T Clark is a UK-based building services contractor. Their principle activities are the installation of electrical, mechanical and ICT services nationwide. They also provide a range of associated products and in-house manufacture, design and engineering services. Clients include global media, financial services and manufacturing organisations along with main contractors in the construction industry, house builders and a range of public and private sector businesses. The group’s business areas are M&E contracting; transport, a rail and airport division; mission critical, a specialist resource for critical data and power; intelligent buildings; facilities management; residential and hotels; design and build; manufacturing and green technologies.

The Design and Build division, based in Colchester, was started this year but the M&E Contracting division is still the core, representing about two thirds of future work. The Facilities Management business involves maintenance and the care of offices, commercial buildings, and institutional buildings such as hospitals, schools and arenas. In particular, the group have facilities management operations serving some of the biggest names in UK engineering and the nuclear industry

Revenue from the rendering of services that do not fall to be accounted for as construction contracts is accounted for by reference to the stage of completion of the relevant contract, determined by reference to the proportion of costs incurred. For construction contracts, when the outcome of the contract can be estimated reliably, revenue and costs are recognised by reference to the stage of completion of the contract activity at the reported date, measured based on the proportion of contract costs incurred for the work performed to date relative to the estimated total contract costs. The recognition of this revenue is a source of uncertainty due to the difficulty of forecasting the final costs to be incurred on a contract in progress and the process where applications are made during the course of the contract with variations, which can be significant, often being agreed as part of the final account negotiation.

T Clark has now released its final results for the year ended 2014

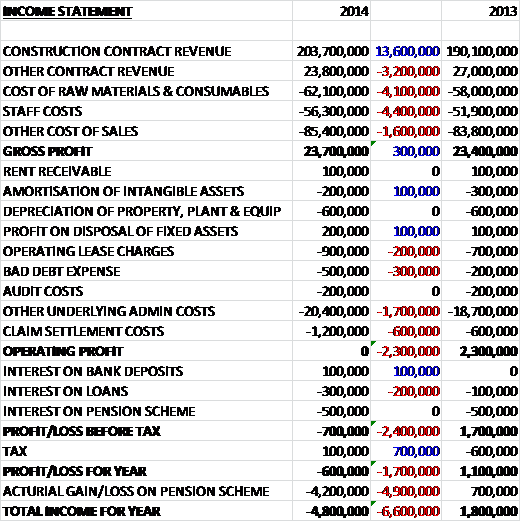

Revenues increased year on year as a £13.6M increase in construction contract revenue was partially offset by a £3.2M fall in other contract revenue. Raw Material costs increased by £4.1M and staff costs increased by £4.4M so that gross profits were some £300K ahead of last year at £23.7M. We then see an increase in underlying admin costs and a £1.2M charge for claim settlement costs (double that of 2013) to give an operating profit of zero. After interest paid on loans and the pension scheme plus a small tax rebate the loss for the year stood at £600K, a negative swing of £1.7M when compared to last year.

