Victoria Oil and Gas has now released its final results for the year ended 2015.

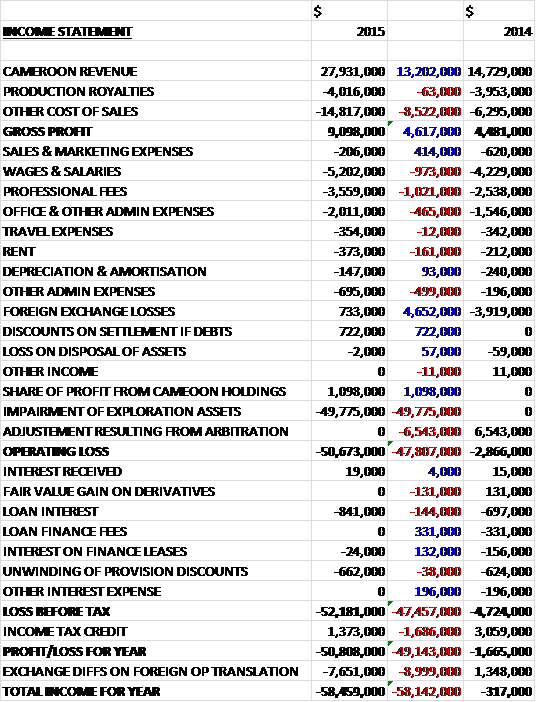

Revenues increased by $13.2M when compared to last year whereas production royalties remained flat and other cost of sales grew to give a gross profit some $4.6M above that of 2014. Sales and marketing expenses declined during the year but depreciation and amortisation increased by $4.7M. Admin expenses fell somewhat and there was a $5.4M positive swing in “other” gains and losses. There was also a $1.1M share of profit from associates before the $49.8M impairment of the assets in Russia meant that there was an operating loss of $50.7M. Finance costs then fell somewhat but there was a much lower tax credit so that the loss for the year came out at $50.8M. If we take off the impairment, the actual loss comes in at just over $1M an improvement of $665K year on year.

