Zytronic has now released its final results for the year ended 2015.

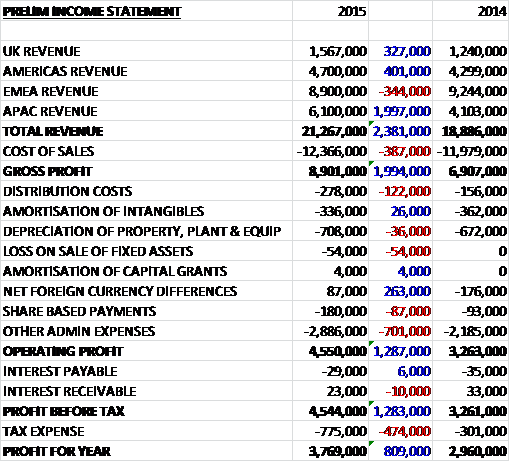

Overall revenue increased by £2.4M when compared to last year due to a £2M growth in Asian Pacific revenue, a £401K increase in Americas revenue and a £327K growth in UK revenue, partially offset by a £344K decline in EMEA revenue. After a modest increase in cost of sales, the gross profit increased by £2M. Distribution costs were up £122K and share based payments increased by £87K with a growth of £701K in other admin costs mainly resulting from increased staff costs but there was a £263K positive movement in foreign currency so the operating profit was some £1.3M ahead of last year. Interest payable and receivable broadly cancelled each other out but the tax expense increased by £474K due to a rebate last year following over provision in previous periods to give a profit for the year of £3.8M, a growth of £809K year on year.

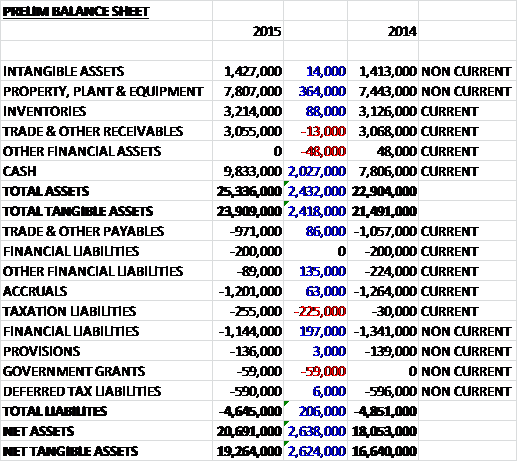

When compared to the end point of last year, total assets increased by £2.4M driven by a £2M growth in cash and a £364K increase in the value of property, plant and equipment. Conversely total liabilities fell during the year as a £232K decline in financial liabilities, as the group pays off its mortgage, was partially offset by a £225K increase in current tax liabilities. The end result is a net tangible asset level of £19.3M, an increase of £2.6M year on year.

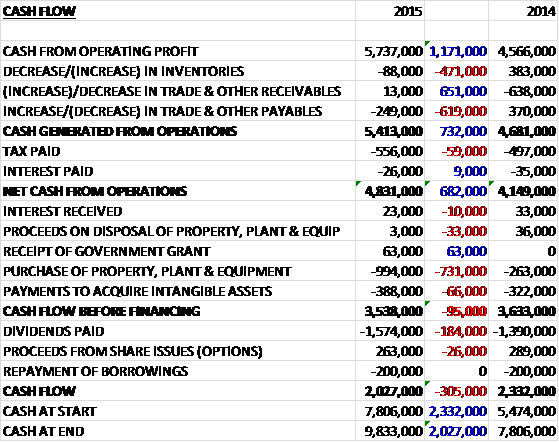

Before movements in working capital, cash profits increased by £1.2M to £5.7M. There was a small outflow of cash due to working capital, in particular a fall in payables and the tax payment was modestly higher which meant that the net cash from operations came in at £4.8M, a growth of £682K year on year. The group spent £994K of this on tangible assets with £400K spent on the refurbishment of the original cleanroom to increase capacity, and £300K on a new lamination machine. They also spent £388K on developing intangible assets to give a free cash flow of £3.5M before £1.6M was spent on dividends and £200K was paid off the mortgage to give a cash flow for the year of £2M and a decent cash pile of £9.8M at the year-end.

