Paypoint has now released its interim results for the year ending 2016.

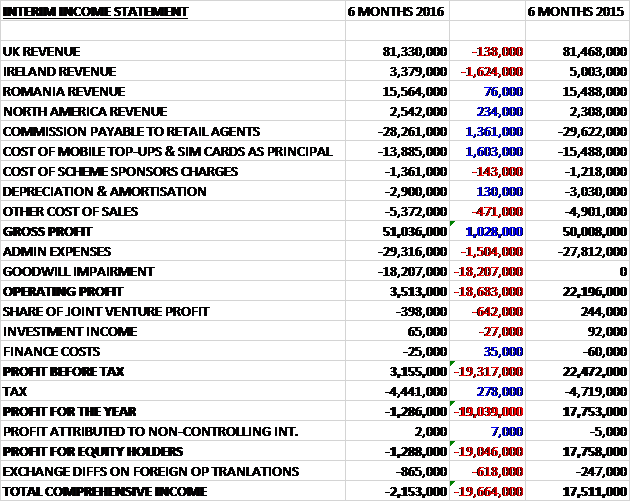

Revenues fell when compared to the first half of last year as a £76K growth in Romania revenue and a £234K increase in North America revenue was more than offset by a £1.6M decline in Ireland revenue and a £138K decrease in UK revenue. The commission payable to retail agents fell by £1.4M as the group has adjusted the share of commission with its retailers in response to competitor rates, and the cost of mobile top-ups and sim cards declined by £1.6M which meant that gross profit was £1M above that of last time.

Admin expenses grew by £1.5M though, due to £700K of restructuring and legal costs related to the sale of the Mobile and Online Payments businesses and the HMRC ruling which increased irrecoverable VAT which accounted for £1M (the rate of increase in admin expenses is expected to slow in the second half of the year), and after the £18.2M goodwill impairment, the operating profit was £18.7M lower. There was a loss from the joint venture, a negative swing of £642K but tax fell which meant that the loss for the first half of the year came in at £1.3M, an adverse movement of £19M year on year (including the £18.2M goodwill impairment).

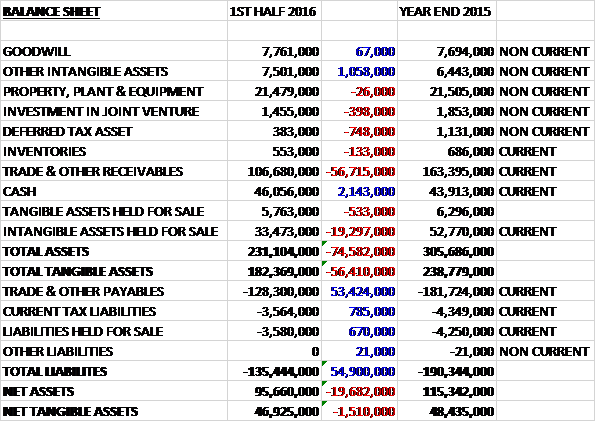

When compared to the end point of last year, total assets fell by £74.6M driven by a £56.7M decline in receivables and a £19.3M decrease in intangible assets held for sale, partially offset by a £2.1M growth in cash and a £1.1M increase in other tangible assets. Total labilities also declined during the period due to a £53.4M fall in payables. The end result is a net tangible asset level of £46.9M, a decrease of £1.5M over the past six months.

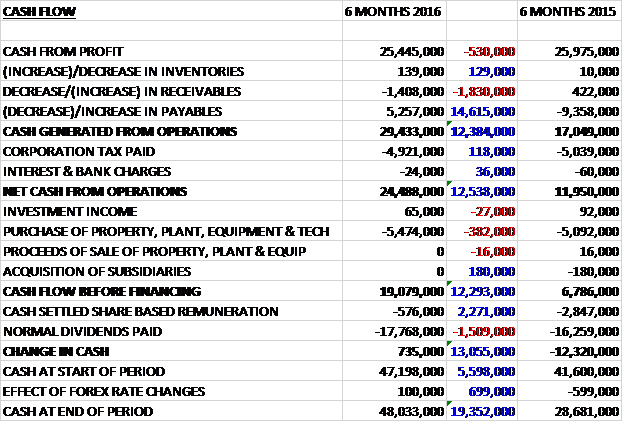

Before movements in working capital, cash profits fell by £530K to £25.4M. An increase in payables compared to a large decrease in the first half of last year meant that net cash from operations came in at £24.5M, a growth of £12.5M year on year after a tax payment of £4.9M. The group spent £5.5M on property, plant and equipment relating to IT infrastructure, development for new products, terminals, ATMs and prepaid energy card and key readers for the software version of the terminal that can be loaded onto retail till systems, to record a free cash flow of £18.5M (after we include the share based remuneration). This was mostly spent on dividends which meant that the cash flow for the six month period was £735K and the cash level of the period-end was a hefty £48M.