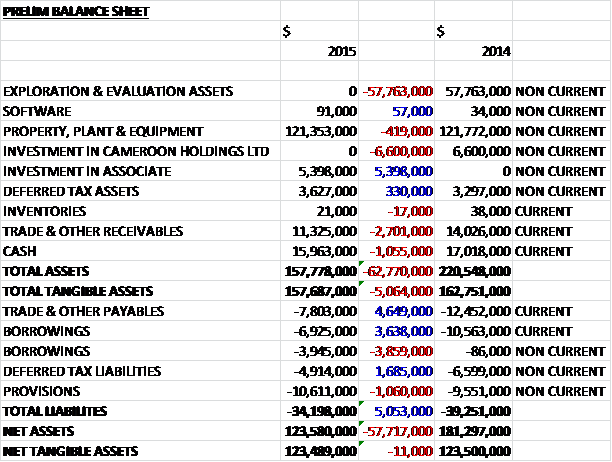

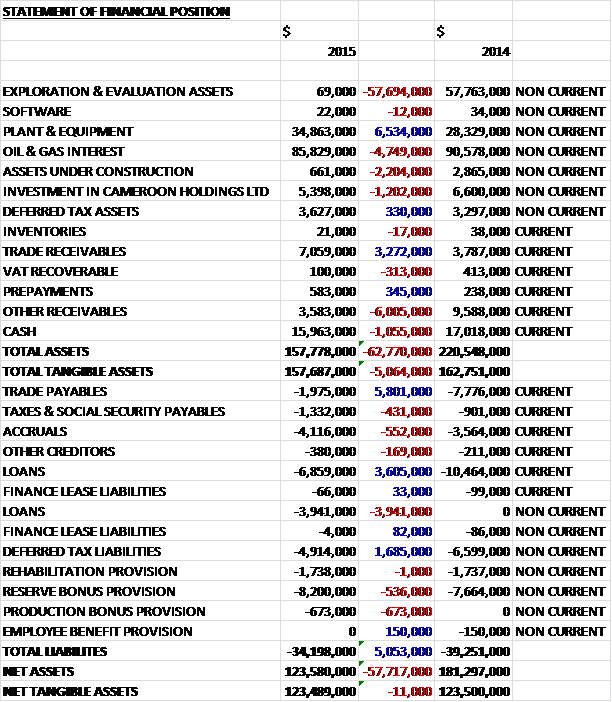

When compared to the end point of last year, total assets fell by $62.8M driven by a $57.8M decrease in exploration and evaluation assets in Russia, a $6.6M decline in the investment in Cameroon Holdings, a $2.7M fall in receivables and a £1.1M decline in cash, partially offset by a $5.4M investment in associate – possibly this is the prior investment in Cameroon Holdings? Total liabilities also fell during the year as a $4.6M decline in payables and a $1.7M decrease in deferred tax liabilities were partially offset by a $1.1M increase in provisions. The end result is a net tangible asset level of $123.5M, almost exactly the same as it was last year.

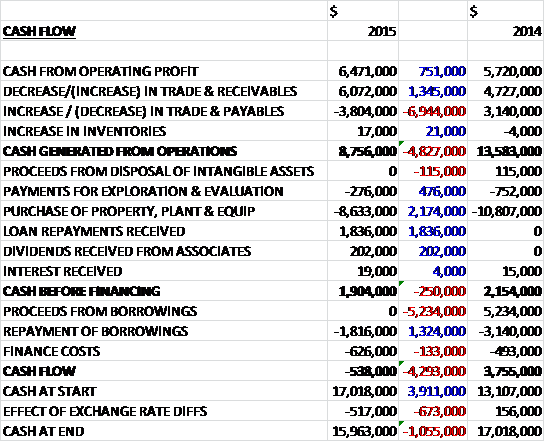

Before movements in working capital, cash profits increased by $751K to $6.5M. A large fall in receivables meant that the cash generated from operations came in at $8.8M but due to the big swing to a fall in payables, this was some $4.8M below that of last year. The group spent all of their cash on property, plant and equipment but due to a $1.8M loan repayment paid to the group, the cash inflow before financing was $1.3M which the group used to pay back borrowings to give a cash outflow at the year-end of $538K and a cash level of $16M. This is actually not that bad in my view.

During the year there have been a number of notable achievements. There has been an increase in monthly average gas production from 2.72mmscf per day to 12.39mmscf by the year-end. In addition they have reached an agreement with Cameroon’s national electricity generating company, EMEO, to provide gas to installations at the Bassa and Logbaba power stations in Douala via take-or-pay contracts that secured revenue for at least the next two years and they delivered the first gas to the grid through the company. They also completed the main Douala pipeline network, crossing the Wouri River to the far shore, opening up new markets in that growing area; and they purchased the Logbaba gas processing plant and started planning for expansion to double capacity to about 40mmscf per day.

During the year the group made its first connection of the first gas-fired electricity generation sets to customer sites in Douala. The four sites connected were all existing thermal customers who needed a consistent supply of electric power to overcome regular grid blackouts. Through an agreement with a third party, the group leased 1.5MW gensets and installed them at dairy Camait, plastic mouldings company Icrafon, flour mill SCTB, and the Guinness brewery. Despite import related delays in delivering this new product line during the past year, once released by port authorities, the gensets were installed and running at the customer sites within a month.

The installation of the gensets provided the group with the first new derivative product from Logbaba gas in addition to thermal combustion. Now that the concept has been proven, the four retail power customers are expected to take over genset rental contracts directly from the supplier and the group will be gas supplier only to these customers.

Work on the spur pipeline to the Dangote Cement works was also completed in early 2015. The clinker grinding and bagging facility, located at Douala port, was commissioned in early June 2015 and has been a consistent and slowly increasing customer of gas since this time. The group also completed connections on the Douala main shore to customers such as Socapursel, a food manufacturing business and SOTEX, a textile manufacturer.

A key task this year has been to establish a presence on the Western Bonaberi shore across the Wouri estuary which hosts a number of potential customers and also has the space for industrial developments requiring port access. As well as the main pipeline under the river, the group also laid some 1,129 metres of branch lines in the Bonaberi-Magzi estate area with the first customers connected within five weeks of crossing following flow testing. New Bonaberi thermal customers were Sopriacam, a cooking oil and soap refinery; New Foods, a biscuit manufacturer; and Sasel, a salt manufacturer. These three customers are now consuming gas and the group are confident of adding at least eight more in 2016.

