Utilitywise has now released its final results for the year ending 2015.

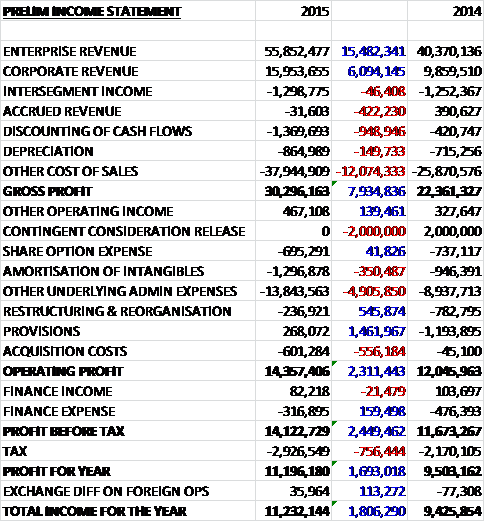

Revenues increased when compared to last year with a £15.5M growth in enterprise revenue and a £6.1M increase in corporate revenue. Cost of sales also increased to give a gross profit some £7.9M above that of 2014. We also see an increase in admin costs, the lack of a £2M contingent consideration release that occurred last year where earn out criteria were not met, and a £1.5M positive swing in provisions, with a provision release occurring this time. Acquisition costs were also slightly higher but operating profit still came in £2.3M ahead. After a slightly smaller finance expense and a much higher tax level, the profit for the year came in at £11.2M, an increase of £1.7M year on year.

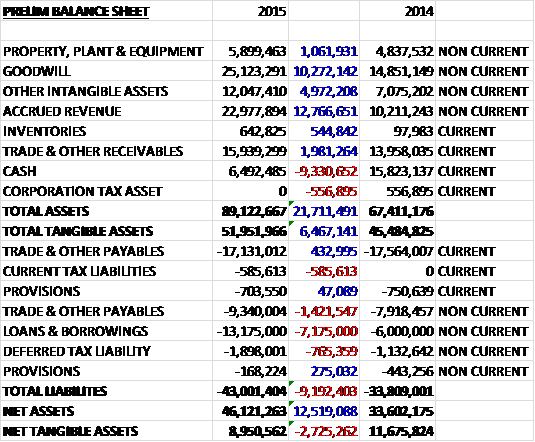

When compared to the end point of last year, total assets increased by £21.7M driven by a £12.8M growth in accrued revenue, a £10.3M increase in goodwill, a £5M growth in other intangible assets and a £2M increase in receivables, partially offset by a £9.3M fall in cash. Total liabilities also increased due to a £7.2M growth in borrowings and a £1.4M increase in payables. The end result is a net tangible asset level of £9M, a decline of £2.7M year on year.

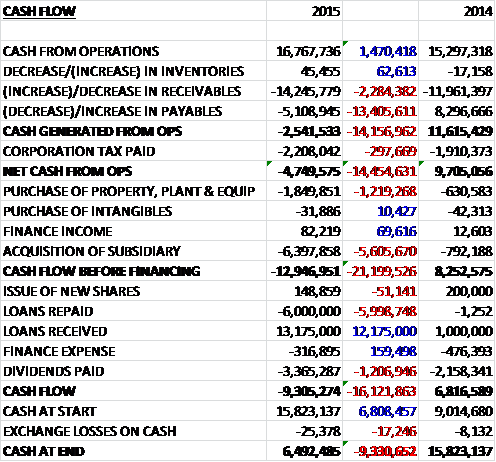

Before movements in working capital, cash profits increased by £1.5M to £16.8M. A huge increase in receivables due to the increased proportion of renewal business compared to last year, plus a fall in payables, however, meant that after tax was a little bit higher, there was a £4.7M cash outflow from operations, a deterioration of £14.5M year on year. The group then spent £1.8M on fixed tangible assets and £6.4M on acquisitions to give a cash outflow of £12.9M before financing. There was then £3.4M paid out in dividends and a net £7.2M in new loans to give a cash outflow of £9.3M for the year and a cash level of £6.5M at the year-end.

