TT Electronics is now organised into four divisions which include Transportation Sensing and Control which develops both sensors and control solutions for automotive OEMs and tier one suppliers including powertrain providers for passenger cars and trucks. The division develops a wide range of sensors for multiple applications on a vehicle from gear position and pedal sensors to fluid and emission sensors. The Industrial Sensing and Control division develops position, pressure, temperature, flow and fluid quality sensors which are used for applications in a range of end markets including industrial automation, industrial process control, medical and aerospace sectors.

The Advanced Components division creates specialist, highly engineered electronic components for circuit protection, power management, signal conditioning and connectivity applications in harsh environments. The division serves customers in the industrial, automotive, aerospace, defence and medical markets and focuses on developing solutions that solve challenging problems for their customers. The Integrated Manufacturing Services division provides electronic manufacturing solutions to customers in the aerospace and defence, medical and industrial sectors. The division has broad capabilities ranging from printed circuit board assembly to environmental test and full systems integration and is focused on low volume business.

TT Electronics has now released its final results for the year ended 2015.

Revenues have fallen when compared to last year as an £11.6M growth in Integrating Manufacturing Services revenue, and a £2.2M increase in Industrial Sensing & Control revenue due to positive forex movements was more than offset by a £24.7M decline in Transportation, Sensing & Control revenue and a £3.5M decrease in Advanced Components revenue. Depreciation declined by £600K and other cost of sales were down £26.2M which meant that the gross profit was £12.4M above that of 2014. Underlying amortisation costs declined by £1.5M and a raft of non-underlying costs fell, including a £13.2M reduction in the spend on the operational improvement plan, a £4.1M fall in other restructuring costs , a £2M decrease in management change charges, a £7.7M reduction in impairments which this year related to the North African resistors business reflecting the downturn in activity experienced in H2, and a £1.6M positive swing in deferred consideration relating to the decline in the oil and gas market following the Roxspur acquisition. Other admin costs did increase by £21.8M, however, so that the operating profit was up £20.6M.

We then see a £400K fall in the interest on employee obligations being offset by a £1.2M increase in bank interest costs but after a £1.2M fall in tax costs, the profit for the year came in at £10.4M, a growth of £20.9M year on year.

When compared to the end point of last year, total assets increased by £41.6M driven by a £25.5M growth in goodwill, an £18.3M increase in other intangible assets, a £1.5M increase in receivables and a £1.5M growth in cash which was partially offset by a £4.4M reduction in property, plant and equipment. Total liabilities also increased during the year as a £43.3M growth in borrowings, an £8.7M increase in the pension liability and a £2.1M growth in payables was partially offset by a £6.3M decline in provisions, a £2.6M fall in the income tax payable and a £1.9M decrease in accruals and deferred income. The end result is a net tangible asset level of £55.9M, a decline of £44.2M year on year.

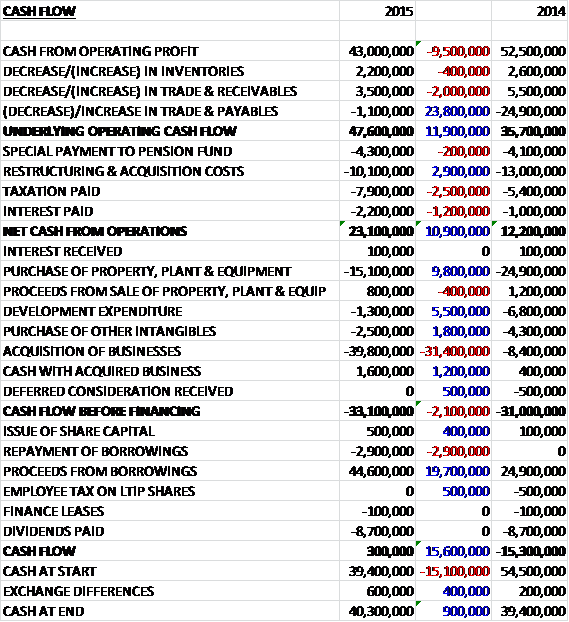

Before movements in working capital, cash profits fell by £9.5M but there was a modest cash inflow through working capital and a much lower fall in payables than occurred last year. Restructuring costs did fall by £2.9M but tax payments increased by £2.5M and interest costs were up £1.2M to give a net cash from operations of £23.1M, a growth of £10.9M year on year. The group then spent £15.1M on property, plant & equipment, £1.3M on development expenditure and £2.5M on other intangible assets before a net £38.2M was spent on the acquisition which meant that before financing there was a cash outflow of £33.1M. The group then paid out £8.7M in dividends that it couldn’t really afford so took out £41.7M of new borrowings to give a cash flow of £300K for the year and a cash level of £40.3M at the year-end.