The improved performance this year is principally as a result of a 16% revenue growth in the touch sensor products. The total volume of sensor units sold increased by 10,000 to 149,000 with increases in sensors of over 15” but declines in smaller sensor sizes.

The largest area of export growth was attributed to sales to the Asia Pacific region which saw a £2.3M increase in South Korean sales to £2.8M, mostly supplies into the gaming market with sales to China, which is driven in the main by ATM sales, accounting for £1.9M of total revenues and remaining unchanged year on year. The most significant year on year reduction affecting the region was the end of life of an agricultural telematics project for an Australian customer, which significantly contributed to the £300K reduction in revenues in that country.

The EMEA region remains by far the largest export market but sales reduced year on year, mainly as a result of a £500K reduction in non-touch product revenues in the financial market across Germany, Hungary and the Netherlands. Other contributing factors were associated with the vending market with a fuel service payment terminal touch project in Benelux which concluded at the start of the second half of the year.

In the Americas, gaming revenues are predominantly driven by direct supply into Las Vegas based equipment manufacturers for casino cabinet slots, which during the year reduced as some machines approached end of life and new designs were being developed, with a change in the resultant supply chain this year through South Korea. This period has benefited from the substantial increase in the purchase of units through Canada for the Coca Cola Freestyle drinks dispensing touch project, which was triggered by an end of life notification for the LCD unit used in the existing design.

The main driver of growth in the UK was the work undertaken by the group in providing ultra-large format touch products to an interactive table manufacturer for the retail sector, and a project for a car showroom deployment across a number of European outlets associated with the launch of a new car model.

The revenues from non-touch products were flat year on year, although above management forecasts. This was mostly attributable to the £400K of revenues generated by the uptake of a curved non-touch display unit into Asia Pacific, used in the same design of casino cabinets as the touch sensor provided. In total, non-touch ATM product revenues increased by £600K but revenues from the largest contributor of ATM display filter glasses did decline, down £600K when compared to last year.

The financial market continues to be the group’s largest, accounting for £6.3M of revenues. This year continued to benefit from a new platform launch by one of their major ATM customers, were the group is supplying multiple different sized touch sensors used in the same ATM machine. Consequently this, combined with a level of growth from existing designs, gave a total volume increase in ATM units. As with last year, they have once again experienced a reduction in financial type kiosks, partly countering the increase in ATM volumes.

Vending machines maintains its ranking as the second largest touch market for the group with revenue growth of 24% to £3.7M. There were two main factors that influenced the overall performance of this market during the year, the first being the positive uplift in the Coca Cola project mentioned above where the uplift in the volume of sensors sold was nearly double that of 2014. This was countered by a volume and revenue reduction of sales across the fuel vending application area, however, which in the main had an effect on EMEA sales.

Sales into the industrial market for human machine interface control devices and general application kiosks were similar to those of last year at £2M. Significant growth in the year was seen in the gaming market which showed the highest percentage growth of all touch markets at 80% to £3.4M and about a third of all units supplied were for a new curved 42 inch MPCT design, supplied through a South Korean integrator customer, replacing a flat designed PCT model to the same end markets. The healthcare market also showed sales growth in both revenue, up £100K to £400K, and volume due in the main to sales to a Singapore manufacturer of a blood analyser unit.

There was a decline in revenues from the telematics and signage markets, the former being significantly influenced by the end of life of an agricultural GPS project which declined by £500K to £100K. Revenues from the signage market declined by £200K as the mix of the supply of larger sized units decreased. The home market which was solely influenced by sales of the Bosch cooktop unit saw an increase and was in line with management expectations.

