Wentworth Resources has now released its interim results for the year ending 2015.

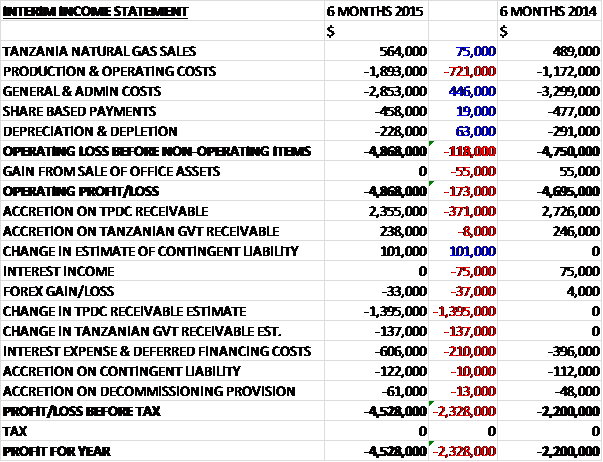

When compared to the first half of last year, natural gas sales increased by just $75K due to slightly higher demand from new electricity customers and lower downtime at the power plant. This was dwarfed by a $721K increase in operating costs due to the $600K recognised relating to the estimate cost of settlement of the ongoing tax audits, partially offset by a $446K fall in admin costs due to downsizing of office space, streamlining IT infrastructure and optimisation of the corporate structure to give an operating loss of $4.9M, an increase of $173K year on year. There were then various adverse movements in finance costs and gains with the largest differences being a $1.4M change in TPDC receivable estimate, a $371K fall in the TPDC receivable accretion and a $210K increase in interest expense. The end result is a half year loss of $4.5M, an increase of $2.3M when compared to the first half of last year.

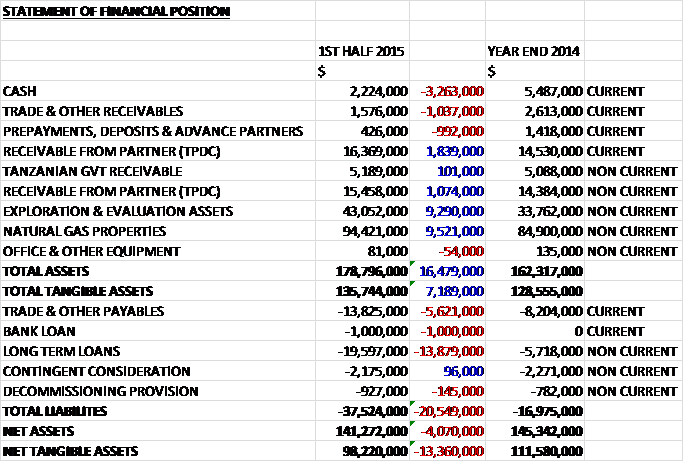

When compared to the end point of last year, total assets increased by $16.5M at the half year point, driven by a $9.5M increase in natural gas properties, a $9.3M growth in evaluation and exploration assets, and a $2.9M increase in the TPDC receivable, partially offset by a $3.3M fall in cash, a $1M decline in trade receivables and a $992K fall in prepayments. Liabilities also increased during the year due to a $13.9M increase in long term loans, a $5.6M growth in payables and a $1M increase in the current aspect of the long term loan to give a net tangible asset level of $98.2M, a decline of $13.4M over the past six months.

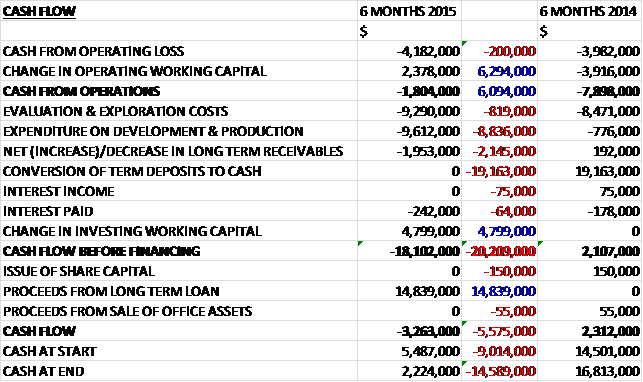

Before movements in working capital, the cash loss increased by $200K to $4.2M for the first half of 2015. After working capital movements, the operational cash outflow was $1.8M, an improvement of $6.1M year on year. The group then spent $9.3M on exploration costs relating to $8.6M spent on the drilling of the Tembo-1 and Kifaru-1 wells in Mozambique, $507K in indirect overheads in Mozambique and $151K relating to 2D seismic processing in Tanzania; $9.6M in production development relating to $7.9M spent on the MB-4 development well, $1.4M spent on Tanzania field infrastructure connection works and $277K spent on other field development; and $242K on interest. There was also a net increase in long term receivables and a $4.8M favourable movement in “investing working capital” to give a cash outflow before financing of $18.1M. The group drew down on the long term loan to give a cash outflow for the half year of $3.3M and a cash level of $2.2M at the period end.

