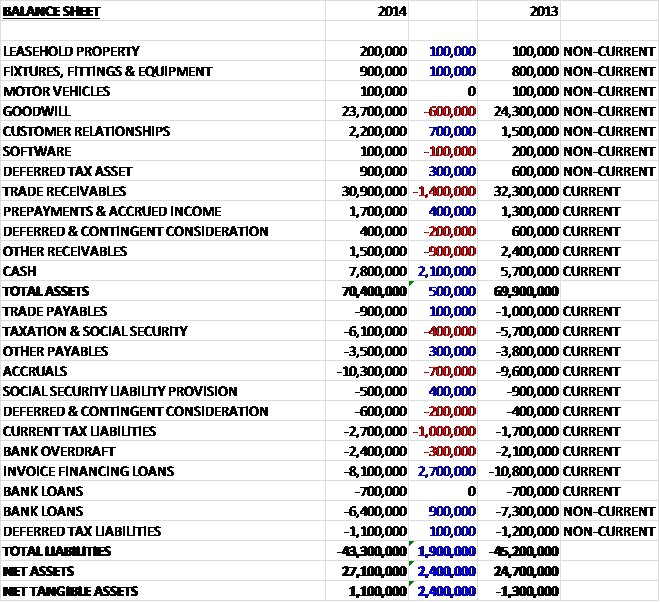

When compared to the end point of last year, total assets increased by £500K driven by a £2.1M growth in cash, partially offset by a £1.4M fall in trade receivables, and a £900K decline in “other” receivables. Total liabilities fell during the year as a £2.7M decline in invoice financing loans and a £900K decrease in bank loans were partially offset by a £1M increase in current tax liabilities. The end result is a net tangible asset level of £1.1M, which is not great although it has improved by £2.4M year on year.

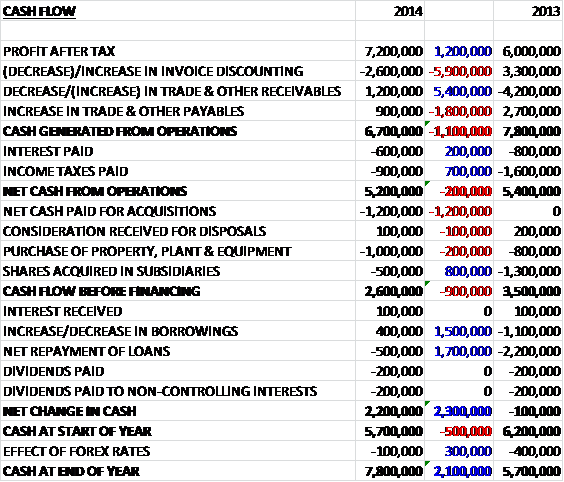

Before movements in working capital, cash profits increased by £1.2M to £7.2M. We then see a fall in invoice discounting compared to an increase last time that meant that despite the lower tax paid, the net cash from operations fell by £200K to £5.5M. The group then spent £1M on fixed assets, £500K on shares in the subsidiaries and £1.2M on acquisitions to give a cash inflow of £2.6M before financing. Some of this cash was used to pay back debt and pay out dividends but the cash flow for the year came in at £2.2M to give a cash level of £7.8M at the year-end.

Market conditions have generally been good during the year, particularly in the UK but certain markets do remain uncertain and the group is obviously susceptible to adverse economic conditions and any knock on effect on the job market.

The operating profit in the UK was £2.2M, an increase of £100K year on year with revenues falling by 7% due to a reduction in the technical and industrial sector driven by the completion of a large airport project coupled with the deliberate move away from low value work. This was partially offset by growth from Financial Services and Domestic Services, with the banking and insurance markets seeing a marked rise in confidence in the year. NFI grew by 1% to £15.9M but adjusting for the prior year branch closures and disposal of the payroll services business, the underlying growth was 6%. The group opened new offices in Manchester during the year in Technical and Industrial, and Domestic Services so they now have three sectors operating in that market.