Overall results for the first half were in line with management expectations with operating profits decreasing by 5% due to investment in the Mobile business and lower revenues in Online Payments. The retail networks produced net revenue growth of 3.5%. In the UK there were 1.2% fewer prepaid energy transactions than last year and in particular the number of prepay electricity transactions was lower as consumer demand appears to have reduced. In Romania, bill payment transactions have grown 15.6%, as the group continued to add new clients and increased their market share. Retail services transaction growth was 21.2% and net revenues were up 16.2% to £15.1M. In the UK, mobile top-up transaction volumes have continued to decline, whereas in Romania the volume of transactions has increased.

Bill and general transactions were ahead of the same period of last year as a result of a 15.6% increase in Romanian bill payment transactions. UK and Irish bill and general transactions were down 1% on last year due to lower transactions in prepaid electricity. An apparent decrease in consumption together with the effect of higher average transaction values exceeded the impact from meter growth. Although not material to these results, the multi-channel payment solution continues to grow strongly and sales to a further five clients have been agreed, including the first big six client, and it is attracting interest from other sectors. The strong growth in Romania, where the group processed 29.1M transactions, was the result of increasing market share to 21.3% from 18.8% and the addition of new clients. Growth in net revenue of 1.2% to £26.2M slightly exceed that of revenue, helped by changes to the retail terms made in response to competitor rates.

Top up transactions decreased from last year as a result of the continued decline in mobile top-up volumes in the UK and Ireland of 13.8%. This fall was only partly offset by an increase in other top-up transactions and Romanian mobile top-ups. The reduction in top-up transaction value was lower than that of transaction numbers as the average value of mobile top-ups increased which helped mitigate the reduction in net revenue to a 5.2% fall to £11.1M, as did the increase in other top-ups.

Retail services transaction volume has increased across all products. ATM transactions increased by 27%, credit and debit transactions by 19.2%, money transfer transactions by 7.2%, SIM cards by 45% and parcels by 18.1% over the same period last year. A higher average credit and debit transaction value and money transfer transaction value has driven an increase in total transaction value in excess of transaction volume. Strong net revenue growth of 16.2% to £15.1M was driven by increases in parcels, ATM transactions, credit and debit, and income from broadband enabling faster terminal transactions.

Collect+ is the market leading third party click and collect service and its parcel returns activity also continues to grow strongly with transactions up 18.1% to 9.9M. Within the consumer send market, there continues to be substantial price competition and consequently the management team has focused on developing click and collect along with returns. The group continue to discuss with Yodel the future of the joint venture and the proposed increases in charges put forward by them. A portion of these charges have been allowed pending the outcome of these discussions which has caused an adverse impact on profitability with losses of £797K recorded compared to a profit of £487K last time. They expect to be able to report on the conclusion of these discussions by the time of the full year results announcement.

In Mobile and Online, transactions increased by 22.2% with payment transactions of 62.3M up 22.7% and parking transactions of 23.6M up 20.9%. Parking transaction growth was driven predominantly by the continued increase in consumer adoption in existing clients and the full roll out of parking payment services in Paris. The increase in online payment transactions stemmed from existing merchants. Net revenues decreased by 5.7% to £7M reflecting a decline in payment revenues due to larger merchants benefiting from lower pricing on core payment processing transactions, offset by strong growth in the mobile business in North America.

The business has continued to add parking contracts with councils and parking authorities as they provide them with a more cost effective method for collecting parking charges. It has fully rolled out the parking payment services in Paris during the period, a contract has been signed to service a number of London Underground car parks as part of a TFL initiative and during the period, Brighton local authority ended its use of parking meters.

In online payments an increasing number of clients are processing on the new Advanced Payments platform and the sales of the two new licensed products, Cashier and Cardlock have started to accelerate. Cashier enables merchants to offer a customised payment experience for their online or mobile customers and also has a built in capability to allow customers to store multiple cards whilst Cardlock removes card data from client websites as soon as it has been entered, securing it remotely in Paypoint systems. A further two products have been launched during the period. Mobile SDK makes it easier for a merchant to provide an improved payment experience in an app and Fraudguard5 is an enhanced version of the successful Fraud Management product which introduces new analytical capabilities.

Terminal sites overall have increased by 848 to 38,389 since the end of last year. The group continue to roll out their PPoS integrated solution to retailers which combines a virtual terminal with a plug in reader, to provide their service at lower cost. As well as enhancing service to retailers, this allows the group to redeploy the old terminals for use in Romania. In addition to the 7,717 PPoS solutions, there were 11,627 broadband enabled terminals at the period-end. In Romania, they increased their sites by 224 to 9,458 over the same period but the number of internet merchants fell by 645 largely through churn of low volume merchants. The number of sites offering the Collect+ parcels service increased by just 64 to 5,895, constrained during the discussion of Yodel’s proposed increase in charges to the joint venture.