There was a note with the results this year that noted the financial statements have been adjusted to reflect the correction of an error made in the financial statements for 2013 and 2014. This arose followings management’s review of the revenue provision (when the revenues are generated, the amount is estimated for the length of the contract and the revenue provision is the predicted variance for customers that do not take as much energy as expected). The conclusion of the report was that the rate used to calculate the estimated variability in value was too low (it is currently 15%) and also the provision was held for two years and then released which did not reflect the lengthening of contract terms the group was experiencing. Last year this means that revenues were increased by £305K in the re-stated finances but interestingly the variance will be assumed to be 15% for 2016.

The profit in the enterprise division was £9.7M, an increase of £4.9M year on year. The profit in the corporate division was £1.2M, a decline of £144K when compared to last year. The group now have 27,000 customers in the UK and 4,000 in Europe. In the enterprise division they have increased their ability to engage with potential customers and have developed their Trusted Advisor framework to ensure consistency and complete delivery of all applicable products and services as part of the Utility Management Plan. These will also enable them to establish a relationship with potential customers outside the normal procurement contract cycle.

During the period they have completed the move to the new HQ which has allowed them to recruit more sales people and support staff. Having increased the salesforce from 363 to 610, they have slowed and refocused their recruitment in recent months to ensure they have quality staff capable of delivering their strategy effectively and to increase customer conversion rates. This means that overall headcount growth in the coming year will be slightly slower than previously expected. There have also been a number of additions to the management team. Steve Atwell was appointed as Managing Director of the Enterprise Division and Brin Sheridan has just been announced as the new COO. Brin has extensive experience in the field of energy management within the built environment space having previously been employed as MD at the Energy Solutions Group. He will oversee the implementation of the group’s energy saving propositions.

At the period end the secured pipeline was slightly below last year but had improved from the position at the half year point when the move to the new HQ had just been completed. By the end of September, the pipeline had grown further to £28.3M. The group have developed an online site intended to assist customers comparing tariffs. It is specifically for certain smaller meter sizes, enabling them to switch supplier with minimal human intervention, therefore making the service viable for the smaller customers.

In April the group acquired T-mac Technologies for £16.2M. The consideration consisted of £6.3M in cash, £3.8M-worth of shares issued and £5.7M of contingent consideration. The total value of the contingent consideration is based on a multiple of expected EBITDA capped at £12M, split between cash and shares. The acquisition generated goodwill of £10.3M and in the three months since the acquisition the business contributed a pre-tax profit of £252K. It is expected that T-mac will provide the group with additional capabilities in the energy monitoring and controls space to help customers of energy not just monitor but to control and optimise their energy usage. The T-mac customer base is more akin to the larger multisite corporate customer but they intend to develop products and services which will appeal and provide this capability to the wider SME customer base. The integration has gone well to date and some additional opportunities have been seen as a result of the joint offering.

Exceptional items in the year related to the costs incurred in the acquisition of T-mac Technologies, costs of £39K in relation to unforeseen late invoices connected to the prior year acquisition of Icon Communications and other aborted acquisition costs. Also included are restructuring and reorganisation costs such as settlement payments of £83K and costs of £52K incurred in the set-up of the head office. During the year there was also a credit of £268K offsetting these costs which arose from the release of restructure and dilapidation provisions not utilised.

Obviously there continue to be specific risks to the company – many of which are the same as last year including any potential regulation of the industry. Going forward the investment in the UK procurement and services business model will continue and the number of sales people is now planned to increase to over 800 by the end of 2016. The group also continues to evaluate acquisitions which will add to the overall proposition and in addition a clear market opportunity exists to continue and evolve the business model across Europe and they are currently procuring energy on behalf of customers in France, Germany, Holland and Belgium.

At the current share price the shares trade on a PE ratio of 13.8 which falls to 10.4 on next year’s consensus forecast. After a 25% increase in the total dividend for the year, the shares yield 2.5% increasing to 3.5% on next year’s forecast. Net debt at the year-end was £6.7M compared to a net cash position of £9.8M at the end of last year.

Also today, in a second announcement the group announced the immediate change to its existing payment terms with a key energy supplier. They have agreed to amend terms such that any extension secured on a contract that has not expired receives the same payment terms as a new customer would, in this case 80% on the extension signing and 20% subject to the normal reconciliation process at the end of the contract. They have also agreed that this change of terms will apply to historic accrued revenue balances and hence they have received £3.6M in cash from the supplier.