Overall results were in line with board expectations in what was a year of transition. The reduction in revenue was largely as a result of the non-recurrence of two large one-off orders. These orders contributed £5M of profit last year and overall profits were also affected by lower R&D capitalisation with a £2.5M increase in the R&D expense, although profits did benefit from a £1.4M positive forex benefit. The order book remains sound, albeit recent weakness in the shorter cycle industrial markets has resulted in it being slightly below that of the same time last year.

The underlying operating loss in the Transportation Sensing and Control division was £1.4M, a detrimental movement of £2.8M year on year on revenues that declined 3% on an organic basis as a result of contractual price reductions of about 2% and modest volume reductions along with an adverse forex impact of £18.6M. Despite the loss, the operating performance is showing signs of improvement, moving to break even in the second half before exchange movements increased the loss by £400K, with the full impact in the second half.

There was a series of contract wins in target growth markets and with new customers. In the first half the business displaced an existing tier one manufacturer for the supply of an advanced haptic pedal solution for a global premium automotive OEM. They delivered wins in China with three new contracts for accelerator pedals, an oil temperature sensor for a major Chinese transmission manufacturer, and a crankshaft sensor leveraging an existing product design. They also won a global project for a new chassis height sensor based again on an existing TT design, with initial launch in Europe and China.

The division also secured a development order from a large tier one customer for a new linear sensor for suspension systems and extended their capabilities in high temperature sensors via the purchase of capital equipment from a supplier. They launched their AdBlue optical fluid sensor which is used to reduce NOx emissions for diesel exhaust systems, a key area of OEM focus to address legislative change and their first-mover advantage was reflected in securing their first customers in Korea, India and China.

The underlying operating profit in the Industrial Sensing and Control business was £11.4M, a decline of 11% on last year, and an 18% fall at constant exchange rates. This was on revenues that declined by 10%, mainly due to the non-recurrence of a material one-off order for steering position sensors last year. Excluding this impact, like for like revenues increased by 4%. The absence of the last order affected profits by £4M and was partially offset through new orders and some initial modest benefits from the transfer of activity from Fullerton to Mexico, which was completed in the second half. Roxspur contributed an additional £300K during the year.

The division secured a number of key programme wins in the year. In their core industrial markets they shipped the first production order for their latest phase diode array, a critical component used in robotic position sensors. Working with a major customer, they designed a custom optical sensor with increased ambient light immunity to meet a specific application need, resulting in the award of business on their next generation platform which is expected to be volume production from 2016 for a minimum of four years.

The business also secured a number of new wins with its position and torque sensors used in electronic power steering systems. By focusing on the recreational and off-road vehicle markets where the deployment of these systems is increasing, they secured a number of new multi-year programmes with customers in the US and Asia. The integration of the Roxspur business is now complete but it has been impacted by the slowdown in the oil and gas sector which has resulted in £2.5M of contingent consideration now not becoming payable.

The underlying operating profit in the Advanced Components division was £6M, a decline of 37% year on year on revenues that declined by 7% reflecting a weaker second half performance from the resistors market and the prior year’s £2M of non-recurring revenues associated with the closure of the Smithfield facility. The reduction in profit was put down to this high-margin non-recurring revenue, increased depreciation from last year’s investments and the reduction in demand for resistors products.

The business released a number of new products during the year and successful launches included a high power current sense resistor for the industrial, medical and automotive markets in motor drive, battery monitoring and process control applications; passive components which have been ordered by all three manufacturers of smart meters; and custom inductors for a major tier one automotive supplier to the truck market.

At the end of 2014, the business extended its long term agreement with Controls and Data Services. In support of this agreement, a new clean room facility to supply multi-chip modules for fuel management systems on aircraft engines was constructed which opened in early 2016. This has also positioned the division to accept the transfer of production from Fullerton as part of the additional footprint reduction.

The underlying operating profit in the IMS division was £5.7M, an increase of 4% year on year, although this included a favourable foreign exchange benefit and on a constant currency basis, the profit fell by 11% on revenues that were up 4% driven by strong demand in the US and China. The profit performance was as a result of a substantial adverse mix impact in the first half of the year which was largely reversed in the second half and a higher allocation of central costs. The growth in revenues in China was supported by contract wins supplying into metro train systems and narrow body aircraft, together with the benefit of a global contract renewal with one of their largest customers, which also supported demand in the US along with a production extension for a major defence customer.

In the first half, the business was chosen by L3 as a partner to support the design and prototyping for a new product to help aircraft operators take advantage of the Next Generation Air Transportation System traffic management standards. The division also passed a number of major customer audits and renewed its NADCAP certifications. In addition they received the Carestream supplier of the year award in China and Cubic Defence’s supplier excellence award in the US.