The pipeline is now expected to be completed and commissioned in Q3 2015 and the final handover from the construction contractor, China National Petroleum, to TPDC is expected to occur in November. All connection infrastructure is planned for completion in Q3. Mechanical, electrical and instrumentation installation for the de-hydration unit and other equipment; civil works for all the equipment and control room for the gas plant; and condensate storage tank site erection and painting activities are ongoing. Construction of the Madimba GPF is complete with start-up and commissioning of the facility expected to take place during Q3. The start-up and commissioning of the pipeline commenced in July. The completed gas receiving station is scheduled to be ready to deliver gas to the end users during September.

As a reminder the Mnazi Bay partners are contracted to supply a maximum of 80mmscf/day during the first eight months after commercial operations date with an option to increase over time to a maximum 130mmscf/day during the supply contract period which lasts until 2031. Negotiations on the payment security arrangements are at an advanced stage and are expected to be concluded during Q3 in line with expectations.

The company’s existing five wells within the concession are expected to produce a combined 80mmscf per day which should cover the initial delivery volumes. The recently completed MB-4 well which intersected the Miocene gas reservoirs with a net pay of 24 metres in the Upper Mnazi Bay and 43 metres in the Lower Mnazi Bay zones, has been selectively tested at different two hour stabilised flows with the upper bay achieving a flow rate of up to 18.8mmscf/day and the lower bay of up to 22.2mmscf per day. The MB-3 well is still producing at 2mmscf/day, limited by the demand of an 18MW gas fired power station.

In terms of readying the existing five wells to deliver gas to the new pipeline, MS1-X and MB-3 will be tied-in to the connection point by mid-August, MB-2 and MB-4 are scheduled to be tied in and commissioned by the end of August and MB-1 will be tied in during Q2 2015. The company anticipates gas sales to the pipeline to increase to 130mmscf/day as market demand grows and deliveries could escalate to 270mmscf per day within five years subject to the drilling of additional development wells.

As well as the drilling of the MB-4 well, the surface infrastructure activity comprising the installation of separation facilities, piping, flow lines and civil works was ongoing. Progress during the period included the completion of the by-pass infrastructure at the Msimbati Plant gate, allowing delivery of gas to TPDC in advance of the separation units becoming operational; long lead time items were procured; existing wells were tied-in and flow lines installed for MB-3 and MS1X; and work on the tie-in of MB-2 and MB-4 was ongoing with a target of completion in Q3. The surface infrastructure allowing the flow of gas from all production wells to the Madimba GPF is expected to be fully operational during Q4 2015.

Given the immediate access to a market for Mnazi Bay gas and the spare capacity available in the pipeline, the company expects to initiate and exploration drilling programme in 2016, a significant proportion (but not necessarily all) of these activities are expected to be funded from internally generated cash flow.

In Mozambique, the company continued discussions with the partners on the Rovuma block on a possible appraisal of the Tembo-1 gas discovery. All work commitments on the block have been fulfilled and the third and last exploration phase expires at the end of August, subject to any appraisal of the Tembo-1 discovery. Anadarko, the operator and PTTEP have indicated their intention to exit the block on this date. The fourth well, Kifaru-1 failed to find an economic reservoir.

In July, the company provided formal notification to the Mozambique government of its intention to proceed with an appraisal of the Tembo-1 discovery. During Q3, priorities are determining the participation interests of the joint venture partners remaining in the block and appointing an operator in addition to agreeing an appraisal work programme and budget and establishing the appraisal area. A definitive plan going forward is subject to a resolution of these issues and approval being granted by the Mozambique government to continue with an appraisal programme. The rest of the block acreage with the exception of the agreed appraisal area will be relinquished at the end of August.

At the period-end an undiscounted long term receivable of $36.2M from Tanzania Petroleum Development Company (TPDC) as outstanding and the company is basically waiting for the cash to flow from the pipeline before this can be paid back which should start to occur from 2016 and it is hoped that the recovery of the receivables will be fully collectable within two years from delivery of first gas and this should provide an important source of cash flow for Wentworth. There is always a risk that future production from the Mnazi Bay concession may not be sufficient to settle the receivable which would then require a provision.

There is also still a $6.5M long-term receivable from TANESCO that remains uncollected and the company continues discussions on this matter. The group is also owed some $1.4M from eight months-worth of gas sales to the 18MW gas fired power station. It is hoped that the new pipeline will provide an opportunity for TANESCO to operate more efficiency but I am not as positive about that as Wentworth management. They expect to eventually receive full recovery of current and future gas sales to TANESCO but they have been slow in settling invoices so far.

