Wentworth Resources is an East Africa focused oil and natural gas explorer and producer. They are incorporated in Canada and listed on the Oslo Stock exchange and AIM – quite an eclectic mix! There are two operating segments – Tanzania, the Mnazi Bay Concession, and Mozambique, the Rovuma Onshore Block.

The Mnazi Bay concession covers approximately 756km2 and has five wells that have been drilled to date. Four wells are capable of producing natural gas from two discovered gas fields and one has been plugged and abandoned. Field operations also encompass natural gas field infrastructure including two processing plants and a 27km pipeline. The interests in production operations at the concession are M&P, the operator with 48%; Wentworth with 32% and TPDC with 20%.

The Rovuma onshore block in Northern Mozambique covers nearly 12,000km2, the majority of which is onshore. Three wells have been drilled on the block to date, two of which encountered hydrocarbons but were considered non-commercial. The third well encountered 11m of natural gas net pay and evaluation of this discovery is ongoing. The partners in the concession are Anadarko, the operator with a 35.7% interest; M&P with a 27.7% interest; Wentworth with an 11.6% interest; PPT Exploration & Production Public Company with an interest of 10%; and Empresa Nacional de Hidrocarbonetos de Mocambique with a 15% interest.

The group currently just supplies one 18MW gas fired power plant in Mtwara in Tanzania at an average price of $5.36/mmbtu but the real step change will be the commissioning of the new pipeline to connect the capital. The group currently has developed reserves of 3.46MMBoe (1P) and 4.84MMBoe (2P) with total 1P net reserves of 11.36MMBoe and 2P net reserves of 15.91MMBoe.

Wentworth has now released their final results for the year ended 2014.

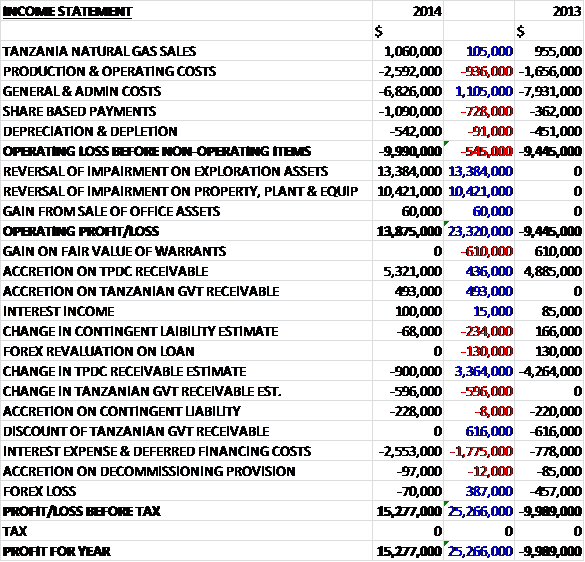

The group made $105K more in natural gas sales than last year due to higher demand from new electricity customers and lower downtime experienced at the power plant, but the total for the year was still only $1.1M. This was dwarfed by the $2.6M of production and operating costs, which increased by $936K year on year as the company prepares for the ramp-up in operations next year, offset by the $1.1M fall in general and admin costs. After a $728K increase in share based payments which, at $1.1M were higher than all the revenue from gas sales, the underlying operating loss stood at $10M, an increase of $545K year on year. The group benefited from a reversal of impairments on both tangible assets and exploration assets, however, to give an actual operating profit some $23.3M higher than last year at $13.9M. We then see a large amount of finance costs and income, in particular a positive accretion on the TPDV receivable of $5.3M and a large increase in interest expense and deferred financing costs at $2.6M relating to the repayment of the Vitol Loan, to give a profit for the year of $15.3M, a positive swing of $25.3M when compared to last year.