For the Germany to Romania transfer, the board initially intended to move 16 lines over the life of the project, with ten of those being transferred during 2015. In November, under pressure from the unions, they decided not to move four of the remaining lines as the expected benefits no longer justified the required level of spend. All twelve lines have now been moved and are customer qualified. The final step in the programme is to consolidate the footprint in Germany.

The transfer of production from Fullerton, USA to Mexico was completed in H2 2015 and overall the Operational Improvement Plan is expected to be completed at a cash cost of about £23M, £7M less than the original estimate, and the full run-rate benefits of £5M per annum are now anticipated in 2017, a year earlier than originally expected. What is omitted from this narrative is the fact that this benefit is lower than originally thought. The shorter-cycle industrial market facing businesses experienced market weakness, and the intention is now to make footprint reductions. These plans ae well advance and include relocating the last remaining production out of the Fullerton site to be transferred to the facility in the UK.

On the 18th December the group announced the acquisition of Aero Stanrew for a total consideration of £43.8M consisting £39.8M in cash and the issue of 2,575,669 shares worth £4M to key members of the management team. The acquisition generated goodwill of £22.4M and £18.8M of intangibles have been recognised. The acquisition strengthens the group’s position in growth areas in the aerospace and defence market and is expected to be earnings enhancing immediately with the business delivering EBITDA of £3.6M in 2015.

As a result of the impact of a slowdown in the oil and gas sector, a £2.5M contingent consideration payment relating to the Roxspur acquisition will not now become payable and £800K of contingent consideration accrued to date was released through the income statement.

The triennial valuation of the UK pension scheme in 2013 showed a deficit of £19.1M. It was agreed with the trustees that the group would make contributions of £4.5M in 2016 after £4.3M was paid in 2015, £3.2M in respect of 2015 and £1.1M in respect of the prior year. A further £1.1M was paid early in 2016 in respect of 2015. In addition, the company set aside £3M to be utilised in agreement with the trustees for reducing the long term liabilities of the scheme. The next valuation is due to be undertaken around now.

Despite the tougher macro-economic environment, the combination of self-help actions and the contribution from Aero Stanrew mean the group is on track to make progress in 2016 and the board are confident in their ability to return the business to sustainable profit growth in the medium term.

At the year-end, net debt stood at £56.1M compared to £14.3M at the end of last year and there was £20.3M of long-term facilities available along with £17.3M of short-term facilities undrawn. At the current share price the shares are trading on a PE ratio of 25.5 which falls to 17.2 on next year’s consensus forecast – that looks rather expensive to me. After the final dividend was kept the same this year, the shares are yielding 3.3% which increases modestly to 3.4% on next year’s forecast.

Overall then this has been a mixed year for the group. Profits are up but when we take off last year’s impairments and restructuring, profits fell in 2015. Net assets were also down and although the operating cash flow did improve, this was due to a lower fall in payables and cash profits declined. Some free cash was generate but this doesn’t cover the dividend even before the acquisition is taken into account. The poor performance is put down to less large one-off orders, and less R&D capitalisation which increased expenses.

The transportation sensing and control division was loss making and the performance deteriorated this year due to price reductions and unfavourable forex movements. The industrial sensing and control business saw profits fall due to the one-off steering position sensor order last year; the advanced sensing and control division also saw profits decline as a large order relating to the closure of the Smithfield facility was not repeated and the resistors market saw a difficult H2; and although the IMS division did modestly increase profit, this was entirely due to forex movements and constant currency profits declined due to an adverse product mix.

The acquisition seems like strange timing to me, I would have thought the group would have completed its restructuring first but hopefully that will add to the bottom line despite the extra debt taken on to pay for it. Going forward, markets seem to be tough and the order book has fallen when compared to the same point of last year. With a forward PE of 17.2 and dividend yield of 3.4%, these shares look too expensive to me but then again, I have thought this for some time and they keep going up!

On the 11th May the group released a trading update covering the first four months of the year. Overall trading was in line with board expectations with revenue 4% higher on a constant currency basis and flat on an organic basis. The order book is in line with last year before the additional contribution from Aero Stranrew and trading results in the year to date have been favourably impacted by forex movements.

The integration of Aero Stanrew has progressed well with the majority of the basic integration complete and focus is now shifting to opportunities to enhance value through collaboration with other group businesses which is showing encouraging signs.

Overall, not a bad update but pretty unexciting really and I don’t completely understand why these shares are so expensive. This is perhaps not a view shared by the directors as Chairman Neil Carson has purchased 50,000 shares at a value of £67K to give him a holding of 150,000 in total.

On the 28th June the group announced that director Jack Boyer acquired 40,500 shares at a value of just under £50K. This represents his first share purchase.

On the 11th July the group announced that Alison Wood joined as a non-executive director. She is senior independent director of E2V and a non-executive director at Costain, Cobham and the BSI. She was formerly global director corporate development and strategy for National Grid.