Telford Homes has now released its interim results for the year ending 2015.

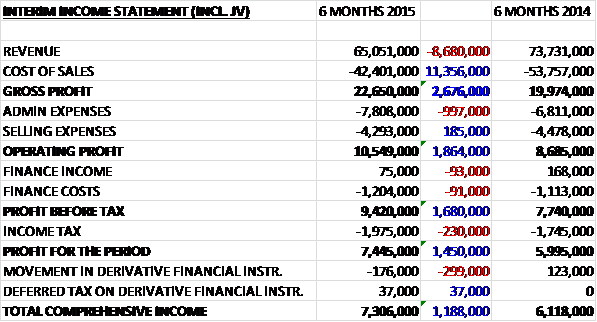

When compared to the first half of last year, revenues fell by some £8.7M in H1 2015 due to the timing of completions. Cost of sales also fell, though, to give a gross profit £2.7M up. Admin expenses increased, as a result of higher staff costs, but selling expenses showed a small decline so that operating profit was £1.9M higher. A small adverse movement in finance income/costs due to non-utilisation fees on the credit facility and a small increase in tax meant that the profit for the period of £7.4M was £1.5M higher than during the same period of last year.

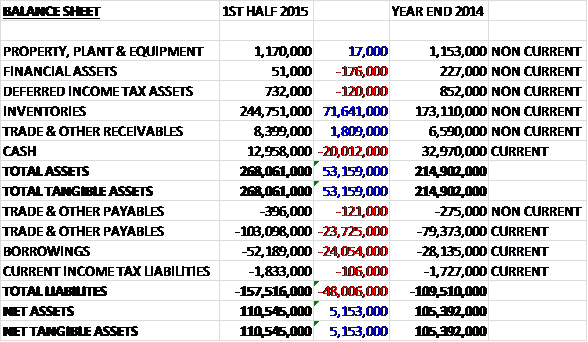

When compared to the end point of last year, total assets increased by £53.2M driven by a £71.6M increase in inventories, somewhat mitigated by a £20M fall in cash levels. Likewise liabilities also increased due to a £24M increase in borrowings and a £23.8M growth in trade and other payables. This meant that net assets were some £5.2M higher at £110.5M.

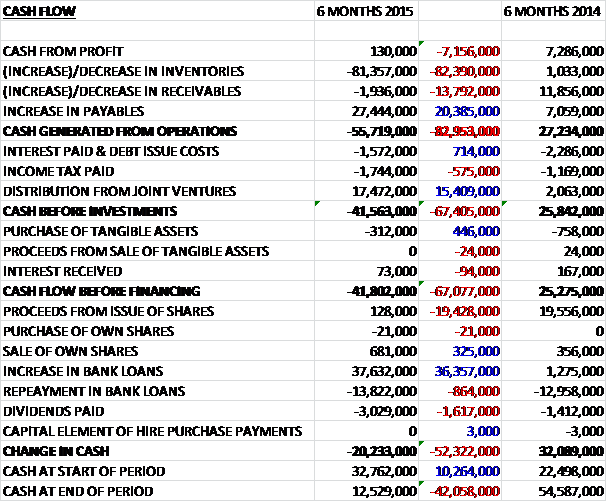

Before movements in working capital, cash profits were some £7.2M lower at just £130K. A huge increase in inventories, however, meant that there was a cash outflow of £55.7M. After the £17.5M contribution from joint ventures, somewhat offset by interest and tax, there was still a net cash outflow of £41.6M from operations. A small purchase of tangible assets meant that free cash flow was a negative £41.8M. In order to balance the books somewhat there was a net £24M increase in loans, partially offset by a £3M dividend payment to give a cash outflow for the period of £20.2M. Considering the cash position at the end of the period was £12.5M, this looks a little precarious, although it should be noted that this situation was flagged up by management in the last update.

During the period the group agreed contracts for the sale of more than 600 open market homes which is more than were sold during the whole year in 2014. The development pipeline has increased to £1.1BN of future revenue and half of this pipeline has been forward sold. The results for 2015 are expected to be weighted towards the second half of the year with a greater number of open market completions due in that period, including in the Parliament House and Lime Quay developments.

In the first half of the year, open market completions were 140 compared to 222 last year. Some of the progress made on the pipeline includes the £16.3M contract to progress the first three phases of redevelopment of Poplar Business Park. The first phase has planning consent for 170 homes with total revenues expected to be in excess of £75M. This followed the purchase of a development site on Rotherhithe New Road in Southwark for £19M which has planning permission for 158 homes and two new schools. Construction work for both of these projects will start later in the year. Another acquisition involved a 50:50 joint venture with Notting Hill housing group which has purchased a significant site in Stratford for £44M. Outline planning consent has already been granted and an application to create 400 new homes will now be pursued. Despite these successes it seems the board is becoming more frustrated with the planning process in general and particularly how long consent can take.

