Telford Homes has now released their final results for the year ending 2014.

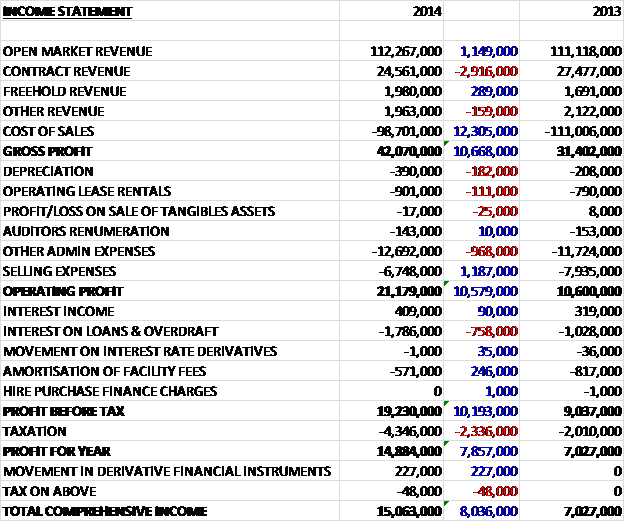

Overall revenues declined when compared to last year with a £1.1M increase in by far the largest sector, the open market, offset by a £2.9M decline in contract revenue. Cost of sales also declined, in part due to the lack of inventory write down that cost £1.9M in 2013, to give a gross profit some £10.7M higher than last year. We also see an increase in admin expenses, mainly due to higher employee costs in constructing increasing numbers of homes, counteracted by a decrease in selling expenses which are expensed as they occur and not necessarily when revenue is recognised when the homes complete (mostly relating to agent’s commission), so that operating profit is a similar £10.6M higher. There was a £758K increase in loan interest and a more than doubling tax bill to give a profit for the year twice that of in 2013 at £14.9M.

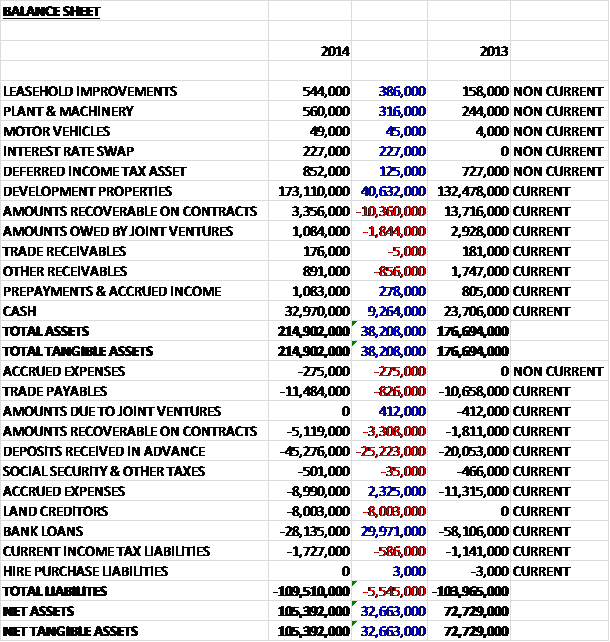

When compared to the end point of last year, total assets increased by £38.2M driven by a £40.6M hike in development properties and a £9.3M increase in cash, somewhat offset by a £10.4M reduction in amounts recoverable on contracts(occurring when costs incurred and profit exceed progress billing) and a £1.8M fall in amounts owed by joint ventures. Total liabilities also increased as a £25.2M increase in deposits received in advance, an £8M growth in land creditors and a £3.3M increase in amounts recoverable on contracts were mitigated by a £30M fall in bank loans and a £2.3M decline in accrued expenses. This all meant that net assets (there are no intangible assets) jumped by £32.7M to £105.4M.

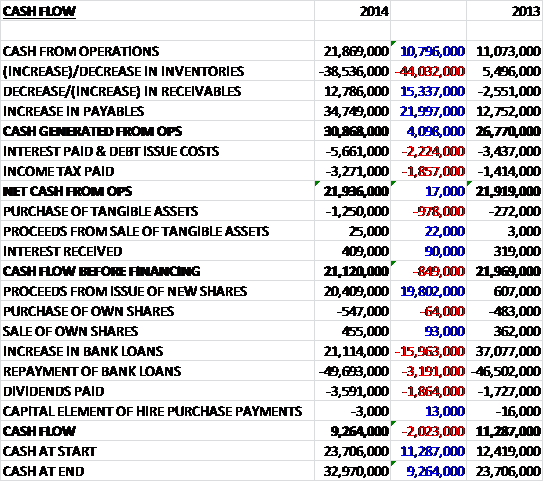

Before movements in working capital, at £21.9M cash profits were some £10.8M higher than last year. A large increase in inventories was offset by favourable movements in receivables and payables so that cash generated from operations was £30.9M, a £4.1M increase on 2013. There was higher interest and tax paid so that net cash from operations was actually flat on last year at £21.9M. Only £1.3M was spent on the purchase of tangible assets and free cash flow was £21.1M, a slight fall. The group then seems to have shuffled debt around so that a £20.4M placing was used to repay some bank loans and pay £3.6M of dividends so that the cash flow was £9.3M and the cash levels at the end of the year were £9.3M. It is pleasing to see debt reduced but a placing of shares was needed to do it.