At the end of last year the company had estimated $280K was likely to become payable for alleged unpaid payroll taxes and withholding taxes on imported services, certain accounting transactions and late penalty interest. In June, the TRA issued an amended tax assessment certificate that indicated a total liability of just $140K so the company recorded a credit adjustment of $140K. During Q2 2015, the TRA conducted a tax audit for the period 2009-2012 on a discontinued subsidiary of the company. They issued a notification that tax assessment certificates of $740K will be issued for alleged unpaid withholding taxes and payroll taxes along with $610K for alleged unpaid VAT. The company has recognised a liability for the first set of charges but believes it has a strong case against the VAT tax issues so has not provided for that liability.

No options were granted during the period and some 10M remain outstanding at an average price of $0.58 per share.

At the period end the company had cash of $2.2M and a further $5.2M available to draw down on the existing credit facility. In July they completed a private placing which raised $7.6M through the private placing of 15,412,269 shares at 32p per share, which gives a total of about $15M to play with, which is not really that much given that current liabilities stand at $14.8M relating to amounts due to the operators of the company’s assets in both Tanzania and Mozambique. Should additional exploration and development activity take place prior to generating sufficient cash flows from gas sales to the new pipeline or should there be delays beyond Q4 2015, additional funding may be necessary. It is also worth noting that repayments on the loan will commence in Q2 2016 and the group went down the road of doing a placement because they found debt difficult to source given the challenging macro oil and gas environment which is a little concerning.

After the initial delivery of gas in Q3, management expect to ramp up sales so that they will exit 2015 generating significant free cash flow to fund future growth and finance exploration activities. The company is still loss making so there is no PE ratio this year which is expected to remain the case for the rest of 2015, although the consensus forecast for 2016 suggests a forward PE of 4.4 which is very cheap if it can be relied upon.

Overall then, this is still a company that interests me but the good times continue to be just out of reach at the moment. The loss increased year on year, mainly as a result of a decline in the TODC receivable estimate and the provisions for the tax audits. The group got through about $18.1M of cash in the first half of the year before financing and as we can see, this is not sustainable. The new producing well in Mnazi Bay looks pretty decent but given Anadarko’s decision to leave the concession in Mozambique, I am not holding out much confidence that the Tembo-1 well has found much of interest.

The opening of the pipeline has been put back to November, which should not come as much of a surprise and the first cash flow from the gas sales will not now arrive until the end of the year. The delay meant the company had to do another placing as they found debt hard to come by due to the poor oil and gas environment at the moment. As far as I can tell, the company has $2.2M in cash, $5.2M in further debt and $7.6M from the placing but this $15M is not going to last long given the $14.8M of current liabilities due on the two concessions. This is looking very tight to me and any further delays are going to make things rather uncomfortable. This is so frustrating as I really do think there is great potential here. I will remain a very interested onlooker.

After a brief improvement in July, the shares seem to have resumed their downward trajectory.

On the 20th August the group released an update covering operations at the Mnazi Bay Concession. Gas deliveries have now commenced to the new pipeline in Tanzania. Two wells are now producing and the remaining three wells will be put on production in the coming months. Initial production volumes will be used for commissioning purposes and to fill the pipeline. Production rates are expected to increase to 70 mmscf/day by October and reach 80 by the end of the year. Gas deliveries by TPDC for use by power and industrial companies are expected to commence in October. The partners will receive payment at the end of each calendar month for sales volumes delivered during that month. As a reminder, the gas sales price has been set at $3.07 per thousand cubic feet, rising in line with US CPI.

The partners have agreed payment security terms with TPDC , the buyer of the gas and various other parties which provides sufficient assurance that sales of gas will be settled in accordance of the agreed payment terms. The MD expects to exit the year in a strong financial position.

This is the update I was waiting for. I was concerned that there could be further delays to the commissioning of the pipeline so that now gas is actually being delivered, these are mostly allayed. There are still concerns over the tight financial position and whether TPDC will actually pay on time but on balance I have decided to take a position here. I expect a bit of a choppy ride!

On the 4th November the group released an operational update for Mnazi Bay. The gas production facilities at Madimba, the Mtwara to Dar es Salaam pipeline and the Kinyerezi gas receiving facility have now been fully commissioned and are operational. Mnazi Bay gas is currently being used to generate power in Dar es Salaam at the existing Ubungo-II and Symbian power plants, as well as the new Kinyerezi-I power plant. Production volumes into the pipeline are currently at 33mmscf per day from three wells on a restricted flow basis, and are expected to reach 80mmscf per day once all the generators of these three power plants are fully operational, which is expected in Q4 2015.

Three of the five existing wells at Mnazi Bay have been successfully brought on stream with well performance in line with expectations. The fourth well is expected to be tied in during November and the fifth well is expected to be tied in and ready to produce into the new pipeline in Q1 2016.

Sales gas volumes of 1,032mmscf were delivered to the new pipeline during October at an average of 33mscf per day and a gross payment of $3.8M to the joint venture partners has been received from the Tanzania Petroleum Development Corp. Under the gas sales agreement, the sale price has been set at $3 per million NTU, about $3.07 per thousand cubic feet, rising in line with the US CPI industrial index starting in 2016.

All this seems fairly good as things seem to be progressing as expected.