Wentworth Resources has now released their interim results for the year ending 2017.

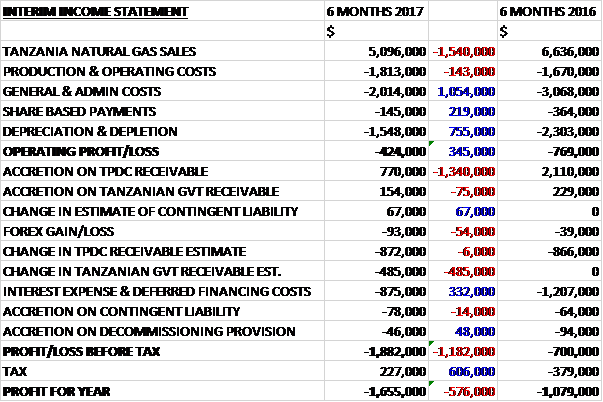

Revenues decreased by $1.5M when compared to the first half of last year. Production and operating costs increased by $143K but general and admin costs were down $1.1M reflecting both cost savings and the fact that some costs in Mozambique are now being capitalised, share based payments fell by $219K and deprecation declined by $755K to give an operating loss $345K better than last time. The accretion on the TPDC receivable fell by $1.3M and there was a $485K detrimental change in the Tanzanian Government receivable but interest expenses declined by $332K and there was a $606K swing to a deferred tax credit so the loss the period was $1.7M, an increase of $576K year on year.

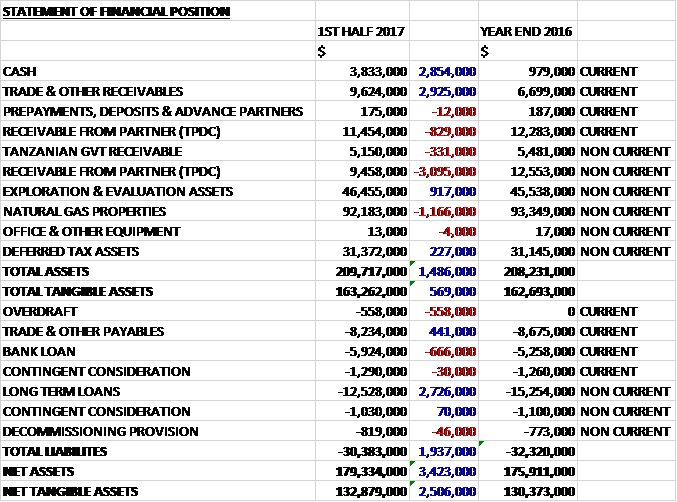

When compared to the end point of last year, total assets increased by $1.5M driven by a $2.9M growth in cash, a $2.9M increase in receivables and a $917K growth in exploration and evaluation assets, partially offset by a $3.9M decline in the receivable from TPDC and a $1.2M fall in the value of natural gas properties. Total liabilities declined during the period was a $558K growth in the overdraft was more than offset by a $2.1M fall in other loans. The end result was a net tangible asset level of $132.9M, a growth of $2.5M over the past six months.

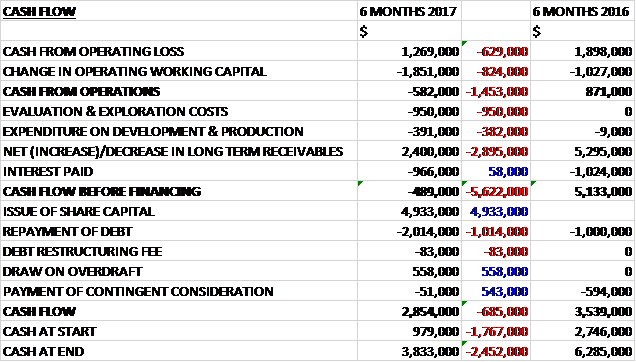

Before movements in working capital, cash profits declined by $629K to $1.3M. There was a large cash outflow from working capital which meant that there was a $582K cash outflow from operations, a detrimental movement of $1.5M year on year. The group spent $950K on exploration, $966K on interest and $391K on development and production but they did receive $2.4M of the long-term receivable to give a cash outflow of $489K before financing. The group then received $4.9M from the issue of new shares along with $558K from the overdraft so they could pay back $2M of debt and leave a cash flow of $2.9M for the half year and a cash level of $3.8M at the period-end.

The Mnazi Bay field achieved average gross daily gas production of 30.7MMScf per day in Q2 and 36.9MMScf in H1 as a whole. Q2 production was impacted by the heavier than usual rainy season during which hydro power is used as a substitute for gas-fired power generation, but production rebounded to an average of 61MMScf per day in July and the group continue to maintain an average production guidance for the year of 40-50 MMScf per day.

Overall sales to TPDC, net to the group declined by 27% in H1 and 41% in Q2 to 1,494,549MMBtu and 619,688MMBtu respectively reflecting the heavier rainy season and the earlier closure of the Symbion power plant. Sales to TANESO increased by 7% in the period to 101,930 with sales prices to both customers broadly stable. This meant that production in the half fell by 25% to 1,560,585Mscf, net to the group and operating costs per Mscf increased by 45% to $1.16 as the operator billed higher overheads in Q2.

During Q2 the group’s gas was used to fuel two power stations – Kinyerezi-1 and Ubungo-II. Additional gas-fired power generation is expected to materialise over the next year and a half with the completion of the Kinyerezi-1 extension and Kinyerezi-2. During the quarter they started delivery of gas to their first industrial customer, a newly constructed ceramic tile factory. Gas demand to power the factory is expected to reach up to 8MMscf per day by the end of the year with deliveries currently at 5MMscf per day.

