Over the period Tesco has changed the way in which it reports its different segments. They have moved the retailing activities in Ireland, previously disclosed in the Europe segment, into a new UK and Ireland segment. The activities in other countries, previously split between Europe and Asia have been combined into an International segment. The activities in South Korea have been classified as discontinued operations.

Tesco has now released its interim results for the year ending 2016.

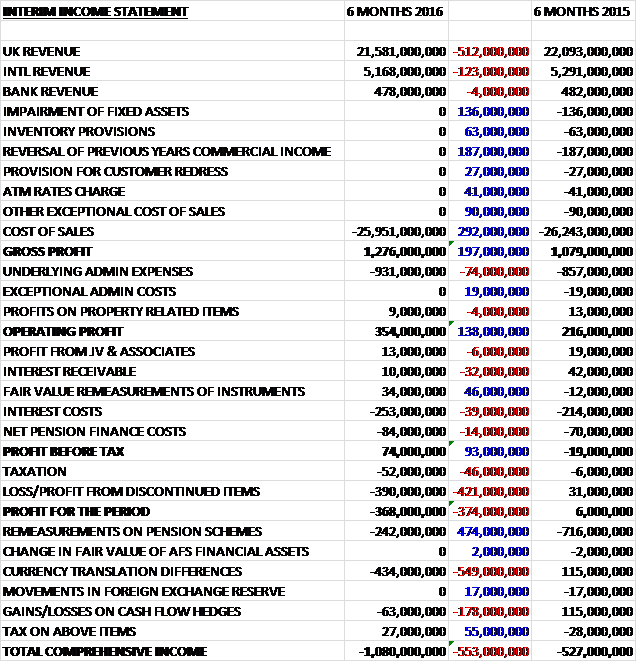

Overall revenues declined when compared to the first half of 2015 due to a £512M fall in UK and Irish revenues, a £123M decrease in international revenue not helped by the strength of Sterling against the Euro and a £4M decline in bank revenue. Underlying cost of sales fell by £292M due to a decline in the cost of inventories, but there were also a number of non-recurring costs last year that were not repeated including a £187M charge for the reversal of previous year’s commercial income and a £136M impairment of fixed assets. This resulted in a gross profit some £197M above that of last time. Admin expenses did increase, though, to give an operating profit just £138M ahead. We then see a net £71M increase in interest costs and a £14M growth in pension finance costs which meant the profit before tax was just £74M, albeit £93M better than last time. An increase in tax and a £390M loss contribution from the South Korean discontinued business, however, meant that the loss for the period came in at £368M, a detrimental movement of £374M year on year due to the £31M profit from discontinued items.

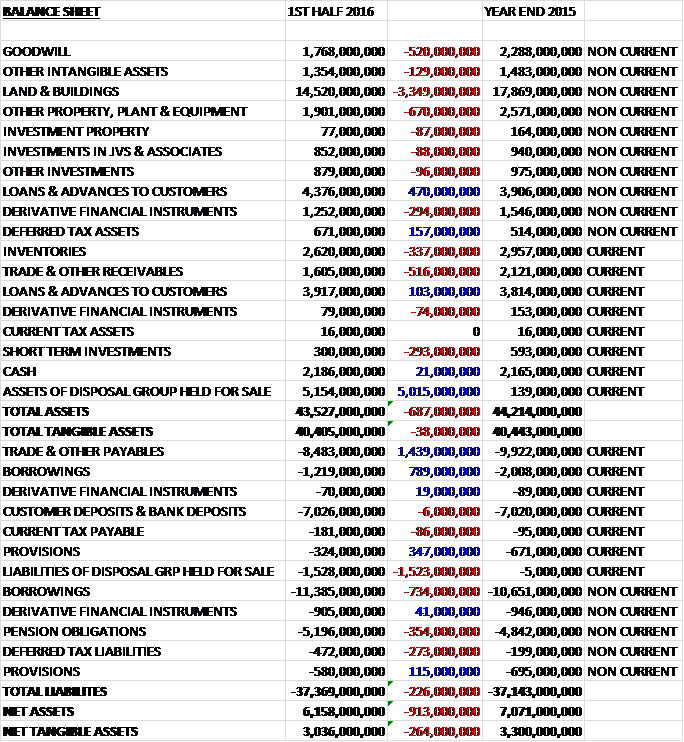

When compared to the end point of last year, total assets fell by £687M driven by a £3.349BN decline in land & buildings, a £670M fall in other property, plant & equipment, a £520M decrease in goodwill, a £516M decline in receivables, a £294M decrease in derivative financial instruments, a £293M fall in short term investments and a £337M decline in inventories. This was partially offset by a £5.015BN increase in the assets held for sale and a £573M growth in loans to customers. Total liabilities increased during the period as a £1.523BN increase in liabilities held for sale, a £354M increase in pension obligations and a £273M growth in deferred tax liabilities were partially offset by a £1.439BN fall in payables and a £462M decline in provisions. The end result is a net tangible asset level of £3.036BN, a decline of £264M over the past six months.