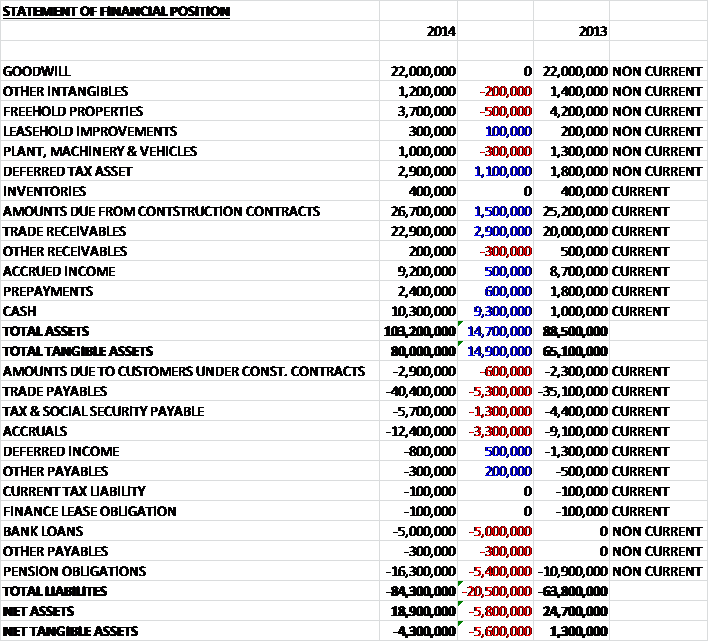

When compared to the end point of last year, total assets increased by £14.7M driven by a £9.3M growth in cash levels, a £2.9M increase in trade receivables, a £1.5M increase in amounts due from construction contracts and a £1.1M growth in deferred tax assets (relating to the re-measurement of the pension scheme). Total liabilities also increased during the year due to a £5.4M increase in pension obligations, a £5.3M growth in trade payables, a £5M increase in bank loans and a £3.3M growth in accruals. The end result is a £5.6M fall in net tangible assets to a negative £4.3M which looks rather weak. There was also £3M of operating leases outstanding at the year-end, half of which are due within the next year.

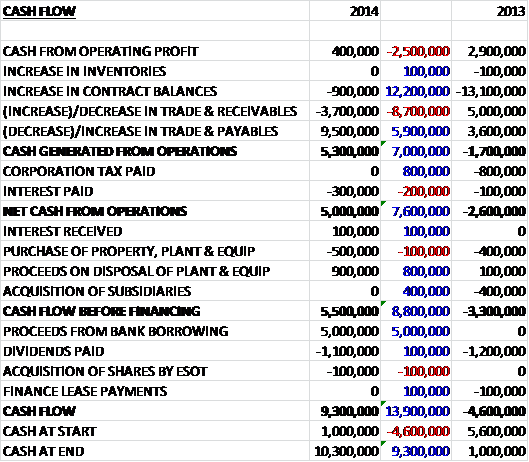

Before movements in working capital, cash profits fell by £2.5M to just £400K. A large increase in payables, however, meant that the net cash from operations stood at £5M, an increase of £7.6M year on year. The group then actually made more money selling its tangible assets than buying them to give a free cash flow of £5.5M. The group used £1.1M to pay the dividends but curiously took out a loan of £5M to give a cash level of £10.3M at the year-end. The draw-down of the loan seems rather strange given the amount of cash supposedly on the balance sheet – I can think of two likely explanations – either the company is eyeing up an acquisition, or more likely in my view, that cash level at the year-end is a bit misleading and the group is going to have to pay those increasing payables which means the cash at the year-end is probably significantly higher than at other times of the year.

The underlying loss from operations at the Southern division was £1.1M, a negative swing of £2.1M year on year. This loss was due to a substantial loss on the Mission Critical contract highlighted last time on which the group reached a negotiated settlement that has now been fully settled. If this one contract is removed, the region would have delivered a significantly higher profit than in 2013. Elsewhere in the region, competition has remained fierce, particularly in the first half of the year with clients delaying procurement to secure ever lower prices. This trend began to reverse towards the end of the year with many of the region’s offices benefiting from repeat work. The last few months have also seen significant wins for the combined M&E business in London, securing significant revenue into 2015 and beyond.

The underlying profit from operations at the Northern division was £1.6M, a decline of £200K when compared to last year and this represented a decline in profit margin from 4.8% to 3.2%. The fall is apparently due to positive final account settlements that occurred in 2013 on a number of contracts undertaken in previous years. Despite this excuse, growth seems to be quite slow in the region even though it benefited from strong client relationships and repeat business. The underlying profit from operations at the Scottish division was £600K, an increase of £400K when compared to 2013 as improving commercial and IT revenues were added to the continuing strong performance in the residential sector. There were additional costs of £100K during the year as the business defended a multitude of adjudication claims brought by a sub-contractor. The underlying profit from operations at the property division was £300K, an increase of £100K year on year.

The UK economy as a whole saw many signs of substantial recovery in 2014 but in the construction sector such signs remained sparse until late in the year and there was no significant surge in demand. Margins, therefore, remained under pressure and despite the record order book, there was no margin improvement until Q4. There are significant signs that the London commercial market is picking up with contractors looking to build their major schemes now. In the normal cycle, it is expected that regional markets will pick up a little later than the market in the capital.