As a result of the strengthening supplier relationships and the prevailing energy price environment the length of the contracts being secured for customers has increased. The group have prioritised securing existing customers on longer contracts with their incumbent energy suppliers, either as renewals or extensions to the initial contract. Historically the supplier payment term for this contract revenue was delayed until the extended period had commenced and was booked to accrued revenue on the balance sheet.

Discussions are ongoing with all of the key energy suppliers to amend payment terms to reflect this changing way that the company is doing business, with the aim of agreeing revised terms resulting in the receipt of payment for renewals and contract extensions in a similar way to the revised terms detailed above. This is a very positive step in my view. It does some way to improving cash flow and addressing the very genuine concerns that potential investors like myself have about the cash flow here and the very aggressive revenue recognition policy. More really needs to be done in my view but this is a very positive first step.

Overall then this seems to have been a bit of a mixed year for the group. Profits increased year on year but net tangible assets were down and operating cash flow deteriorated considerably into a cash outflow despite an increase in cash profits as the large number of contract renewals meant there was a huge increase in accrued receivables. The previous year adjustment doesn’t really change much but it does show that revenue recognition is confusing even the company itself. There was a bit increase in customers although these seem to be mainly attributable to the enterprise division where profits increased considerably with profits in the corporate division falling away despite the recent acquisitions.

The levels of sales staff has also increased considerably but it seems that this rate of increase has been a bit too much with a focus more on quantity rather than quantity as new staff don’t seem to have been as productive as expected. The acquisition, although expensive, looks like a decent, profitable, one and the European expansion looks like an interesting prospect. With a forward PE of 10.4 and a dividend yield of 3.5% the shares look cheap but despite the changes in terms with one of the suppliers there is still a nagging doubt over the revenue recognition policy and the outflow of cash during the year. I am tempted at these levels but these doubts are holding me back for now.

On the 15th December the group released an AGM statement. They have made a solid start to the year with trading in line with expectations. The pace of recruitment is picking up and they anticipate their position continuing to improve as the year progresses. The secured future pipeline as of the end of November was £27.7M. The board expect the oil price reduction to feed through to improved tariff opportunities for end consumers, providing further opportunities to serve their customers. They are also making progress in further developing their multi-channel routes to market and overall they view the future with confidence.

Additionally the group have announced the immediate change to their existing payment terms with a second key energy supplier. They have agreed to amend their terms such that any future extension secured on a contract that has not expired receives the same payment terms as a new customer would, in this case either 75% or 80% of the expected revenue from the contract falling due on the extension signing and the remainder at maturity. Discussions are ongoing with more of the key energy suppliers to amend payment terms to reflect the changing way that the group are doing business.

So, we have a positive update, but more important in my view is the fact that another supplier has agreed to a change in terms. I am tempted to take a position here but I think I would prefer to wait until I can see an updated cash flow statement that shows what effect these contract changes are having on the all-important cash position.

On the 17th February the group released a trading update for the half year period. The group has performed in line with management expectations with continued revenue growth in both UK divisions as well as the European operation. In the Enterprise division, gross order book additions totalled £40M in the period and the contract go live rate improved meaning the group revenue pipeline was £24.7M at the period-end, some £1.5M below that of the at the end of last year although it was £1.2M up on the same point of last year.

Energy consultant headcount at the period-end was 625 compared to 610 at the year-end with headcount growth being slightly slower than expected, although it is expected to increase in H2. Consumer numbers stand at 29,288 compared to 25,976 six months ago. The all-important figure though is net debt which stands at £10.4M compared to £6.7M at the year-end. This is in line with management expectations but seems disappointing to me in a period that included the £3.6M received following the change in payment terms with an energy supplier.

The rate of customer acquisition has increased compared to extensions and renewals in line with management expectations and the board expect to report both revenue and profits full the full year in line with management expectations. Overall, the cash position looks poor to me so I am staying clear for now.

On the 11th April the group announced that it had been named a partner by Dell which means they are now one of Dell’s OEM partners as part of a joint strategy to introduce internet of things building automation to customers. It is unclear to me what this actually means!