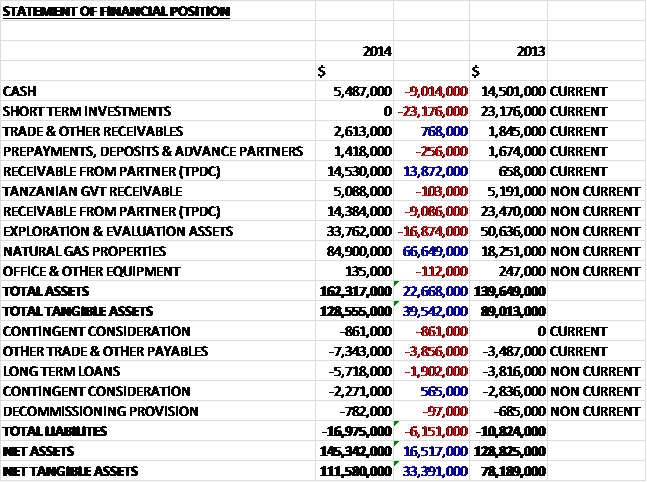

When compared to the end of last year, total assets increased by $22.7M driven by a $66.6M growth in the value of natural gas properties and a $4.8M increase in the receivables due from TPDC, partially offset by a $23.2M fall in short term investments, a $16.9M decline in the value of exploration assets as $53.1M was transferred to property, plant and equipment including the costs associated with three existing wells and field infrastructure within the Mnazi Bay concession that will be utilised in the production of discovered natural gas, and a $9.1M fall in cash. Liabilities also increased during the year due to a $3.9M increase in payables and a $1.9M growth in long term loans. The end result is a $33.4M increase in net tangible assets at $111.6M.

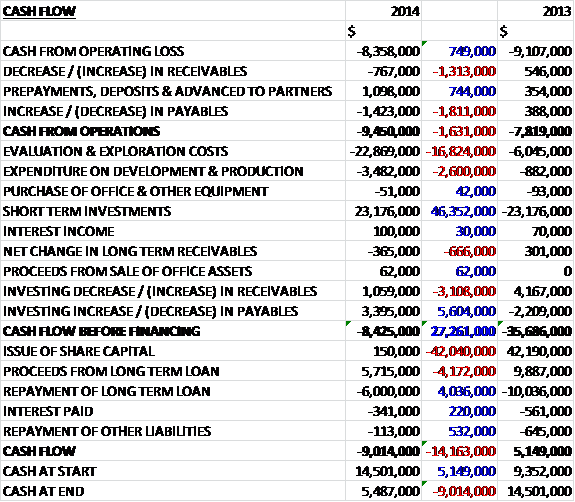

Before movements in working capital, cash losses fell by $749K to $8.4M. A small outflow in working capital, in particular a fall in payables, meant that the cash outflow from operations stood at $9.5M, an increase of $1.6M year on year. The group then spent $22.9M on evaluation and exploration relating to $7.9M on 2D seismic acquisition in Tanzania and $14.1M on exploration drilling in Mozambique, along with $3.5M on development and production relating to $443K on the development well, $1.1M on the field infrastructure connection to the pipeline and $1.9M on other field development, but there was an inward flow from “investing” working capital so that before financing, the cash outflow stood at $31.6M. Surely the $23.2M gained from short term investments is financing, not investment and after taking that into account the cash outflow for the year stood at $9M and the cash level at the end of the year was just $5.5M.

During 2015, the Tanzanian government sponsored gas pipeline project is planned to be commissioned and fully operational. The Mnazi Bay concession is currently the only gas concession in the country with significant discovered gas readily available to feed into the pipeline. TANESCO plans to add another 1,200MW of electricity to the national grid over the next three years by constructing four power stations at Kinyerezi on the outskirts of Dar es Salaam, with additional plants at Kilwa and Mtwara. The current status of the pipeline project indicates that start-up and commissioning are planned to occur in April with a ramp-up to full operations and completion of the project estimated to be in June. The government entity, TPDC will be the operator of the pipeline upon its completion.

There are a number of elements that need to be completed before Wentworth is able to deliver gas to the pipeline. Gas from Mnazi Bay will be sold to TPDC at the fiscal metering station and inlet flange immediately adjacent to the existing company owned gas infrastructure on the Msimbati peninsular at Mnazi Bay. TPDC is responsible for the cost of delivery to the end user and the cost of processing the gas at the Madimba gas processing facility. The connection infrastructure, comprising of the tie-in of the four production wells, a gas gathering system including 7km of pipeline, primary liquid separation and the fiscal metering station will link the Mnazi Bay gas infrastructure to the Madimba GPF and is on schedule for completion in April.

The government’s Madimba GPF is being constructed within the Mnazi Bay concession and is located 11km from Wentworth’s existing gas infrastructure. At peak capacity the facility is planned to have a total capacity of 210mmscf/day consisting three 70mmscf/day trains. Engineering and construction oversight is being provided by Worley Parsons with construction of the facility undertaken by Chinese Petroleum Engineering. So far the Madimba GPF is about 94% complete and commissioning of the facility is expected to commence in April. Foundation work for all the equipment of the gas plant, mechanical installation of the de-hydration units, condensate storage and construction of a treated waste water discharge pipeline are nearing completion.