The operating profit in Continental Europe was £3M, a growth of £1.7M when compared to 2013. Revenues were marginally down during the year and NFI was up 8% to £15M. Currency movements impacted on these results with revenue and NFI up 5% and 14% respectively on a constant currency basis. Germany was the main driver for profit growth following the branch restructuring and cost reductions that took place in previous years. All claims for retrospective pay and social security have been agreed and no further claims are able to be made so £100K of provisions have been released. In Finland, the business returned to profit in the year although market conditions remain difficult due to the severe economic situation. At the start of 2015 the group disposed of the underperforming small businesses in the Czech Rep and Slovakia.

The operating profit in the rest of the world was £1.2M, a decline of £900K when compared to last year with revenues down 3% but NFI up 6%. The business suffered from negative currency impacts with NFI up 9% on a constant currency basis. There were good performances in Japan, India, Thailand and Australia. The operating profit fell year on year due to the investments in new offices in Mexico City, Santiago, Kuala Lumpur and Hong Kong. The group have started to restructure their training business in Indonesia and their executive search business in China where less favourable economic conditions have had a negative impact on profits. The standalone search business in Malaysia was sold to management in January 2015 following a small loss in the year but the group opened up another office in Kuala Lumpur under another brand.

The group have entered two new emerging staffing markets – UAE and Mexico with the opening of a Monroe office in Kuala Lumpur after the disposal of the Metis brand in the country, maintaining a presence in that market. The executive search recruitment business in China is also rebranding to Monroe Consulting, the successful brand already covering South East Asia and parts of Latin America. In July the group increased their shareholding in the executive search business in Shanghai for an initial cash consideration of £300K with a further £100K payment deferred until 2015.

In March the group purchased 51% of the shares in BW&P, a Dubai based company specialising in permanent sales in the Technical and Industrial sector for an initial consideration of £300K with two further payments continent on the performance of the business over the next year. The acquisition generated goodwill of £66K. The business services clients throughout the GCC region and specialises in construction and engineering but also covers a wide range of professional sectors. The business is not directly reliant on the oil price and the management team have a proven track record in the region – this seems like a decent price to pay for this business.

In December the group purchased 75% of the shares in Ball and Hoolahan, a UK based company specialising in permanent sales in the Marketing sector for an initial consideration of £984K with one further payment contingent on the performance of the business in 2015. This acquisition generated goodwill of £503K. The business has a long track record and specialises in the creative media and digital sectors. The acquisitions did not generate any profit this year but had the investments been made at the start of the year, profits would have been £200K higher.

The group is somewhat susceptible to exchange rate changes, particularly against the Euro and a 10% strengthening of Sterling against the currency would adversely affect profits by £400K. They are also susceptible to increases in the interest rate with a 100 basis point increase reducing profits by £200K. Another potential risk for the group is that of regulation. In Germany for example, there are plans to increase the minimum wage and proposals to limit the length of time a worker can be a temporary worker.

At the current share price the shares trade on a PE ratio of 11.6 which falls to 9.7 on next year’s consensus forecast which seems rather cheap to me. At the year end the group had a net debt position of £9.8M and although this has improved by £5.4M during the period, this is still quite high for a company of this size. There is not much in the way of a dividend yield here with the shares yielding 0.8% this year which is expected to remain the same next year.

Overall then this seems to have been a decent year for the group. Profits increased, as did net tangible assets, but they still look precariously low to me. Operating cash flow deteriorated year on year but this was due to changes in invoice discounting and cash profits increased and there was a decent amount of free cash. The result in the UK was fairly flat but real progress was made in Europe after last year’s restructuring in Germany. The profit in the ROW declined, however, due to investments made in new offices. At a forward PE of 9.7, this share does look cheap but on the other hand the dividend yield is rather pathetic and there is a lot of debt (I suppose the two go hand in hand). Overall though, I do quite like the look of this share.