Sylvania Platinum has now released their interim results for the year ending 2018.

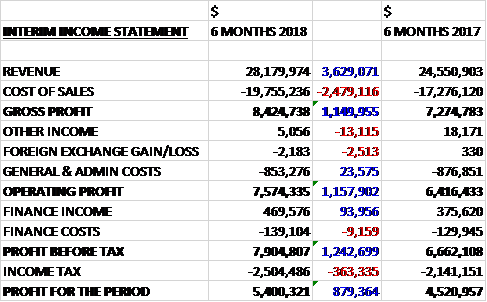

Revenues increased by $3.6M when compared to the first half of 2017. Cost of sales also increased to give a gross profit $1.1M higher. General and admin costs were slightly lower which meant the operating profit was $1.2M higher. There was a $94K increase in finance income but tax charges grew by $363K to give a profit for the half year of $5.4M, a growth of $879K year on year.

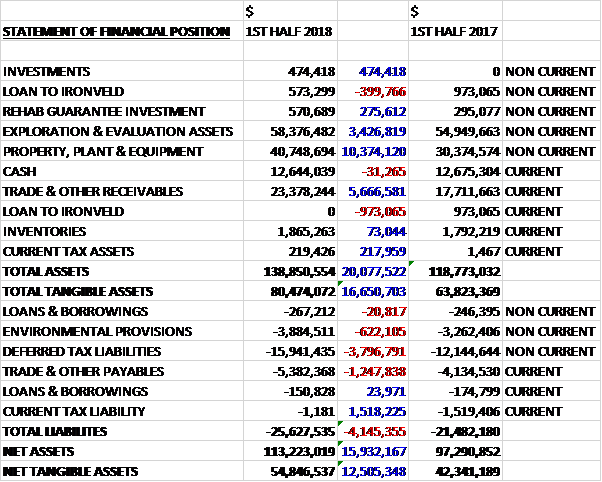

When compared to the end point of last year, total assets increased by $20.1M driven by a $10.4M growth in property, plant and equipment, a $5.7M increase in receivables and a $3.4M growth in exploration and evaluation assets, partially offset by a $1.4M decrease in the loan to Ironveld. Total liabilities also increased during the period as a $1.5M fall in current tax liabilities was more than offset by a $3.8M growth in deferred tax liabilities and a $1.3M increase in payables. The end result was a net tangible asset level of $54.8M, a growth of $12.5M over the past six months.

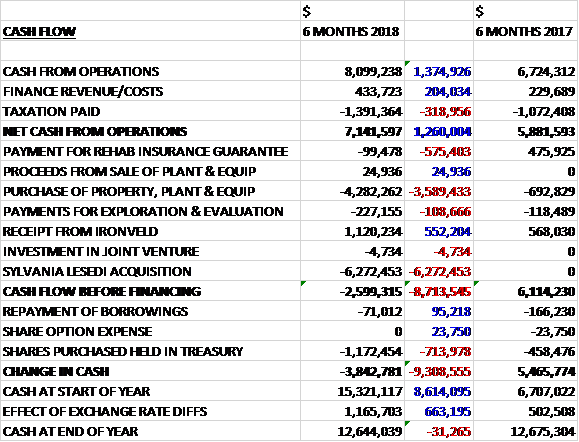

Before movements in working capital, cash profits increased by $1.4M to $8.1M. Finance revenue increased by $204K but tax payments increased by $319K to give a net cash from operations of $7.1M, a growth of $1.3M year on year. The group spent $4.3M on property, plant and equipment as a result of the first two Project Echo modules being commissioned along with $227K on exploration and $6.3M on the Lesedi acquisition but they brought in $1.1M from loan receipts from Ironveld to give a cash outflow of $2.6M before financing. The group also purchased $1.2M of shares to hold in treasury which meant that the cash outflow for the period was $3.8M and the cash level at the period-end was $12.6M.

The SDO produced 33,892 ounces in the period, despite the scheduled end of life closure of the Steelpoort plant in June. Strong performances were displayed by Tweefontein and Doornbosch and Lesedi contributed 1,458 ounces since acquisition.

The gross basked price for PGMs in the period was $1,057 per ounce compared to $883 per ounce for the period as a result of the improvement in Platinum and Palladium prices.

The operating faced two major challenges over the period. The first was the delay in the water use license authorisation by authorities at Millsell resulting in the delayed commissioning of the new tailings dam which impacted negatively on the available dump resource grade and re-mining strategy. The tailings dam is now in operation and the original re-mining site re-established since January with feed grades returning to planned levels. The second was lower than expected current arisings at Millsell and Mooinooi, as well as lower than planned ROM material from the host mine during Q2, which carried over into January, impacting negatively on PGM plant feed grades and production. The host mines are ramping up production again and feed tonnes and grades are normalising.

The introduction of new flotation technology at Mooinooi mid-Q1 together with flotation optimisation initiatives across operations assisted in the improvement of PGM recovery efficiency.

Cash costs for the SDO increased by 24% due to a 5% strengthening of the exchange rate, the lower production and higher dump re-mining costs at Millsell. The cost per ounce is expected to reduce going forward as Project Echo comes on stream in H2 2018.

Project Echo is proceeding well and the construction of the Millsell and Doornbosch MF2 modules was completed, the latter being commissioned a month ahead of schedule. Millsell MF2 was delayed by a month, however, due to the late completion of a power distribution upgrade by the local municipality. The Tweefontein MF2 has also been delayed due to the national power utility’s electricity supply infrastructure to the mining complex being constrained due to increased demand in the area.