The main gas pipeline from Mtwara to Dar es Salaam will have a maximum capacity of 784mmscf per day and is now approaching 99% completion. Government representatives indicate that the pipeline welding, trenching, lowering of the pipe and fibre optic cable into the trench, backfilling and hydrostatic pressure testing is complete with the main ongoing activity being pipeline drying. The gas receiving facility at Kinyerezi is located on the outskirts of the capital and is the end point of the pipeline. At this location, gas will be distributed to end users including delivery to the Kinyerezi power generation complex located about 1km away from the gas receiving facility. This station is about 99% complete with only minor civil works, including cement laying, outstanding. The receiving station is scheduled to be commissioned in April.

The majority of gas supplied by Wentworth to the pipeline will be used for power generation, whilst a small percentage may be for industrial use. There is currently spare capacity in excess of 200MW at the TANESCO owned power plants which equates to demand of about 50mmscf per day. This current spare capacity presents an immediate demand for Mnazi Bay gas from the Ubongo I and II power plants, the Symbion plant and the Tegeta plant. The new 150MW Kinyerezi-1 power station is under construction and is expected to be commissioned in June. This power station will add about 30mmscf per day of new demand when it becomes operational. Additional future gas demand is expected to come from the planned expansion of Kinyerezi-1 (33mmscf/day) which is expected to be commissioned by July 2016 and the construction of Kinyerezi-2, 3 and 4 which are expected to be completed by the end of 2017 along with the Kilwa power station and the Mtware power plant in 2018 at which point the total demand for natural gas from the pipeline will be about 450mmscf/day.

In September the company agreed a long term sales agreement with the government of Tanzania. The Mnazi Bay concession partners are contracted to supply up to a maximum of 80mmscf per day of natural gas during the first eight months after the commercial operations date with an option to increase over time to a maxim 130mmscf/day of natural gas during the 17 year supply contract period. The agreement is subject to certain conditions, including the government providing environmental permits and approvals and providing an executed version of payment security agreements prior to delivery of first gas which are currently being finalised.

The initial delivery of gas within the agreement is expected to occur prior to the end of April and is at a fixed price of $3.07/mmscf. Following the delivery of initial gas, the company expects to deliver gas in May which will ultimately be sold to end users by TPDC. Contractual payment terms will apply to initial gas and sales gas resulting in cash flow for the company which is expected to start in July. The company’s existing four wells in the concession are expected to produce a combined 80mmscf/day and are therefore able to meet the volumes specified by the agreement (just about) but currently one of the wells is producing at 2mmscf per day which is limited by the gas demand of an 18MW gas fired power station located at Mtwara.

A fifth development well, MB-4, is expected to start drilling operations in Q1 2015 and is expected to be completed by June with an initial production of 20mmscf/day. This additional well allows for the flexibility to test reservoir performance while still being able to supply 80mmscf/day within the first eight month period of the agreement. The company expects two wells to be tied in to the connection point to the new pipeline by march with a third tied in by the end of April, the new development well by June and the existing producing well by the end of September. Subject to the deliverability from the existing wells and additional development wells, the company expects gas sales to the pipeline to increase to 130mmscf/day by Q1 2016 and they could escalate up to 270mmscf/day within five years should additional exploration success occur in the concession.

Two key development activities were initiated following the signing of the agreement. Engineering, design and construction of field infrastructure necessary to tie-in the company’s existing wells to the pipeline was started along with planning the drilling of the new development well. The surface infrastructure includes the installation of separation facilities and flow lines and the EPC contract has been awarded to TPF Basse from Belgium who are fully mobilised to site. A detailed engineering design is complete and a 10 metre by-pass pipeline, allowing delivery of gas to TPDC in advance of the separation units becoming operational is expected to be completed by April. Long lead time items have been procured and the separation facilities are expected to be on location and operational in Q3 and construction has commenced on tying-in of existing wells and installing flow lines.

During Q1 2014, the acquisition of 58km of high resolution 2D seismic was completed over the existing discovered Mnazi and Msaimbati gas fields and processing of the data is ongoing and will be used to help determine the location of future development wells. The new infill development well is expected to start drilling operations in Q1 2015 with well site preparation and civil works having been commenced during Q4 2014. The rig is currently being mobilised to the well site location and drilling operations are expected to be complete by June.