The gross profit margin during the period was an impressive 36.6%, an increase on the 31.9% recorded last year. The increase is predominantly due to the fact that more than half of the completions were at the Avant Garde joint venture which enjoys a profit margin north of 40% as opposed to the 24% target the group uses when appraising new opportunities. Over the past couple of years house prices in London have increased significantly but this has been partially offset by increasing labour and material costs and management expects a more modest sales price inflation over the next few years. Due to these issues, it is expected that gross margins will fall back down to the 24% level going forward.

The market outlook for London remains positive as demand outstrips supply in the areas the group operates in and the recent launch of Stratosphere, a 36 storey tower in Stratford went well with over 270 of the 307 open market apartments being sold already with future revenues from the site exceeding £110M. Other launches include Stratford Central where 151 of 157 open market homes have been sold and Vibe in Dalston where 79 of 81 homes in the first release were sold. Completions commence with Vibe in late 2016 and conclude at Stratosphere in late 2018, showing how far in advance sales are made. The group is still selling homes faster than it can currently build them.

As the majority of homes that should legally complete before the end of the year have already been sold, the board are very confident of hitting expectations and the cumulative profit before tax for the next four years should still be in excess of £120M. Going forward there is £550M of future revenue forward sold and the board are confident of a bright future for the group.

An interim dividend of 5.1p was declared which represents a yield of 2.9% at the current share price and is a 38% increase on last year’s interim pay out. At the half year point, net debt stood at £39.2M compared to a net cash position at the end of last year. This increase in debt was fully expected as the group ramps up its acquisition of land and construction of homes. So far £52.2M of the £120M of debt has been used so there is sufficient headroom and net debt is expected to increase further as more land is acquired and construction continues.

Overall this is another good update from Telford Homes. Profits were up, as were net assets but there was a hefty cash outflow during the period, resulting in higher debt levels as the group expands further. The future growth potential is certainly exciting but not without risk as the company will become more susceptible to any downturns. The housing market in London is very robust, however, and with a decent dividend yield I still consider these shares a good investment and will look for an entry point.

On the 18th December the group announced that Frank Nelson will be appointed as a non-executive director of the company and will replace Robert Clarke who is retiring. Frank has over 25 years of experience in the construction, contracting, infrastructure and energy sectors and was Finance Director of Galliford Try for 12 years up to October 2012. He is also a non-executive director of Thames Valley Housing Association which my prove useful to the group.

On the 23rd January it was announced that Schroders sold 541,860 shares in the company which have a value of about £1.9M. This is a substantial sale but they still own 9.9% of the group’s shares.

Looking at the Chart, Telford underwent a strong bull run prior to 2014 but retracted somewhat before recovering towards the end of the year. Although not bad, there does not seem to be much in the way of movement in price at the moment so I will try and use the chart to show me a decent entry point.

On the 5th March the group announced that it had signed a new £180M loan facility to support its growth plans. The revolving credit facility extends to March 2019 and is being provided by HSBC, RBS, Santander and Allied Irish. This facility replaces the group’s existing £120M loan and has a lower cost of debt. This all sounds good, hopefully the group will be sensible with its expansion plans. I have decided to dip my toes in here.

On the 22nd April the group released a trading update covering the full year. Overall, profit before tax is expected to be above current market expectations and profit margins are going to be higher than last year, assisted by some commercial property sales at higher than anticipated prices and cost inflation being lower than estimated. It is expected that margins will return to normal going forward due to more modest price inflation and some material and labour cost increases. Demand for the group’s properties remained strong and they exchanged contracts for the sale of 661 open market properties during the year, an increase of 28% at an average price of £459K, an increase of £59K. The group is already 93% sold in terms of open market homes expected to be complete in the year ending 2016.

Recent launches included Manhattan Plaza in E14, which is close to Canary Wharf and benefiting from a new Cross Rail station in the future. Earlier in the year the group launched The Junction in E1 where half of the 26 open market homes have been sold and the Town Apartments in Kentish Town where all 15 open market homes sold in a single weekend.

The development pipeline has exceeded £1BN and since on top of this, the group has recently acquired a site in Upton Park where they will submit a planning application for more than 170 homes. In addition, they have recently agreed terms with one of its affordable housing partners on a scheme with planning permission for more than 100 homes. The time taken to achieve planning permission can cause delays to the planned development programmes but in recent months the group has finally received a resolution to grant planning consent for a development on Caledonian Road and expects to complete on the site purchase shortly. This development will consist of 96 open market apartments and 60 affordable homes with construction expected to start within the next few months.

After taking into account the high volume of completions during the second half of the year, the development pipeline remains at over £1BN, over half of which is forward sold. The board is apparently not concerned about any individual property proposals announced by the main political parties given the price point of their homes and there does not seem to be much volatility leading into the election. Given the substantial forward sold position and development pipeline, the board expects significant growth in profits over the next few years. This all sounds very positive and I am happy to remain holding here.