Other than the newly commissioned Dangote plant, all new thermal customers were previously using HFO for boilers driving mechanical plant and processes. The group worked with these businesses to demonstrate the cost savings expected to occur following conversion to gas and then implemented individual engineering solutions that ensured an efficient conversion for these customers.

In December the group signed terms with ENEO, Cameroon’s electricity company, to supply gas to two power stations located in Douala. The Bassa power station was located 300m from the existing Northern pipeline and the Logbaba power station was located 1.3km along the proposed eastern leg of the main line. ENEO needed to produce a total of 50MW of power from the two stations.

The agreement with ENEO was a significant gas supply contract for the group in terms of scale and revenue generation, with guaranteed minimum take or pay gas consumption at a fixed $9/mmbut over the two year contract term which can be extended by mutual agreement. The minimum take of pay levels are $9mmscf/d in the dry season and $3mmscf/d in the wet season but the group expects actual demand from ENEO will be higher than the minimum levels during both seasons based on ENEO advising them that they need to supply 50-80MW of additional power to the city grid for each of the next five years. Altaaqa was engaged to provide power generation equipment to the project and took responsibility for importing and installing the gensets at the power stations.

In March the group announced the first supply of 4.5mmscf/d of gas to the 16 Altaaqa gensets installed at Bassa. Following the pipeline connection to Bassa and the installation of the gensets, 20MW of gas generated power was being fed into the grid for the first time. In April, it was announced that the Logbaba power station project was online and delivering 30MW to the grid. This meant that the 50MW target under the ENEO agreement and the group’s responsibilities to deliver gas to both stations ad been met. This principle delivery factor triggered the take or pay conditions in the contract with the total project being delivered within four months of the contract being signed.

In May the group announced that it had made payment in full for the purchase of the Logbaba gas processing plant from Expro for $2.6M using cash generated from operations and contributions from RSM. Ownership of the plant has significantly reduced monthly operating costs there.

Going forward the demand for gas in Cameroon for thermal and power generation is estimated to be in excess of 150mmscf/d and the group need to grow production to meet this demand. The task now is to ensure that the group have the reserves and capacity to be able to deliver new allocations of gas to new customers and markets so they are now planning to drill two new wells at the Logbaba concession site. These wells are primarily twins of the wells completed in the 1950s which produced good gas flows. Spudding of the first will be in the first half of the 2016 calendar year and the group are planning on funding these wells from internal cash flow, bank finance and partner contributions and at this stage they do not expect to need to seek shareholder funding (this doesn’t sound that certain).

The group is currently the only supplier of natural gas to Douala. It owns and manages the whole value chain from the wellhead to customer connection and has supply contracts with customers at prices from $9/mmbtu to $16/mmbtu and the country’s gas price is not subject to regulation. The group obviously intends to maintain its position as a dominant gas supplier to industry in Douala and will seek to act as a gas consolidator in the region. Compressed Natural gas and dedicated small power users can all be allocated gas in addition to maintaining the supply to the regional electricity generator. The group have also begun to look at other opportunities within the country and have been in discussions with several participants in the sector about possible joint ventures and farm-in projects.

The core business has been somewhat insulated from the effects of the major shift in oil pricing but during the year they have had to withstand the competitive price pressure of heavy fuel oils. The group’s gas products are currently more attractive than HFO due to no storage costs, transparency, cleanliness and reliability but in the end, price is possibly the most important consideration. One of the focuses during the year was to bring online new product applications for GDC gas. The most obvious usage was that of power with existing thermal customers in the private sectors requesting the group to apply their gas for an electricity generation solution.

During the year the group decided to completely impair their West Medvezhye Russian asset which generated a loss of $49.8M. The directors continue to pursue ways to derive value from the asset through farm out, joint venture, or sale but this has been challenging due to the state of relations between Russia and the West, combined with the low oil price.

During the year, two new non-executive directors were appointed, with both James McBurney and John Bryant joining during the year. It has also been announced that Ahmet Dik will join the board of the group as CEO of GDC. He has worked with the business for two years, being instrumental in concluding the terms with ENEO, and in time it is the intention that he will step up to the CEO position of the group as a whole, which will enable the executive chairman to relinquish his role as interim CEO which would be a positive move.

The group have a net cash position of $5.1M compared to $6.4M at the end of last year but I could not find any EPS broker forecasts which is a bit of a pain.