In Mozambique, drilling operations of the frontier Tembo-1 exploration well were completed and a natural gas discovery was made in Cretaceous aged sands. The well took over six months to drill and complete and was drilled to a total depth of 4,553 metres. Petrophysical analysis of the Cretaceous section indicates 11 metres of natural gas net pay. Natural gas and some condensate was recovered by modular formation dynamics testing but the partners do not plan any further evaluation of the well and will assess all the data recovered to determine the potential commerciality of the discovery with an evaluation by Anadarko anticipated within the next few months.

In January drilling operations of the Kifaru-1 exploration well in the concession commenced. This well targeted Miocene, Oligocene and Eocene sands. It was drilled to a total depth of 3,100 metres but failed to find an economic reservoir and was plugged and abandoned in February. The government of Mozambique has accepted the drilling of this well as fulfilment of the third phase exploration drilling obligations which expires in August. During 2015 the partners plan to analyse data from both wells in order to determine the next steps and an appropriate work programme for the rest of the year.

Trade and other receivables predominantly comprises amounts due from government departments in Tanzania, tax input credits for goods and services tax in Canada and VAT in Tanzania and Mozambique. The company’s ongoing exposure to receivables from Tanzania Electricity Supply Company Ltd (TANESCO), the state power company, is connected with the gas sales from the Mnazi Bay Concession to the gas-fired power plant located in Mtwana. At the year-end the Mnazi Bay concession partners were owed fifteen months of gas sales with $2.4M owing to the group. After the year-end TANESCO settled three months of arears totalling $483K. The construction of the gas pipeline project may provide an opportunity for TANESCO to operate more efficiently and generate positive cash flow and it is expected that this will mean that the group eventually receive full recovery of the receivables.

In 2009 the company and TPDC entered into a joint operating agreement relating to the Mnazi Bay Concession. Under the agreement, TPDC has a 20% participating interest in the production from the concession and will pay the company for 20% of the past costs incurred on the concession from TPDC’s share of future production. In addition, the TPDC’s share of costs incurred after that date, which are paid by the company, will be recovered by the company from TPDC’s future production and this receivable is subject to an interest charge of one month term LIBOR plus 2% per annum. The accretion over the expected term of the asset is based on future expected cash flows from the concession. A long term receivable of $33.5M is due from TPDC. The company receives a significant portion of TPDC’s share of gas production from the Mnazi Bay concession directly from the operator before TPDC receives cash from its share of the revenue. There is a risk that future production from the concession may not be sufficient to settle the receivable. The receivable has been discounted to $28.9M due to its long term nature but with the passage of time and the move closer to recovery, the carrying amount of the receivable is accreted up to the case value with a corresponding credit to the income statement. It is estimated that the full value of the receivable will be recovered by two years after the delivery of first gas to the pipeline which should provide a significant source of cash flow for Wentworth.

The company has an agreement with the government of Tanzania to be reimbursed for all the project development costs associated with transmission and distribution expenditures at cost. An audit completed in 2012 verified costs of $8.1M reimbursable of which a total of $1.6M has been recognised as a credit against this cost due to tariff equalisation funds and VAT input credits. At the year-end a receivable of $6.5M related to the company’s disposal of transmission and distribution assets and various costs associated with the Mtwara Energy project was due from the Tanzanian government and the group is currently in discussions with the various parties on agreeing a method of reimbursement, which may not be in cash.

During the year there was a reversal of impairments where previous contingent resources were classified as reserves. The market for the company’s discovered gas has evolved to an advanced stage of certainty in Tanzania. The company signed a long-term gas sales agreement in September to deliver natural gas to a government owned transnational pipeline at a fixed price of $3/MMBtu escalating annually at US CPI which has led to the reversal.

As a result of an asset purchase and sale transaction in 2012, the company may be obliged to make payments of $3.4M should certain future gas production thresholds from Mnazi Bay be reached.

There remains 5M warrants outstanding on the company’s shares with an exercise price of $0.648 per share. There are also nearly 10 million options outstanding on the company’s shares with some 5.6 million currently exercisable. This figure includes 3,750,000 granted during the year with an exercise price of $0.69 which seems like a lot to me given the company is not yet really making any money.