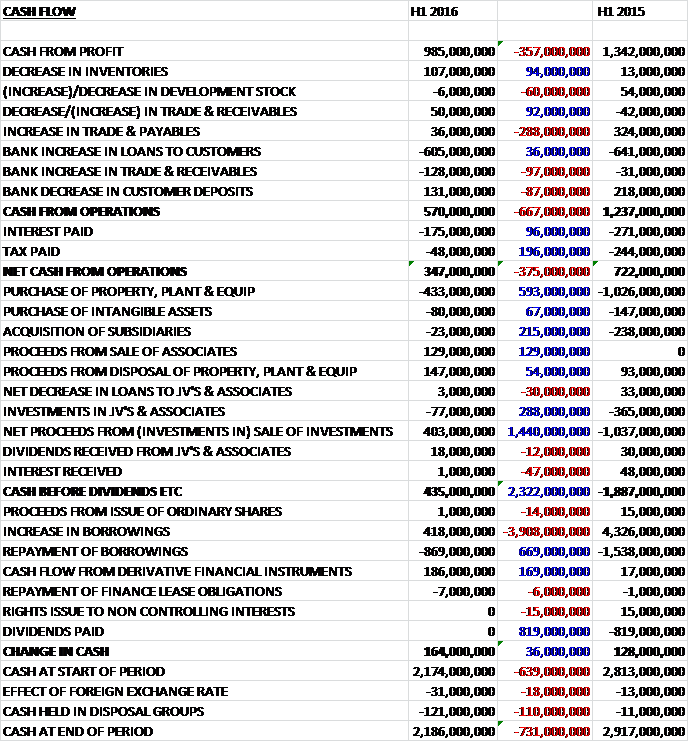

Before movements in working capital, cash profits fell by £357M to £985M. A much lower increase in payables year on year increased this decline and a £605M increase in bank loans to customers meant that cash from operations was £570M, a decline of £667M when compared to the first half of last year. A smaller interest payment and much lower tax paid, however, gave a net cash from operations of £347M, a fall of £375M year on year. We then see £433M spent on fixed assets (£593M less) which mainly related to new stores opened in Thailand, and £80M spent on intangibles which was offset from sales of joint ventures, associates and investments so that before financing there was a £435M cash inflow. This was used to pay back loans with a net £451M being repaid to give a cash flow of £164M for the half year and a cash level of £2.186BN at the period-end.

The operating profit in the UK and Ireland business was £166M, a decline of £377M year on year. First half UK profits also include charges in respect of the restructuring of Dunnhumby’s US relationship with the Kroger Co, in addition to income received following the settlement of proceedings against Mastercard. Like for like sales declined by 1.3% with an improved performance in Q2 (1% fall) than in the first quarter. In the UK, customers are responding well to improvements in the core offer and the group are seeing sustained year on year growth in transactions and volume which is more than offset by deflation driven by the price investment and lower commodity prices. The closure of 53 unprofitable stores in the UK during the period and the reduced levels of store openings led to a contribution from net new space of just 0.5%. In Ireland the group have made a significant investment to improve price competitiveness. This has led to an improving trend in volumes throughout the half and an increase in market share for the first time since 2013.

The group have made permanent reductions to their cost base, fundamentally changed the way they do business with suppliers and have started to generate positive operating leverage through increasing volumes. The progress made so far, combined with the improved productivity as they continue to simplify the range, will enable them to fund further improvements for customers in the second half.

The operating profit in the International business was £102M, a decrease of £35M when compared to the first of last year, driven by the impact of investments in the customer offer and legislative changes in Hungary, including mandated store closures on Sundays and the introduction of a “food supervision fee” from January which the European Commission is currently investigating. Total like for like sales increased in the period for the first time in nearly three years. Like for like sales grew in all European markets as customers responded to investments in the fresh food offer, with improving sales trends particularly evident in Poland and Slovakia. They also delivered like for like sales growth in Thailand in Q2 driven by both increased customer numbers and higher volumes, despite high levels of deflation and a difficult consumer environment.

