Tangent Communications has now released its final results for the year ending 2015.

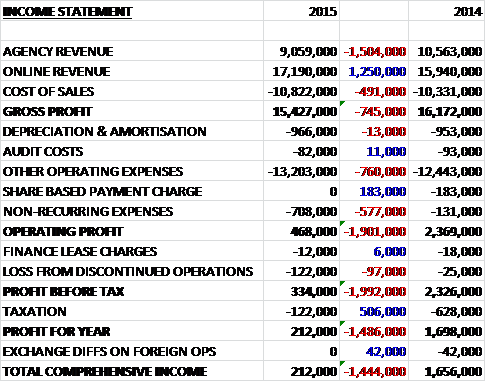

Overall revenues fell as a £1.25M increase in online revenue was more than offset by a £1.5M decline in agency revenue. Cost of sales then increased to give a gross profit some £745K lower than last year. There was also an increase in underlying operating expenses as well as a £577K growth in non-recurring costs relating to the downsizing of Tangent Snowball, rationalising Ravensworth and relocation expenses, which left the operating profit at just £468K, a decline of £1.9M. This fall widened to £2M when the loss from the discontinued operations is taken into account and after a much smaller tax bill, the profit for the year stood at just £212K, a decline of £1.5M when compared to 2014.

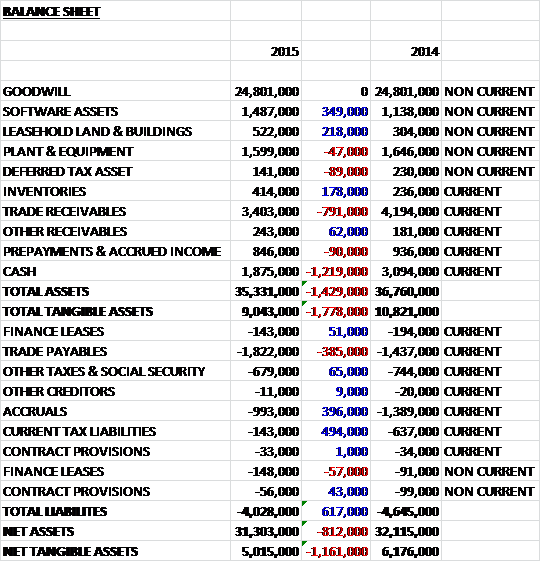

When compared to the end point of last year, total assets fell by £1.4M driven by a £1.2M decline in cash levels and a £791K decrease in trade receivables, partially offset by a £349K growth in the value of software assets, a £218K increase in land & buildings, and a £178K increase in inventories. We also see liabilities fall year on year as a £494K decline in current tax liabilities and a £396K fall in accruals were partially offset by a £385K increase in trade payables. The end result is a £1.2M decline in net tangible assets at £5M. It is worth noting, however, that the group took out a large operating lease (probably relating to the relocation) and leases now represent £4.1M that is not included on the balance sheet which looks rather less robust when this is taken into account.

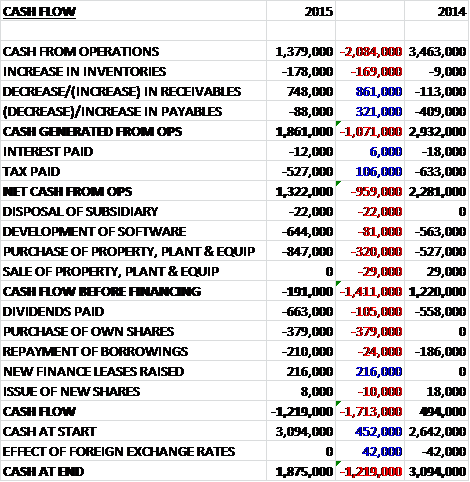

Before movements in working capital, cash profits were some £2.1M lower than in 2014, but this was improved somewhat by a decrease in receivables due to a higher proportion of customers paying upfront and online with credit and debit cards, before a lower tax bill meant that net cash from operations was nearly £1M lower at £1.3M. This was not quite enough to cover capital expenditure of £847K of intangible assets and £644K of intangibles so there was no free cash flow this year. The group then paid £663K on dividends and £379K of cash it barely had on the purchase of its own shares with the end result being a £1.2M cash outflow to leave a cash level of £1.9M at the year-end with overdraft headroom of £1M.

Overall online print sales grew by nearly 8% to £17.2M which was a slower increase than anticipated and profits fell by £1.3M to £454K. Measures have been taken to rationalise the online print business with a focus on driving sales through the growing printed.com platform which will involve the transfer of the goodprint business under the printed.com umbrella. In line with this approach, going forward the group will report the performance of printed.com, goodprint and Ravensworth in a combined business segment. Sales at printed.com increased by 25% to £7.6M with new customers and an increase in customers who returned year on year providing the basis for the growth.