Overall then, this seems to have been a solid year for the group. If we discount the Russian impairment, the loss was better than last year and they must be pretty close to breaking even. The net tangible asset level was flat and the operating cash flow fell year on year, but this was due to a large working capital inflow last year and cash profits were up year on year. The group is also very close to generating some free cash flow too.

Operationally a lot of progress has been made. The average gas production has increased from 2.72msf/d to 12.39 and the contract with ENEO to provide gas to two power stations has gone live. Additionally, they have laid enough pipeline to reach the far side of the river which should open up some new customers. Of course there are some risks. The need to expands means that there are plans to drill two wells – these will obviously cost money but this is probably the time to be doing it when hopefully drilling costs are lower. The possibility of the issue of new shares for these drills can’t be ruled out. Also, although the group is sheltered from the declining oil price, a continued fall with start to make HFO look better value.

In conclusion, I thought these results read better than I expected. The company is very close to generating proper profits and some free cash so I am keeping close watch here.

This chart looks rather interesting.

Victoria Oil and Gas has now released its annual report for 2015 which contains a bit more detail.

We can see a bit more detail on those admin costs and it seems that the increase came from a $973K growth in wages, a $1M increase in professional fees and a $465K growth in office costs. Those other gains and losses relate to a foreign exchange gain compared to a hefty loss last time and a $722K discount on the settlement of debts. The improvement in finance costs was mainly due to the lack of any loan finance fees.

When compared to the end point of last year, total assets declined by $62.8M driven by a $57.7M impairment of the Russian exploration asset, a $6M fall in other receivables, a $4.7M decrease in the oil and gas interest, a $2.2M decline in assets under construction, a $1.2M fall in the investment in Cameroon Holdings and a $1.1M decline in cash, partially offset by a $6.5M increase in plant and equipment and a $3.3M growth in trade receivables. Liabilities also declined during the year due to a $5.8M fall in trade payables, and a $1.7M decline in deferred tax liabilities. The end result is a net tangible asset level of $123.5M, flat year on year.

In January 2014, the group signed a loan agreement with BGFI of Cameroon. The principal facility of $8.3M was taken out to fund pipeline extensions, customer connection work and installation of gensets at customer premises. The facility is payable at a rate of 7.25% per annum repayable in 36 monthly instalments and the outstanding balance at the end of May was $6M. The balance owing on the Noor Petroleum loan is currently $4.7M and this attracts an interest of 6.5% per annum.

At the end of May the group had $16M of cash which had fallen to $13.5M by the end of October. The directors expect that the group will be able to generate enough revenue to fund its operations for the next year at least. Given the debt levels of $10.9M, the net cash position should be about $2.6M at the moment. It should be noted that at some point RSM will become entitled to its participating interest share of revenue but it is not clear when this might be.

On the 5th November the group released an update for Q3 (this confused me a bit until I saw the later RNS regarding a change in reporting year-end to the end of the calendar year. This quarter was the first full period specifically covering the wet season in Cameroon since they started supplying gas to ENEO and it is the lowest demand period due to the seasonal increase in power output from the country’s hydroelectric dams. The take or pay terms in place with ENEO split minimum payment levels between the wet and dry seasons. Bearing this in mind, average daily gas production was 8.2mmscf/d with 718mmscf of gas sold compared to 12.6mmscf/d and 1,120mmscf in Q2 and 4mmscf/d and 368mmscf in Q3 last year. The group sold 10,878bbls of condensate compared to 13,445bbls and 5,667bbls respectively. This was actually higher than expected as ENEO exceeded its take or pay minimum quota for the period by 32%.

The cash level at the end of the quarter was $12.8M compared to $14.2M at the end of last quarter primarily as a result of a $2.4M debt repayment. The cash received from gas and condensate sales was $8.1M, a 17% reduction on the $9.8M received last quarter.

Having purchased the Logbaba gas production plant in the previous quarter, the group has agreed terms for the operation and maintenance of the plant with Expro (the company they bought the plant from in the first place). They also commissioned a design study with Expro for the expansion of the gas production plant from its existing 20mmscf/d level to up to 40mmscf/d. During the quarter they continued to assess the investment case for potential pipeline expansion into the Bonaberi area and customer connections.

