T. Clarke has now released its interim results for the year ending 2015.

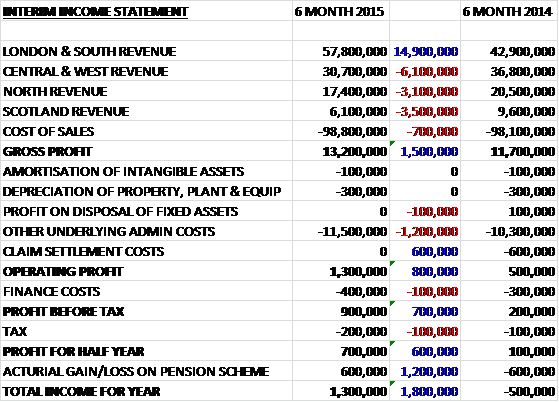

Overall revenues increased when compared to the first half of last year as a £14.9M growth in Southern Revenues was mostly offset by a £6.1M fall in Central and West revenue, a £3.5M decline in Scottish revenue and a £3.1M fall in Northern revenue. Cost of sales also increased slightly to give a gross profit some £1.5M ahead of last time. We then see an increase in underlying admin costs, partially offset by the lack of a £600K claim settlement cost that occurred last year so that the operating profit was £800K higher than in the first half of 2014. A small increase in both finance costs and tax expenses meant that the profit for the half year stood at £700K, an increase of £600K year on year.

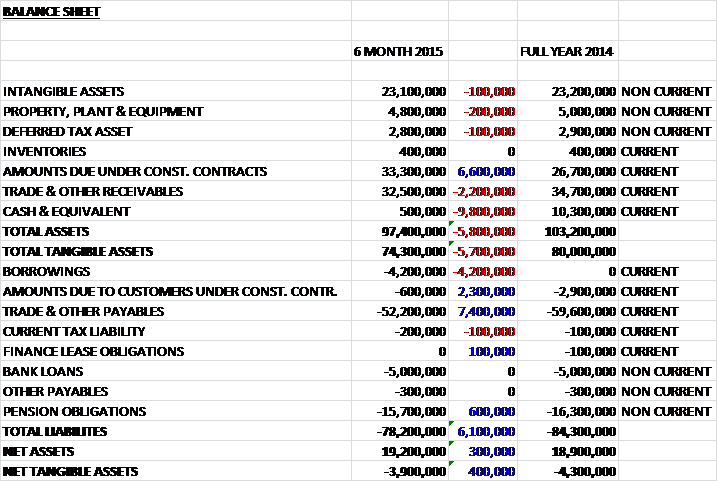

When compared to the end point of last year, total assets at the half year point of 2015 fell by £5.8M driven by a £9.8M decline in cash and a £2.2M fall in receivables, partially offset by a £6.6M increase in amounts due under construction contracts. Total liabilities also fell during the period as a £7.4M decline in payables and a £2.3M fall in amounts due to customers under construction contracts were partially offset by a £4.2M increase in borrowings to give a net tangible asset level some £400K better than at the end of last year but still negative at -£3.9M.

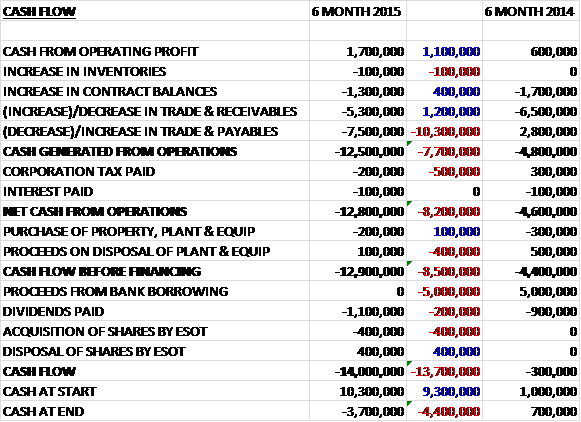

Before movements in working capital, cash profits increased by £1.1M to £1.7M. There was then a huge outflow of working capital, driven by a £7.5M fall in payables and a £5.3M increase in receivables and after minimal tax and interest, there was a £12.8M cash outflow at the operating level, an increase of £8.2M year on year. Once again there was minimal capital expenditure but the group did spend £1.1M on dividends, which seems a little frivolous to me and left the group with a £14M cash outflow at the half year point and a cash level at the period end of -£3.7M.

The underlying operating profit in the London and South division was £1.2M, a positive swing of £1.6M when compared to the first half of last year and the operating margin increased to 2.3% with an order book of £210M. Good progress has been made on promoting the group’s M&E offering in London with new projects including Chiswick Park building 7, additional work for Selfridges and Summit House, a commercial office environment. A number of the larger schemes that have been secured are now at the stage where onsite activities can commence and generate meaningful revenues, including Angel Court, Mizuho Bank, Principal Place, Rathbone Square and London Wall Place.

These new projects are in addition to the other key schemes were they already on site including BBC Television Centre, Bloomberg London, Project Nova, Ruskin Square in Croydon, South Bank Tower, Tate Modern and Victoria Underground Station. The group are currently bidding in limited competition for a number of other London schemes where decisions are expected to be made before the end of the year.