A the year-end the group has cash of $5.5M to fund its planned activities prior to the commissioning of the Mtwara to Dar es Salaam gas pipeline which is expected during Q2 2015. During Q4 2014 they secured two credit facilities totalling $26M with a Tanzanian bank. An amount of $6M was used to pay an existing loan with the remaining facility used to fund development capital within the Mnazi concession in Tanzania. The loan is 48 months in duration and bears interest of 6 months LIBOR rate plus 750 basis points subject to a floor of 8% per annum and a ceiling of 9.5%, which seems like a hefty rate to me. After a grace period of one year, repayments are payable in six semi-annual equal instalments.

At the year-end there was $6M drawn down on the facility. So with the undrawn loan amount and the current cash, there is $25.5M available to the company. There is expected to be significant free cash flow from Q3 2015 from the pipeline but the drilling of the MB-4 development well and field infrastructure costs are expected to be $9.2M and $9.8M respectively which gives a total of $6.5M after these payments. The costs attributable to Wentworth on the Kifaru-1 exploration well in Mozambique that have not already been paid are $4.2M which brings the headroom down to just $2.3M. The current expectation is that the financial position is sufficient for operations as far as the current timetable is concerned but if there are any delays (quite likely in my view) the company will have to raise more capital – for which it is exploring operations.

As well as all the receivable outstanding, the group is also having discussions with the Tanzanian government over alleged unpaid taxes. In July they issued tax assessment certificates totalling $2.1M of alleged unpaid payroll taxes and withholding taxes on imported services and certain accounting transactions plus late penalty interest totalling $2.1M for the period 2008 to 2012. In November the Tanzanian Revenue Agency accepted the company’s objection to a withholding on certain accounting transactions and a tax liability of $666K was waived. The company has recorded a liability of just $281K against these taxes. They continue to communicate and provide clarification on the remaining $3.2M and the company believes it has a strong case against the remaining assessed amount and have not recorded a provision against it. A date has not yet been set by the TRA board to hear the tax appeals. Such are the risks of operating an oil explorer in Africa.

The company has some oil and gas concession commitments going forward. On the Romuva onshore block in Mozambique there is a new minimum expenditure net to Wentworth of $2.1M relating to the drilling of the exploration well, Kifaru-1 that was commenced in January 2015.

One risk is clearly the fluctuation of crude oil and natural gas prices. There is some insulation from this effect because the group has an agreement with the government of Tanzania to supply natural gas from the Mnazi Bay concession at a price of $3/MMBtu, escalating at US CPI annually over a 17 year term. There is some exposure to exchange rate risk primarily in respect of the Tanzanian shilling and Canadian Dollar against the US dollar. A 10% increase in the Tanzanian shilling against the US dollar would result in a charge of about $18K.

The company is still loss making and is expected to remain so in 2015 but if we look forward to 2016, the consensus forward PE ratio is a very undemanding 4.4. Of course a lot can happen between now and then but this looks quite cheap to me. Obviously there are no dividends planned for this year and there are none planned for 2015 with any cash going into further development and paying back the loans.

Overall then, this looks like an interesting little company. Although there was a profit recorded this year, it was only because of impairment reversals and there is obviously an underlying loss because the one power station customer is not enough to keep the lights on. The big hope is the new pipeline connecting the capital which will open up a large market for the company’s gas. The group went through considerable cash reserves this year, burning through $31.6M before financing due to the preparations for connection to the pipeline.

There seem to be a number of operational issues. There is a huge amount of receivables due from TPDC as it seems Wentworth has been covering their costs up to now, although once the pipeline is connected the cash should start flowing in from them. Probably harder to obtain will be the receivables from the state owned TANESCO who seem to pay for their gas whenever they want and not when requested by Wentworth! Additionally the receivable from the Tanzanian government is likely to be difficult to obtain in my view and on top of this, the government is now trying to extract unpaid taxes from the company.

The pipeline is due to come on stream by April with the first cash flow coming in by July. These timings are very important as it seems to be the company could run out of cash before then. There is $5.5M cash left, plus the $20M left undrawn from the loan facility but after the development well and other infrastructure is paid in Tanzania there will only be $6.5M and a further $4.2M to pay for the exploration activities in Mozambique which leaves just $2.3M left. Any delays in cash flow from the pipeline could mean the company has to raise further cash somehow. Delays are probably quite likely in my view given the difficult operating environment in the country.

In all, I feel that this could be a good investment soon but the falling oil price is unhelpful and the timings for cash flow look a little too tight for me at present so I will keep a watching brief here.