The group have appointed Petrofac to undertake well planning and project management of the upcoming Logbaba drilling campaign planned for 2016, which will target two new wells. The planning, design, and procurement of services and materials for the next two wells, La-107 and La-108, is progressing on schedule. La-107 is to be a twin for the La-14 well drilled in 1957. This well’s objectives include the development of the Upper Logbaba reserves identified in La-104 and to prove lower Logbaba resources that were found there. The La-107 well design also encompasses an option to drill an exploration tail below the base of the Logbaba formation at about 3,200m.

The second well being planned, La-108, is a step-out well into the 2P area of the Logbaba field. The bottom hole location will be about 1,100m to the South East if the drilling pad surface location and is intended to prove up the 2P reserves in the vicinity of the well and to move the 2P reserves into the 1PD, proven developed category. It is intended that the wells will be funded from internal cash flow, bank finance and partner contributions but at this stage it is not expected to require shareholder funding, although clearly this is an option being considered.

The group continue to look for opportunities to expand its hydrocarbon sales. Compressed Natural Gas presents them with the opportunity to distribute gas from the Logbaba gas production plant to a wider network that the gas pipeline currently offers. They are in discussions with a partner who will fulfil all of the capital and operational requirements for the gas compression and distribution of CNG which will enable customers up to 250km from Douala to be provided with gas.

So, overall this seems to have been a fairly robust quarter considering that it is usually the lowers production period during the year. The next quarter will see the tailing off of the wet season in terms of production and expected increased production. The future drilling of new wells offers both risks and potential rewards and until the costs of these wells are more clear I feel the prudent option would be to stay out of the shares for now – I may reconsider this position though.

On the 17th December the group announced the appointment of Iain Patrick as a non-executive director. Iain co-founded PWX Ltd, a consultancy providing business development support to a number of oil and gas companies. In 2006, he was appointed as director of commercial & legal affairs of Gulf Keystone before joining Edgo Energy as commercial director in 2008. He is currently CEO of the oil and gas consultancy Trinity Energy, and serves as a non-executive director for Madagascar Oil and Gas. The company is also considering an additional director to be appointed in 2016 which is an interesting decision given the fact that most of their peers are looking to restrain costs and conserve cash.

On the 20th January the group released an operations update covering Q4. The period marked the third quarter of supply to ENEO and overall production was in line with expectations. The continued erosion of the global oil price has had minimal effect on the business in terms of either gas price changes or customers changing back to oil. The quarter covered the second half of the wet season and average daily production was 7.1mmscf per day compared to 8.2mmscf per day in the previous quarter, of which 3.4mmscf was attributable to grid power. January marks the return to the dry season and associated higher gas utilisation with the grid power sector now recording consistent consumption in excess of 9mmscf per day. This increase is due to the take or pay terms with ENEO.

At $7.6M revenues in Q4 were below the Q3 total of $9M and the net cash position was $5.9M compared to $4.9M at the end of Q3.

Thermal gas sales remained reasonably consistent with the previous quarter, although there was a decline from 350mscf in Q3 to 315.3mmscf in Q4 and management expects this to continue until the capital expansion projects are completed. Grid power sales declined from 367.6mmscf in Q3 to 310.3mmscf in Q4 but consumption is expected to increase significantly during H1 2016 with the first two weeks of the year producing an average of 15.3mmscf per day. Condensate sales are a by-product of the gas production process and volumes sold of 8,608bbls in Q4 compared to 10,878bbls in Q3 reflect these volumes.

The drive in 2016 is to ensure there is sufficient capacity to bring on major new customers by increasing reserves, plant capacity and pipeline reach. At present the production plant capacity is constrained at 20mmscf per day. In addition, finding new applications such as CNG that can add capacity for the existing markets remains a priority.

The group is a 60% holder in the Logbaba concession but is currently entitled to 100% of revenue generated from the project. The concession agreement provides for this allocation of revenue to continue until gross revenues equal the initial exploration costs incurred in the drilling of the two operational wells. Management expects that this point will be reached during H1 2016 and thereafter revenues will be split in accordance with the participating interests which will obviously impact on profitability.

Overall then, sales have fallen quarter on quarter but should increase considerably from Q1 following the start of the dry season. I think the fact that the partner in the Logbaba concession will start earning 40% of the revenues, however, could have a big impact on profitability so now is probably not the time to jump in here.