The restructure of the teams in Czech Rep, Hungary, Poland and Slovakia is now complete, moving from operating as individual country trams to one regional team. The board see significant opportunities for synergies in buying, marketing and operations across the markets.

The operating profit at the bank was £86M, a fall of £13M year on year mainly due to an initial reduction in interchange income following Mastercard’s agreement with the Competition and Markets Authority for a phased introduction of new, lower fee levels. This agreement is ahead of the introduction of European Commission caps which will lead to a further reduction from December. In July the bank became the first in the UK to show foregone interest on customer’s monthly statements which allows them to see if they could have earned more interest by transferring deposits from their current account to an instant access savings account.

In addition, the business introduced a 95% loan to value mortgage and smaller loan sizes during the period which contributed to an increase of 10.2% in customer lending. In a very competitive market, the insurance business was able to broadly maintain the number of in-force policies. The profitability of both home and motor products has benefited from further enhancements to their underwriting approach.

The share of the post-tax profits from joint ventures and associates declined by £6M to £13M as a result of increased losses in the partnership with China Resources company. Commitments for capital expenditure were £294M at the period end principally relating to store development. The group are making progress in their cost saving initiatives and are on track to deliver annual savings of around £400M across the company.

During the period the group reached a decision to close the pension scheme to new entrants and future accrual from November, and to replace it with a new defined contribution scheme. During the period the pension deficit increased by £300M to £4.2M driven by asset returns which have been impacted by volatile equity markets in recent months. A cash contribution of £92M was made to the scheme during the period.

In March the group obtained sole control of the Tesco Aqua Ltd Partnership, previously a joint venture with British Land. The group received British Land’s share of the partnership and cash of £96M in exchange for British Land taking sole ownership if three shopping centres, three retail parks and three standalone stores which were held in joint ventures between the two companies. The consolidation of the Tesco Aqua partnership has increased property, plant and equipment by £465M, being the fair value of 21 standalone stores included in the assets acquired, together with increasing group liabilities by £474M third party debt and £57M derivative liabilities. No goodwill was recognised on the transaction.

The serious fraud office commenced an investigation into accounting practices at the group in October. The SFO could decide to prosecute individuals and the group and there is a possibility of fines and other consequences. Also, class actions have been filed in the US against the group and various directors for alleged violations of US federal securities laws. The lead plaintiff filed a claim on behalf of all investors in May 2015 and the group filed a motion to dismiss the claim in August. In addition, law firms in the UK have announced the intention of forming claimant groups to commence litigation against the group for matters arising out of its overstatement and have secured third party funding for the litigation. No such litigation has yet been formally threatened so the group does not make any assessment of the outcome.

After the period end, the group entered into a conditional agreement to sell the Korean business to a group of investors led by MBK Partners, and including Canada Pension Plan, Public Sector Pension Plan and Temasek Holdings with completion expected in October. The £3.839BN fair value less costs to sell exceeds the carrying value of the Korean net assets so no impairment loss has been recognised. As can be seen there was a substantial loss from the discontinued South Korean business. This was due to a £419M one-off charge which relates to a deferred tax charge of £408M and costs to sell of £11M, the business itself made an operating profit of £29M. Last year the loss from discontinued operations included a £53M tax charge from the disposal of Chinese operations.

Going forward, the market remains challenging. In the second half the group will continue to benefit from initiatives already undertaken to improve the competitive position and reduce the cost base which means that full year expectations remain unchanged.

Tesco does not currently pay dividends, and most analysts expect this to continue for the whole year. At the period end the group had a net debt of £8.588BN compared to £8.481BN at the end of last year with the increase mainly as a result of the £561M debt acquired on the acquisition of Tesco Aqua partnership. The total indebtedness which includes lease commitments and pension deficit was £21.880BN compared to £21.719BN at the start of the year. Not including the pension deficit and adding on the pro-forma effect of the Homeplus disposal, the total indebtedness stands at £13.454BN.