The group have developed a multi-channel product in UK retail, aimed at addressing the payment challenges faced by utilities as a result of the government mandated change to smart meters by 2020, which builds on the existing online payment solutions for prepaid meters. This product has already been sold to six clients in the energy sector including the first big six energy client and has attracted interest from other sectors, including housing.

The group have made progress with the sale of Mobile, which is expected to complete before the end of the year but offers made for Online Payments are disappointing, reflecting the potential buyer’s uncertainty of the business’ success with new products which are at an early stage of their lifecycle. In view of the uncertainty of the eventual outcome, management have recorded an impairment of all the goodwill in the Online Payments business of £18.2M – it looks like they overpaid for that one then!

So far in the second half of the year, trading has been in line with management expectations and after a 14.5% increase in the interim dividend, at the current share price the shares are yielding 4.3%.

Overall then, this was a bit of a disappointing set of results in my view. Profits declined slightly if we ignore the goodwill impairment which seems to have been due to higher irrecoverable VAT and some restructuring costs, net assets declined and although operating cash flow was up, this was only due to an increase in payables and cash profits decreased year on year. The group is still very cash generative though and produced a lot of free cash – enough to cover the dividend.

There was a good performance in retail services with particularly strong growth in parcels, ATM transactions and credit and debit card services; while there was also a modest improvement in bill and general transactions due to growth in Romania partially offset by a decline in UK electricity prepayments. Top-ups continued to struggle due to the structural decline in UK prepay mobile phone top ups, mobile and online saw net revenues decline due to larger merchants getting lower prices, and Collect+ is starting to struggle due to the higher charges levied by Yodel – it appears they are trying to push through even greater charges in future too.

The sale of the mobile business should take place in the second half of the year that should bring in even more cash but it looks like they are struggling to find a buyer for the online payments business which is disappointing. The dividend yield here is pretty good, at 4.3% and covered well enough but the growth here does seem rather lacklustre.

On the 8th January the group announced the sale of its Online Payment businesses comprising Paypoint.net and Metacharge to Capita for a consideration of £14M satisfied in cash. They will update on the sale of the Mobile Payments business in due course.

On the 28th January the group released an interim statement covering Q3. Retail services have grown strongly, the new terminal is in pilot in the UK and they have made good progress in developing their core epos software. Since the end of the quarter, they have also completed the sale of their online payments business. This progress has been partially offset by the unseasonably warm weather, however, which has impacted on energy consumption, and an extension of the additional costs in Collect+ along with a delay in the sale of the mobile payments business. The board aim to resolve the Collect+ JV agreements and complete the sale of their mobile payments business by the year-end.

Net revenues in Q3 were up 1.8% to £35M year on year. There was strong growth in retail services of 22.7% and mobile & online of 9.6%, offset by a 13.7% decline in top-ups and a 2.4% fall in bill & general, the latter mainly due to lower energy consumption. The previously reported adverse VAT ruling from HMRC and the warm weather has slowed improvement in the results.

In UK and Ireland retail, retail service transactions were up 14.3% but bill and general transactions were down 8.1%. Mobile top-ups continued to decrease as the prepaid mobile sector declined, partially offset by an increase in other top-ups. Retail sites in the region increased by 113 in the quarter to 29,044. In Romania, profitable growth continued. The group processed 15.3M bill payments in the period, up 11%. Top-ups increased by 6.2% and retail services by over 50%. They increased their terminal estate by 307 sites in the quarter to 9,765 and continued to add new clients.

At Collect+, volumes increased by 5% to over 6M transactions in the period with a record Christmas week of 638K transactions. The network continued to expand with an increase of 75 sites to 5,970 in the quarter. Discussions are ongoing with Yodel regarding the future of the joint venture and the proposed increase in charges put forward by Yodel. Some of these charges have been allowed pending the outcome of negotiations which has resulted in the joint venture generating a small loss.

In Mobile and Online, transactions increased by 37.6% to 50.2M with mobile payment transactions up 38% to 13.3M and online payment transactions up 37% to 36.9M. The online payments business was sold to Capita after the end of the period for £14.4M and they have continued to progress the sale of the mobile business.

Overall then, this is a bit of a disappointing. Whilst the group can’t be blamed for the warm weather, the continued decline of mobile top-ups is disappointing and it would be useful to know how much further this has to fall and how much profit that part of the business contributes. The Collect+ joint venture also seems to be an ongoing problem and has become a drag on the business. Aside from Romania and other geographical expansion it is difficult to understand where any further growth will come from but at the current share price this seems like an interesting value play and I am keeping it on alert.

On the 29 January it was announced that director Nicholas Wiles purchased 10,000 shares at a value of just under £80K to give him a holding of 35,000 so it seems he sees some value here too.

On the 4th February the group announced that non-executive director Steve Rowley stepped down from the board with immediate effect having spent the last seven and a half years in the role.

On the 5th February the group announced that director Giles Kerr purchased 7,500 shares at a value of just over £58K. This represents his maiden share purchase.