On the 28th January the group released an operations outlook. The business is beginning 2016 with average daily gas production rates of over 15mmscf per day and aim to increase annual production by 30% during the year. Despite the massive fall in the price of oil, the group has managed to maintain its gas prices at $9 to $16 per mmbtu.

The group will be drilling two new wells in the Logbaba concession in 2016 with spudding of the first well anticipated by the middle of the year. Both wells will be drilled on the current site with well LA107 a twin of well LA104 previously drilled in the 1950s and well LA108 a step out well adjacent to known formations. Petrofac has been engaged as project consultants to help complete the well programme and planning is advanced with a suitable rig secured. Whilst drilling onshore Cameroon is more expensive than in established gas producing regions, the company is taking advantage of the current slump in the hydrocarbon services market to ensure the most cost effective and efficient programme is implemented. The aim is to complete drilling by the end of 2016 and they expect to add new reserves as well as transfer 2P reserves into the 1P category.

In the first half of 2016, the group plans to finalise designs to expand the Logbaba gas processing plant to provide increased capacity. Expansion of the plant is necessary to allow them to process the increased production expected from the drilling programme and pipeline expansion into the Bonaberi area. Expro International has been engaged to complete a study on the design and costs to increase the capacity of the processing plant over three stages to 40mmscf per day. Stage 1, which will expand capacity to 25mmscf per day, is expected to be completed in 2016. The group has received the initial reports on the options available and the next phase is to provide a cost and schedule that ties into the expansion phase of the project from the gas supply side.

The expansion of the pipeline network into Bonaberi will allow the group to access industries that need room to expand or build away from the crowded Douala environment. Before the drilling programme is completed, they expect to have phase 2 commissioned and phase 3 of the pipeline underway. This will provide access to a number of new customers and twelve new gas supply agreements have been signed for businesses on the proposed pipeline. Maya Oil are located at the end of the phase of this expansion and are expected to be a significant consumer of gas, estimated at 0.3mmscf per day.

The group have suggested that they are in discussions to supply additional gas to power projects with ENEO and others and have also mentioned that they are implementing a strategic plan to target other countries in Africa which is an interesting development, although it would be good to get Cameroon cash flow positive first.

During 2016 the revenues from the Logbaba project will be split between the participating interests which will reduce cash coming into the group. The board have indicated that they will fund their capital projects via a combination of strong and established operational cash flows, partner contributions and debt – no placings then? Interestingly the board have also commented that they will endeavour to distinguish the group’s business and from other companies in the oil and gas sector so that they attract an appropriate equity market valuation – I am not sure how they intend to do this, and they will also enhance reporting, transparency and corporate governance which is good to hear.

Overall then, it sounds like quite an exciting year ahead for the group with the new wells planned and other expansion projects. The fact that no placing is planned is good news but I can’t help being concerned about the effect of the revenue split between the partners in the Logbaba concession.

On the 18th February the group announced that it had reached an agreement with Glencore Cameroon and Afex Global on the Matanda Block, a large hydrocarbon license in Cameroon. The terms include the assignment of Glencore’s 75% interest to the VOG with the company becoming the block’s operator. As consideration for the assignment, the group will assume responsibility for carrying out a work programme to be agreed by the Cameroon government. The block covers an area of about 1,235 square kilometres and is prospective for significant natural gas and condensate resources.

The other player in the block is Afex, a Bermuda-based exploration and production company and with this partner the group will initially focus on prospects in the onshore license area located close to the Logbaba area and the existing pipeline network currently operated by Victoria. They will submit a new work programme to the government for approval and expect to start the first phase of seismic data acquisition in Q4 2016.

The board believe that the North Matanda Field has considerable potential and that it is an extension of the Logbaba structure. The block is certainly sizeable, some 60 times larger than their existing concession. It is believed that the concession has a strong geological continuation with Logbaba and tests from three wells already drilled prove a rich condensate yield varying from 30bbl/mmscf to more than 70bbl/mmscf.

It is estimated that the concession has a P50 gas in place volume of 1,864Bcf with condensate in place of 136Mmbbls and ta recent well drilled in 2013 shows a deeper gas reservoir that has not been included in these estimates.

Overall then, this seems like a good, opportunistic acquisition but I wonder how the group will pay for the work programme as well as the up-coming wells to be drilled at Logbaba.