Overall then this has been a difficult period for the group but one of some progress. Profits fell in the period due to the deferred tax on the sale of the Korean business but last year, we also saw a plethora of one-off costs and without these, underlying profit was also down during the period. Net assets also declined as did operating cash flow. There was no free cash as such but some was obtained from the sale of investments which was used to pay down debt. In the UK and Ireland, profits fell but like for like sales declines were slowing and volumes increased. Internationally, profits were also down mainly due to the Sunday closure in Hungary and the dubious sounding “Food Supervision Fee” in the same country. Like for like sales in Europe were up though, and Q2 saw an improved performance in the most important Asian market, Thailand.

Profit at the bank also declined due to a reduction in the interchange income on transactions with more declines to come. Additionally, profits in the associates fell due to increased losses in China, which sounds a little ominous to me. The group is also under pressure from the SFO investigation and various litigation threats. The sale of the Korean business did bring in some much needed cash to reduce further but the disposal of a profitable overseas business is a little disappointing in my view.

In conclusion then, things do seem to be improving in the core market but there are still potential headwinds and the discounters are not going anywhere – the risk/reward on this one doesn’t quite look good enough in my view.

The share price has certainly recovered over the past week, reacting well to the Sainsbury update but it is debatable as to whether the downtrend has been broken.

On the 15th October the group announced that it had agreed the sale of 14 Spenhill development sites across London, the South East and Bath to a fund and clients advised by Meyer Bergman. The transaction, worth £250M, is for sites suitable for mixed use and residential development. This seems like a good deal to offload more land that is not going to be developed and to strengthen the balance sheet.

On the 26th November the group announced it had reached an agreement to settle a class action commenced in New York on behalf of the holders of the ADRs. The class action against the company alleged breaches of certain US federal securities laws in connection with the overstatement of commercial income. The settlement agreement amounts to $12M and there remains one more claim Brought in Ohio representing the remaining ADRs which it looks like will be paid off too.

On the 14th January the group released an update covering Q3 and Christmas trading. In Q3, group like for like sales declined by 0.5% with a 1.5% fall in the UK and a 1.2% decline in Ireland being partially offset by a 3.3% growth in Europe and a 2.4% increase in Asia. The figures for the Christmas period were much better with a total 2.1% growth with the UK up 1.3%, Ireland increasing by 2.9%, Asia up 4% and Europe growing by 4.2%. Within the UK like for like growth of 1.3% over Christmas, volumes were up 3.5% and customer satisfaction increased considerably.

In Q3, total sales were in line with last year at constant rates as the sales reduction from store closures slightly exceeded the contribution from new store openings but at actual rates, sales declined by 2.2% reflecting the impact of Sterling strength. In the UK, the like for like sales decline of 1.5% reflected the impact from not repeating the national coupon campaigns from the prior year.

The strong Christmas performance was helped by a 5% reduction in price for some lines and the growth in sales was evident across all categories including positive like for like sales growth in the Extra format, where customers responded well to the seasonal general merchandise ranges. In clothing, sales grew significantly ahead of the market with strong ladies fashion and knitwear ranges supported by an attractive Christmas gifting offer.

The positive sales performance over Christmas in Ireland followed an improving trend in sales and volume through the course of the year. There has been a strong customer response to the investments made through the year, in particular the move to lower, more stable prices on key lines.

The sustained positive like for like growth in both Europe and Asia is being driven by improvements across the offer, particularly in food. Combining the Central European businesses is already making a difference, giving them further ability to invest for customers and supporting better availability and improved service. In Asia, the performance in Thailand was particularly good with strong growth in customer transactions leading to Tesco’s highest ever market share.

Tesco bank continued to see strong growth in lending and an increase in number of customers for the home insurance products. Despite this there was a reduction in sales of 5.2% over the Christmas period due to the introduction of European Commission caps on interchange income in December which followed an initial reduction driven by Master Card’s agreement with the CMA in April.

The increase in like for like sales on a constant exchange rate is pleasing but in Q3 total sales at actual exchange rate saw a group reduction of 2.9% in sales with a 1.5% fall in the UK, a 9.3% decline in Ireland, an 8.2% fall in the rest of Europe and a 4.5% decline in Asia. There does seem to be some progress here, though, but I think it is far too early to decide that the downtrend has been broken so I remain out and unless things drastically change, this is likely to be my last report on Tesco I think.

Also on the same day it was announced that Alison Platt and Simon Patterson will join the board as non-executive directors. Alison is the CEO of Countrywide, the UK’s largest property services group and has a wealth of experience in the property sector. Simon is MD of Silver Lake Partners, a global technology investment firm and is also a non-executive of N Brown.