The underlying operating loss in the Central and West division was £600K, a negative swing of £1.1M when compared to the first half of 2014 and the order book fell £7M to £43M at the period-end. This Cardiff business suffered a disappointing performance due to a challenging student accommodation project which is finally due to close out in October and revenues for 2015 have been affected by the same principal contractor withdrawing from a secured project on which the business was partnering with them. Elsewhere across the division, good progress is being made securing projects across a number of sectors with existing clients and new client opportunities. The group are particularly encouraged at the larger projects they have been securing in the South West.

The underlying operating profit in the Northern division was £700K, a decline of £200K year on year with operating margins falling from 4.3% to 4.1% and the forward order book increasing by £8M to £43M. This team is based at Accrington and will shortly relocate to larger offices in Chorley which are well located to serve the current client base in the region. Two significant facilities management contract wins were awarded that means they now provide these services for 500 care homes and 60 office buildings nationwide operated from Leeds. The business also continues to work exclusively for BAE at Warton and Samlesbury and continues to pursue additional opportunities at Barrow-in-Furness.

The underlying operating profit in Scotland halved to just £100K in the first half of the year with the operating margin collapsing from 2.4% to 0.7% although the order book did increase by £4M to £24M. The business saw a slightly quieter first half to the year than expected but it is believed that there will be an active second half to the year, particularly in the residential sector where they remain the contractor of choice to the leading house builders in the Scottish market. The division continues to seek opportunities in the wider M&E sector having recently secured a project at Hunterston Power Station on the west coast of Scotland. Intelligent Buildings is also gathering significant momentum with a number of key contracts secured.

The group’s £5M three year revolving credit facility was fully drawn at the period end. The latest review of the overdraft facility was completed in July and a further £3M working capital facility was arranged. Curiously the group also mentions that it has available bonding facilities of £17.5M and I must admit that I don’t know what is meant by this. During the period the Chairman David Henderson has indicated that he wishes to spend more time on his other business activities and will be stepping down in September. He will be replaced by the senior independent director, Iain McCusker.

The order book now stands at a strengthened £320M compared to £275M at the same point of last year, of which £155M is due for delivery in 2016 and some £108M for the second half of this year as the remainder of the low margin contracts secured during the recession work their way through to completion. The signs of improvement in the London markets continue to be seen and the group expects to see further opportunities for margin growth (which still stands at a wafer thin 1.3% for H1 2015) next year and beyond in the wider markets across all UK locations.

After an unchanged interim dividend of 0.5p per share, the shares currently yield 4.1% which is the same as the estimate for the full year. Net debt at the period end stood at £8.7M compared to £4.3M as the same point of last year as the group invested in its engineering resources in order to ensure the delivery of the larger order book and is likely to improve during the second half of the year.

Overall then, this was a bit of a mixed update. Profits did increase year on year but were broadly flat if last year’s claim settlement cost is removed. Net assets also increased as the pension deficit fell slightly but net tangible assets remained negative but it is the cash flow statement that really tells the story. Despite a small increase in underlying cash profits, there was a huge outflow of working capital as the group gears up to start on projects during the current market improvement. This is actually quite a dangerous time for some companies as the cash levels become very constrained and net debt increases. Quite why the group feels it is prudent to pay a dividend during this time is slightly beyond me but there it is.

Operationally, the London and SE division seems to be seeing the benefit of the improved construction market and the inference is that the new projects are being won on a proper margin. Elsewhere in the country things are rather less positive with Scotland slowing down, the North remaining subdued and problems with a principal contractor affecting performance in Wales. The order book is certainly up, however, and should the group get through the second half of the year with no major issues, next year should be far more profitable but I am unsure whether I want to take the risk with more attractive investments out there in my view.

The share price does seem to be in a general up trend but I’m still not sure about this one…

On the 19th November the group released a trading update where they stated that the underlying performance for the year continues to be in line with board expectations. Net debt has reduced during the second half of the year and as at the end of October stood at £6M in line with internal forecasts. The group’s order book at the end of September was 15% higher year on year and maintained at the level of £320M reported with the interim results. More pleasingly, the board can see a significant improvement in the quality of their order book as they work through the majority of contracts awarded during the down cycle. They are increasingly confident that this will be reflected in a material increase in operating margin during 2016 and 2017. The improving quality if the order book is due to concentrating on London and bidding only on contracts that offer appropriate returns.

Having reviewed the opportunities of the Bristol and Cardiff offices, they board have concluded that they are not capable of delivering the quality of opportunity or level of sustainable margins that they require and therefore both will be closed by the end of this year. The offices are expected to incur a pre-tax loss of £2.6M, of which £300K relates to cash closure costs.

It has also been announced that Mike Robson has been appointed as a non-executive director. He qualified as a chartered accountant with PWC and is currently a director at Azure Partners which offers strategic consultancy services to directors and business owners.

Overall then this seems to have been a decent update with the promise of increasing profit margins in the coming years as their contracts improve following the end to the downturn.

On the 15th January the group announced a trading update for the year where the board stated that overall they expect results to be in line with expectations. The cash position has improved significantly during the second half of the year as major new contracts come on stream with a net cash position of £6.6M at the year-end. The replenished forward order book remained at a similar level to the end of last year and markets remain active with the group tendering for work particularly stretching into 2017 but they remain focused on opportunities that will drive margin improvement.

They are currently the preferred bidder on a number of London projects with a combined value in the region of £65M, none of which is in the current forward order book so if won, this should increase that considerably.