There are a number of R&D projects ongoing and recently completed. Development has been initiated on a new MPCT controller for sensor sizes under 20 inches. This controller, when coupled with a MPCT sensor will provide tablet-like performance for the harshest environments for up to ten individual touches at the same time. The development has the potential to drive performance and functional improvements into most of the units under 20 inches in size that the group has produced in 2015 and it is expected that a production release will occur early in 2016.

In combination with further developments of the MPCT controller electronics, the group has initiated the design and development of a second Zytronic Application Specific Integrated Chip, which will drive cost savings, performance improvements and PCB size reductions across the MPCT family of controllers with the benefits to become realisable from 2017.

Additional developments have been undertaken to improve material performance aspects of the sensors and include specialist anti-reflective coating materials to improve the optical performance of the touch sensors in bright outdoor conditions as well as antimicrobial glass to aid in reducing the potential for the transmission of microbes from one user to another through the touch interaction process.

During the year the group has partnered with a European Commission consortium group comprising academic and industrial partners to evaluate and develop, over a three year period, high resolution and small feature sized inkjet printing techniques for printed electronics. Their involvement is to determine the potential for a developed solution as a method for 2D printing of metallic fluids for touch sensors, as a means of complementing its present manufacturing processes.

During the year the group opened up a representative office in Taiwan to service sales opportunity generation across greater China. Also, from June, they have employed a regional specialist sales consultancy organisation in Japan to further develop the Japanese market, through close collaboration with its existing sales channel partner, and to provide services and directly promote the Zytronic Japan entity. Unfortunately the initiative in mainland China mentioned in the report last year, did not prove as successful as hoped due to local initiative funding issues in the country which means that it has drawn to a premature close.

Early in the year the group undertook a review of the touch manufacturing capacity and capability requirements across the three factory facilities. This resulted in a capital project being undertaken over the year to remove the oldest section of its original 1989 cleanroom and refurbish its existing 2001 cleanroom to expand into the floor space created. This has increased its total touch sensor manufacturing cleanroom footprint within the business by 25%.

In addition they invested in new 2D direct write electrode printing machines and a further automated laminator, to increase the throughput of ultra large touch sensors. A new computer controlled glass profiling machine was also installed to replace an older obsolete machine, allowing the group to improve the finish of the edges of its glass across much larger glass sizes than previously, whilst extending the range of customisations they can offer in the supply of its bespoke touch sensors.

The new year has started positively with maintained momentum. The board are continuing to focus on increasing shareholder value and will update shareholders on progress and material developments during the course of the coming year. This is an intriguing statement and sounds like there might be an acquisition coming here, although that could be a red herring.

At the current share price the shares trade on a PE ratio of 16.7 and after a 20% increase in the total dividend, the shares have a dividend yield of 3% which seems like reasonable value, although I don’t have any updated broker forecasts for next year yet. The group are currently enjoying a net cash position.

Overall then this has been an excellent year for the group. Profits have increased, net assets grew and operating cash flow was above that of last year with plenty of free cash being generated. The good performance seems to have been driven by a Coca-Cola vending machine project in Canada and strong gaming revenues in Korea along with an interactive table contract and a project for car show rooms in the UK, partially offset by the end of a fuel service payment terminal project in Benelux, the end of an agricultural GPS project in Australia and lower non-touch financial service product sales in Germany, Hungary and the Netherlands.

There seems to be a decent pipeline of products being developed and the increased presence in Taiwan and Japan will hopefully bear fruit, unlike the doomed office in China. There has also been a good level of capex with an increase in cleanroom capacity. So far this year, the positive momentum has continued and with a current PE of 16.7 and dividend yield of 3% with a decent net cash level, these shares still look pretty good value. Of course the nature of the large projects that the group undertakes always leaves them open to a shortfall in revenue at some point but overall I am happy to hold these shares.

On the 25th February the group released a trading update where they confirmed that trading and future prospects remained in line with management’s expectations. Progress continues on various initiatives such as interactive signage, investments in touch sensor output, durable touch technology and expansion in North America.