During the year the group has worked on a number of contracts but some stand-out ones include mechanical and electrical engineering contracts at the Walkie Talkie building, BBC White City, Bloomberg London, building E at BP Sunbury, Deutsche Bank, Imperial Tobacco HQ in Bristol, Selfridges, South Bank Tower and Transforming Tate Modern. There were also contracts at Aberystwyth Student Accommodation, Bank Station Capacity Upgrade, De Vere Gardens, Silwood Sidings, US Air Force Bases Mildenhall and Wyton and the Victoria Station upgrade.

One of the main strategic developments this year was the complete integration of the TClark DRG large scale mechanical operation with the main business which was matched by a series of major M&E contract wins and the appointment of DGR MD and founder Danny Robson to the main board. These actions open up the large scale M&E contracts in London and other UK markets.

During the year the group launched their Design and Build operation which opens up another new revenue stream for the group in a strategically attractive area. The business now has a maiden £11M order book and is slightly ahead of its planned growth target. In the coming year the group is planning on bringing all of its local businesses together within one UK operating company in four new regional operations which includes London and the South East, Central and West, the North and Scotland. This structure aims to keep the valuable local presences and connections to the local market but also to maximise efficiency, the capability to cross-sell and share resources and knowledge both regionally and nationally. It is expected that this project will be complete by the end of 2015.

The Design and build division made revenues of £1M during the year and has a forward order book of £11M. The core M&E division made revenues of £148M and has a forward order book of £204M; the Intelligent Buildings division made revenues of £5M and has a forward order book of £4M; the Facilities Management business made revenues of £19M and has a forward order book of £18M and is a particular growth area for the group; the Transport division made revenues of £18M and has a forward order book of £31M and hopes to break into the airport market from their successful rail operation; the Mission Critical business made revenues of £8M and had a forward order book of £6M; and the residential and hotels business earned revenues of £30M and has a forward order book of £26M.

The group is market leader in the large scale electrical engineering sector. During 2014 margins remained tight but going forward it is expected that better margins will be available as clients seek to lock in the group’s resources as skills shortages loom. In the large scale mechanical engineering sector, the group made a series of major contract wins and the board thing that this is an area that represents a good growth opportunity. There has been a strong performance from the transport and residential businesses. The board see HS2 and other major rail projects as an opportunity for further growth in the transport sector.

During the year the Scotland Green Technologies and Renewable energy department handed over, in partnership with Springfield Properties, the first nine Air Source Heat Pump installations to Muirhouse Housing Association in Edinburgh. These pumps work by using the latent heat in the outside air to deliver heating and hot water to homes using electricity only to run the fans and compressors. At the school Ask Putney, their package included site-wide mains and sub-mains distribution, complete internal and external lighting systems, site-wide data, fire detection voice alarm, CCTV, access control, metering and maintenance of systems. Mechanically they provide natural gas site wide distribution, air-con, BMS and smoke extraction systems, full public health services, above ground drainage, rainwater installation, portable drinking water and domestic water services.

The group also completed a major animal management and vet services building working with Midas Construction on a full mechanical and electrical design and build. They provided everything from PV installation to fire and intruder alarm design and installation. They also completed a turnkey design and build project for Springfield Fuels, a prefabricated Mask Air Compressor Plant. It is a world class nuclear fuels facility and T Clark was engaged to design and install a mask air compressor unit to provide breathing air across the site. The plant was to be prefabricated to that it could be moved in future to a different location if necessary and the air supply was to be delivered to various points across the site.

T Clark has recently, working with global scanner manufacturers Siemens and GE, developed a very high quality in-house design and manufacturing operation for scanner controls. These scanners are installed in every hospital across the UK. In November the group announced over £7M if major new project wins in London, all starting in 2015. These included Beaufort House in Hendon, London Wall Place, One Angel Court, Principal Place, Bishopsgate and Rathbone Square. In the transport division, wins over the past year and a half meant that their order book stretched ahead to 2022. The work with Costain at Waterloo Station is the first project with this major contractor and around 40% of the contract wins in the division are for full design and build contracts.

In December the team in Huntingdon concluded a six month programme to deliver a full building services package at Peterborough stadium including mechanical, electrical and ICT works. On the electrical side they installed general power and lighting plus emergency lighting throughout with CCTV, fire alarm, TV, data installation to all floors, local electric and water heaters, and a photovoltaic system on the roof. They also delivered a lighting protection system to the complete building and external lighting. On the mechanical side, they installed a new water main, a rainwater harvesting system, net controls and pipework to the existing pitch irrigation system, new water tanks, drainage, a complete refrigerant and heating cooling system and a full ventilation system.