During the year the group exchanged contracts for 515 open market properties and increased the forward sold position and including contract revenue from affordable housing the value of secured but unrecognised revenue at the end of the year was £341M, despite the lack of any significant development launches in the second half of the year. After the end point of the year, however, the group launched Stratford Central which includes 157 open market apartments, 148 of which have already been sold generating more than £70M and with the development expected to be completed in 2018, these are forward sales four years in advance.

Better than expected sales prices were a factor in the profit increase experienced by the group with the gross margin standing at a record 31.9% with the Avant Garde joint venture giving a gross margin in excess of 40%(although only half of profits were attributable to Telford) and the operating margin increasing from 9.7% to 17.1%. As well as the increased sales prices, the group has benefited from a good control on construction costs but inflation in London construction costs is likely to take effect going forward as activity across the city increases.

As far as customers are concerned, roughly equal splits go to owner-occupiers, UK based investors and overseas investors with a slightly higher proportion going to owner-occupiers than in previous years. The group has a policy of marketing each development to UK based buyers before going overseas. The average price of a Telford home is £400K with underlying price inflation in the areas the group are active being between 10% and 15% and with significant undersupply of homes in London, it is easy to see why the prices increase at such a rate. The group is focused on relatively affordable areas of inner London and most of their customers tend to take fairly small mortgages with no sales being made on the Help to Buy scheme which is good as the scheme is clearly susceptible to political changes. The group also seems to provide customers with the service they are looking for as they have received a 98% customer recommendation rate in an independent survey

In September the group purchased its Horizons development in Tower Hamlets for a consideration equal to a variable percentage of the open market sales proceeds that are achieved from the future development. So far an advance of £4M has been paid to the vendors with the remainder settled after individual completions and likely to come to around £20M. In addition the group has entered into a contract to purchase land that is conditional on obtaining planning permission. If granted, the value of the contract is £27.8M. The total development pipeline is expected to generate revenues of £875M, a 40% increase on the position at the same point of last year and £45M has already been received in the form of deposits. During the year the group achieved planning consent for 47 homes and a new church at Hackney Square in Frampton Park, 101 homes and a new school at Vibe in Dalston , 181 homes in Stratford Central and after a planning appeal, 18 homes at Allcroft Road in Camden

As far as financing is concerned, the group has a £120M loan facility extended to 2016 with three banks. To date, £29.6M of this facility has been used and interest is charged at a fairly hefty LIBOR + 4%. This facility is used to acquire development land and undertake site construction. One of the joint ventures, Bishopsgate Apartments, had a £43.1M development loan facility with HSBC which was paid off this year from the proceeds of the now completed development. In addition the group raised £20M of new equity from a combination of existing and new shareholders which was invested in the pipeline of new developments. Despite having a lot of headroom, it is anticipated that the group will increase the £120M loan facility in the latter half of 2015 to support further growth.

There are a number of risks that affect the group that are out of their control. The economic conditions in the UK, and in particular London have a big effect on the housing market, although it should be pointed out that London has one of the most robust housing markets of any city in the world. Any interest rate changes could also have a profound effect both as potential house buyers being put off by higher rates and the more direct effect of the increased cost in borrowings. A 1% increase in interest rates would increase costs for the group by £452K. To combat this, they have entered into an interest rate swap which effectively fixes interest rates on £50M of borrowing for two years. As well as on the demand side, a potential risk is an increase in costs on the supply side and getting land at the best price is critical in maintaining margins. Due to the long term nature of this business, if the group has stocked up on relatively expensive land when times are good, if there is a down turn they may find it hard to make much margin on the resultant home sales. Another risk is the political landscape, which can have direct and indirect effects on trading.

Going forward, the strong pre sold position, with over 150 homes sold already in this year’s launch at Horizons and Lime Quay and the increase of the development pipeline gives a good visibility over future profits and given a stable market, pre-tax profits are expected to increase next year and more than double by the year end 2018.

At the current share price the P/E is 13.7, falling to a rather cheap looking 11.5 on next year’s estimates. There is a policy where the group pays out one third of earnings in dividends so after an 80% increase in the pay out the shares are currently yielding 2.5% which improves to 2.9% on next year’s forecast, which seems like a fairly decent return. At the end of the year the group was in a net cash position of £4.8M, a vast improvement on the net debt of £34.4M at the end point of last year, although the board expect debt to increase as more work is undertaken and more sites are added to the development pipeline.

Overall then, Telford homes seems to be a company going places. Profits are almost double that of last year, net assets are increased by more than the extra cash received from the share placing and although, slightly below that of last year, free cash flow is at a pretty decent rate. Going forward, there is good earnings visibility and the group is expanding, although it sounds as though there will be some reliance on new debt which might be a concern given any interest rate changes. The shares seem good value on a P/E ratio basis and the dividend yield is fairly decent so I might look for an entry point at this company.