In addition, TPDC has finished a commercial arrangement to supply gas to a Dangote cement plant for power generation and firing its clinker kilns. Commissioning of the 35MW power plant, which is expected to require around 7MMScf per day of gas, and associated power supply to the plan is expected during the second half of the year. In addition, completion of the pipeline and distribution system delivering gas to the kilns, expected to require an additional 8MMScf per day of gas, is expected by the end of the year.

During Q2, minor works continued on the expansion of the processing facilities at Msimbati. Primary processing of the gas is required to remove free liquids before it enters the submarine pipeline that connects the Madimba gas processing facility. The expansion of the processing facilities together with the tying in all five wells completes all the necessary field work to enable delivery of gas volumes in excess of 100MMscf per day to the TPDC-owned pipeline to Dar es Salaam. Commissioning of these facilities is expected in September and there will be no need for any additional capex until the average daily demand exceeds 100MMscf per day, double what it is now.

They are effectively managing working capital through a period of slower payments from their government agency customers TPDC and TANESCO. At the period-end they were owed eleven months of gas sales by TANESCO with $1.9M outstanding, although after the period-end they paid three months of invoices totalling $510K.

TPDC owes $7.6M, of which four months is past due. After the period-end they paid one month of invoice for $900K relating to the outstanding May gas sales invoice. At the prior year-end only two months’ worth of invoices were outstanding. TPDC’s ability to settle gas sales invoices in a timely manner is directly impacted by the timeliness of them receiving payment for the gas they sell to TANESCO power generation plants. Recently, TANESCO have been challenged to pay them in a timely manner and the group continues to engage with both TPDC and TANESCO on finding ways to improve the timeliness of settling obligations. The face value of money owed is $23.7M and the group expects to fully recover this by Q4 2018 (by which time I am sure more receivables will have built up)

They continue to advance the process of securing a farm-in partner for the drilling of an appraisal well in Mozambique and have received positive initial interest. The government has expressed their support for the drilling of an appraisal well in 2018 in advance of the need to acquire new seismic data over the discovery area. They are currently determining a well location and expect to secure a farm-in partner before the start of drilling operations.

The reprocessing of 1,000km of existing seismic data was completed in Q2. This data is currently being integrated into the seismic interpretation and geologic evaluation of the block and mapping and re-interpretation of the data is ongoing. A new seismic acquisition programme was being considered for H2 and a tender process was completed in the period although the board think they have enough information to support drilling an appraisal well without the need to acquire new seismic. The preferred bidders have been informed of the postponement.

In May the group completed a private placement and issued nearly 17M new shares for a cash consideration of 25p per share for gross proceeds of $5.5M

In Q2 the group executed amendments to the credit facility agreement which include the restructuring of the principal loan payments and the addition of some new provisions: the addition of a debt service coverage ratio and long live coverage ratio as financial covenants, a requirement to maintain a minimum cash balance, a cash flow waterfall procedure to ensure certain cash proceeds from gas sales are used in settling obligations as a priority and a prepayment fee in the event the group decides to accelerate principal payments. The amount outstanding at the period-end was $15.7M with the June payment of $1M paid in July and a July payment of $1.3M due. They are in ongoing discussions to settle the amount due in July in August to coincide with expected receipts of outstanding gas receivables. This seems quite precarious.

There is also another outstanding $6M credit facility that has a $1M payment due in December. In addition they have secured a $2.5M overdraft facility, of which $560K has so far been drawn. The group expect to draw on the full amount of the facility in H2 for short term working capital purposes. The group is also itself now falling behind on payments to the operator of Mnazi Bay with $2.9M outstanding and expected to be settled through cash receipts and receipts from existing gas sales receivables and funds available through the overdraft facility.

As the group made a loss last year and is forecasted to make a loss this year too, there is little point in analysing PE ratios. Based on next year’s consensus forecast, however, the group is trading on a future PE ratio of 23.6.

Overall then it has been a rather difficult period for the group. Losses worsened due to the lower accretion on the TPDC receivable. The operating loss did improve, but this was due to them capitalising some of the costs in Mozambique. The net assets did improve but the operating cash outflow worsened which necessitated a share placing. Production was down in the period due to the heavier rainfall and the closure of the Symbion power plant and the group is not really being paid for what it does manage to sell.

The late payments are really taking a toll here and the group is now having to restructure loans, delay payments to suppliers and set up an overdraft. This risks being terminal if they can’t turn it round and sadly I don’t the two new industrial customers will be enough to stem the tide. This is uninvestable at the moment in my view.

On the 17th August the group announced that it received further payments from TPDC and TANESCO totalling $1.9M for the June 2017 and October 2016 gas invoices respectively. They also confirm that all principal and interest payments currently due on their credit facilities are now fully settled with the next principal payment of $1M due in December. That is a relief!

On the 18th September the group confirmed that further payments had been received from TPDC and TANESCO totalling $2M for one month’s gas sales and two month’s gas sales respectively.

On the 20th October the group announced that it had received $1.1M from TPDC and $400K from TANESCO. Q3 gross production volumes averaged 60MMScf per day, bringing the year to date average up to 44MScf per day. Production volumes have continued at similar levels in Q4 with October month to date averaging over 64MMscf per day. They continue to maintain a full year guidance of between 40 and 50MMScf per day.