This year there was a £1.2M exceptional claim settlement cost. A subsidiary business was one of a number of parties that were subject to a substantial damages claim for work carried out in 2007 before it was acquired by the group. Damages were awarded against the company, the bulk of which were covered by the insurers but following an unsuccessful appeal, the apportionment of costs exceeded the insurance cover in place which resulted in a negotiated settlement that cost the group £700K.

Last year the company settled a sub-contractor claim against the group for work carried out in previous years which resulted in costs of £500K. A further £400K in costs were incurred this year in seeking to reach a settlement of costs and interest in respect of this claim and a potential counter claim by the company against the sub-contractor. Proceedings are ongoing in this matter but the directors do not believe there will be any significant additional costs to the group. In addition, a sub-contractor has brought a number of adjudication claims against a subsidiary in respect of a single contract. The company has so far been successful in defending these claims but has incurred costs of £200K in doing so (£100K of which were incurred last year).

The group has an £8M overdraft facility with Natwest which attracts interest of 2.75% above base rate and at the year-end none of this facility was being used. In February the group arranged a £5M committed three year revolving credit facility with Natwest which incurs interest of 3% above LIBOR on drawn facilities and 1.5% on undrawn balances. This facility includes some financial covenants and while the group was compliant with its obligations at the year-end, this was not the case during the whole year. The group breached its obligations by failing to notify the bank in a timely manner of an award of damages against them but they managed to obtain a waiver of this breach – it sounds like it might have just been an oversight.

Also, following the settlement of a contractual dispute in the group’s mission critical division which resulted in the group recognising a significant loss on the contract concerned, the group informed the bank that it would be unable to meet the interest cover covenant and requested in advance a waiver of this covenant. The terms of the facility were subsequently varied before the year-end to remove the interest cover test for the last quarter – this is potentially more serious in my view and reinforces the fact that the group is actually in a bit of bother over its finances despite the apparent large cash pile they are sitting on.

Last year one customer accounted for 18% of total revenues but this year no customers accounted for more than 10% of sales. As can be seen, the group seems to be having a bit of trouble with its pension scheme. The deficit of £11.5M represents a funding level of just 68% and has been significantly impacted by the fall in bond yields. A deficit reduction plan has been agreed with the regulator which involves making additional contributions and providing the security in the form of a contingent asset over the group’s property portfolio worth £3.1M with the aim of eliminating the deficit by 2029. Employer contributions amount to about £1.1M per annum at the moment which is fairly substantial given the lack of profits being made here. .

With a record order book of £300M and early signs of margins beginning to improve, the board are looking to 2015 with confidence.

The underlying PE ratio currently stands at a massive 66.2 but this falls to a more reasonable 12.8 on next year’s consensus forecast. After an unchanged total dividend for the year, at the current share price the shares are yielding 4.1% which remains the same for next year’s forecasted pay out. The group has a net cash position of £5.2M at the year-end compared to £900K at the end of last year.

Overall then, this has been a rather difficult year for the group. There was a loss recorded, which seems to have been as a result of various contract disputes and one substantially loss making contract in the mission critical business. Net assets also fell and the increased pension deficit and increase in payables took their toll. At first glance the cash flow looks pretty decent with increased net operational cash flow and plenty of free cash but we can see that this was entirely due to the large increase in payables which are going to have to be paid at some point, and the underlying cash profits actually fell year on year. It is also a bit concerning that a covenant on the debt had to be waived during the period and that pension deficit is starting to look a little menacing.

Operationally, the Southern division is suffering from that loss making contract and things also seem to be rather slow in the Northern division, although in Scotland the group is making increasing profits. The group is obviously very cyclical and dependent on the UK construction sector and this, in London at least, finally seems to be picking up which should bode well for the coming year if the group manages to stay clear of further contract disputes. The forward PE ratio looks about right and the yield of 4.1% is certainly worth considering but although I do feel this should be a much better year for the company I have a few niggling doubts about how well they can take advantage of the increased opportunities.