Sales at goodprint declined with business card sales down 34% to £2.1M as the market became increasingly competitive. The customer facings brands under goodprint are now being merged into printed.com which should reduce costs and increase efficiency. Ravensworth benefited from a strengthening of the residential property market in the early part of the year but saw it cool significantly in the latter part of the year with sales from October dropping 20% below the trend set in the first eight months. This impacted profitability as the business was taken by surprise before it could fully adjust to the changing market conditions. Sales in the year as a whole were up 12% to £7.5M but clearly this was due to the strong performance in the first half of the year offset by the weakness in the second half.

Profit from Agency operations fell by £700K to £424K. Sales at Tangent Snowball fell by 19% to £6.7M due to budget cuts from two key clients at the start of the year and the divestment of the Australian operations. The business has reduced headcount during the year and has now started to see the benefits of operating with a leaner team. Apparently digital marketing remains in demand but competition and an increase in in-house skills are having an impact on the business. New business was slower than targeted to relieve the reliance on a few large clients and senior management changes have now taken place within the division. Sales at Tangent on Demand were flat year on year at £2.4M.

After a review of the operational structure, the group has reduced headcount which led to restructuring and redundancy costs of £590K. In addition, all of the London based businesses have been relocated during the year which resulted in a one-off expense of £120K. The reduction in operating profits meant that the headroom with regards goodwill impairment was reduced so I would not be surprised to see a write-down at some point in the future. I don’t generally include Goodwill in my analysis of a balance sheet, though, so this has limited effect as far as I am concerned (although the reduction in predicted operating profit going forward is clearly a concern). Of the group’s capital expenditure this year, £570K was spent on printing equipment and IT, £280K was spent on leasehold improvements and £640K was spent on software. Investments in equipment and IT is likely to remain flat going forward but should reduce in software and cease entirely with regards to leasehold improvements, so capital expenditure should reduce in 2016.

The group has various financial and non-financial KPIs with most of the financial ones worsening year on year with employment costs as a percentage of sales up, operating margins down and EPS down. One highlight though was the increase in cash conversion to 158% reflecting the higher proportion of customers paying in advance via credit and debit cards on the website. The highlight of the non-financial KPIs is staff retention with staff turnover improving to 2%, which seems remarkably low and suggest the company is a good place to work despite the disappointing financial results.

There does seem to be a large amount of options granted to the directors with nearly 10% of the total shareholder equity in the form of options, some of which have an exercise price of zero, which I think is not really on. During the year the group completed the disposal of its 81% holding of Tangent Snowball in Australia which resulted in a loss of £120K, approximately half of which related to the fees of the disposal and half relating to the operating loss of the subsidiary while it was part of the group.

The new year has started in line with expectations but profits are expected to be lower year on year in the first half of 2016. Despite the challenges, however, the board believes there is a sizeable market to exploit and demand for the group’s products remains but whether the group can capitalise on these opportunities remains to be seen.

At the end of the year, net cash stood at £1.6M, a reduction of £1.2M year on year. There is prudently no final dividend this year and one is not expected next year either. At the current share price the shares trade on a very expensive P/E ratio of 43.7 but this reduces to a much more reasonable 10.8 on next year’s consensus forecast.

Overall then, this was clearly a poor update from Tangent. Profits fell drastically, net assets declined and the balance sheet is looking rather weak, being loaded with Goodwill that has had its impairment headroom lowered. Operating cash flow fell despite an increase in advance payments and there was no free cash flow at all, although the cash pile should be sufficient for the year ahead and capital expenditure should be a bit lower this year. Operationally, the only business that is doing well is Printed.com with the second half performance at Ravensworth particularly disappointing. It seems that for the bulk of the business that there is just too much competition and Tangent may not be able to compete. The forward P/E ratio does look good but with management flagging up lower H1 profits this year and no dividend on the cards for 2016, I think I will be avoiding these shares for now.

As things stand, this is not a chart that I can invest in.

On the 23rd June the group released a statement covering trading in Q1. Apparently trading was in line with expectations but forecasts for the rest of the year have been lowered due to Tangent Snowball not winning enough new business. As a result, it is anticipated that the outcome for the group for the full year will be below expectations, although net cash at the year-end is expected to be £2M. More specifically, management expects profits at Tangent Snowball to be £500K below expectations and as a result Tangent Snowball CEO Steve Grout has been dismissed and replaced by Tim Green who has taken over day to day responsibility for the agency business. In addition, the business will be seeking to hire new senior sales staff.

The print business performed in line with budget in Q1 and performance is forecast to continue in line with expectations. The rationalisation of the print business continues and the full goodprint proposition is now available on printed.com. This is yet another profit warning and it seems pretty difficult to justify an investment in this company.

On the 30th June it was announced that CFO Jamie Beaumont and non-executive director Nigel Kissack had purchased 250,000 and 340,172 respectively which represents £7,500 and £9,185. These are their first share buys so I am not getting too excited about this.