Although this does not put the current Tweefontein operation at risk, it does introduce an element of risk to the MF2 module’s commissioning. As a result, a decision was made to delay the construction and commissioning of Tweefontein’s module until the power distribution infrastructure upgrade is complete. It is anticipated that it will now be commissioned by mid-2019, but the timing will be dependent on the completion of the power upgrade.

In November the group acquired Phoenix Platinum (renamed Sylvania Lesedi) for a consideration of $6.3M. Due to the close proximity of Lesedi to the group’s existing operations and similar process and business model, certain synergies are expected to be achieved. In the two months since acquisition, the business contributed profit of $7K.

Since integration, the primary focus has been on increasing plant production volumes, improving feed stability, feed grade and recovery efficiency to assist with production, and also to implement action plans to reduce overall production costs. Current initiatives include the application of Sylvania’s operating model in order to improve PGM ounces and to reduce operating costs; with the operation already benefiting from the SDO’s shared management teams; mass pull optimisation strategy has been implemented in order to improve PGM recovery efficiencies in the flotation circuit.

Plant feed tonnes and PGM feed grades have increased since December through a combination of plant de-bottlenecking and resource scheduling. The outsourced plant operation and maintenance contract was terminated in December which should result in significant savings. The improved quarterly PGM ounce production was a result of higher PGM plant feed tonnes, grade and recovery efficiency, especially during December.

Going forward, during the next half of 2018 the group remains focused on delivering on production guidance. Given the challenges in the past quarter, the board believe it necessary to revise the production guidance to between 71,000 ounces and 75,000 ounces, however.

At the current share price the shares are trading on a PE ratio of 7.8 which grows to 9.1 on the full year consensus forecast.

Overall then this was a bit of a mixed period for the group. Profits increased, net assets grew and there was a higher operational cash flow. There was no free cash generated but this was due to the acquisition. This good financial performance is entirely due to the increase in the price of platinum and related products. Offsetting this, the operational performance suffered from a delay in the water use license at Millsell and lower arisiings at both Millsell and Mooinooi. Both issues have now been rectified but the latter one will also affect results in Q3.

In addition, there have been delays in the commissioning of MF2 modules due to local electricity supplies and all of these issues have reduced the predicted production volumes. With a forward PE of 9.1 the shares are not as cheap as they once were but arguably still hold some value at these levels. I will continue to hold for now but will keep an eye on the platinum price.

On the 30th April the group released a trading update covering Q3. Overall the SDO delivered 16,857 ounces in the quarter, a decline of 3%. Revenue generated increased by 3% to $14.5M on the back of stronger sales prices and the group achieved a net profit of $1.1M. Group cash costs increased 10% in ZAR terms due to lower PGM ounces produced in January.

January was a particularly difficult month due to the impact of delays with a licence at the Millsell tailings facility. When the permissions were eventually received to use the new facility, nearly barren waste slime on top of the dump had to be processed first. Once they migrated down into the higher grade feed the project started generating increased ounces, resulting in March being the highest ever ounce production.

The PGM production is 2% lower than in Q2 after a challenging start in January, however the monthly production trend improved steadily throughout the quarter. Lower PGM feed grades at Millsell and Mooinooi during December and January and the decision to delay the construction of the Tweefontein MF2 module due to power supply constraints necessitated the production guidance revision during the quarter, which is now between 71,000 ounces and 75,000 ounces for the full year.

The basket price increased by 7% to $1,141 per ounce which mitigated the impact of lower production. Cash generated from operations before working capital movements was $2.9M with net changes in working capital amounting to an increase of $6.4M. An amount of $2M was spent on capex projects and the impact of forex fluctuations on cash held was $2.4M.

On the 31st July the group released a trading update covering Q4. After the record monthly production achieved in March, the SDO again delivered new consecutive production records of around 6,650 ounces and 7,400 ounces for May and June which generated a new record quarterly production figure of 20,278 ounces.

Whilst plant feed grade was marginally lower, higher plant feed tonnes, which were up 14%, and improved chrome yields enabled higher feed grades to the flotation which, together with a 7% improvement in recovery efficiencies contributed to the higher production. The higher plant feed tonnes resulted from improved plant utilisation and stability at Millsell, Mooinooi, Doornbosch and Tweefontein with the latter achieving higher PGM feed grades and recovery efficiencies. At Lesedi, they were slightly lower, however.

In terms of the first modules of Project Echo commissioned at Millsell and Doorbosch earlier in the year, the PGM recovery efficiencies at both operations improved significantly, contributing towards the overall improvement. The SDO cash costs in ZAR terms decreased by around 5%, assisted by higher production. In USD terms they decreased by 10% to $553 per ounce due to the additional impact of a weakening of the Rand.

While the newly commissioned Doornbosch MF2 has been performing as expected, the Millsell module experienced some challenges during the quarter with higher than anticipated wear rates on equipment associated with the new technology selected, which impacted on plant stability and recovery. This is currently being resolved with the supplier and should have a positive contribution going forward.

With the delay in the execution of the Tweefontein module, the module for Mooinooi is being fast tracked to counter the delays in order to mitigate any impact on production and sustain group production profiles. The relocation of the redundant Steelpoort chrome circuit to the Lesedi operation is planned to improve chrome removal ahead of flotation, which will enable chrome removal ahead of Lasedi’s PGM plant and contribute towards higher PGM feed grades as per the standard model employed at existing operations in the group.

The basked price in the quarter was $1,167 per ounce, a 2% improvement. Although the platinum and palladium prices dropped, the rhodium price continued to increase. With the basket price remaining fairly flat, the 39% increase in revenue is a result of increased production and forex movements. The group cash balance at the period-end was $14M, a $3.4M decrease in Q3.

The group has not pursed its exploration activities during the quarter.

Things seem to be going fairly well here operationally, although the fall in platinum price should be watched. I am considering buying back in here.