32 Red has now released its interim results for the year ending 2016.

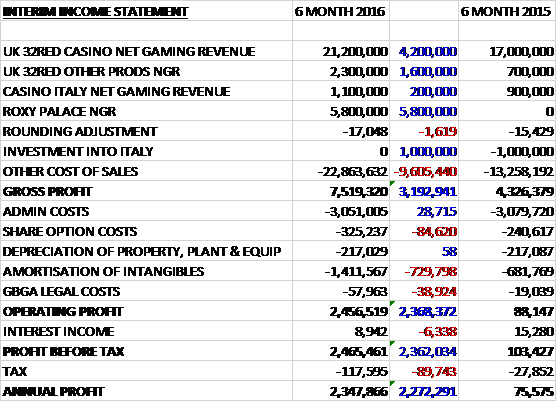

Revenue increased when compared to the first half of last year with a £5.8M maiden contribution from Roxy Palace, a £4.2M growth in casino product NGR and a £1.6M increase in other product NGR. Cost of sales increased by £9.6M which meant that the gross profit was up £3.2M. Admin costs were broadly flat but share option costs increased by £85K and amortisation was up £730K which meant that the operating profit grew by £2.4M. After interest saw a modest increase and tax charges increased by £90K, the profit for the period came in at £2.3M, a growth of £2.3M year on year.

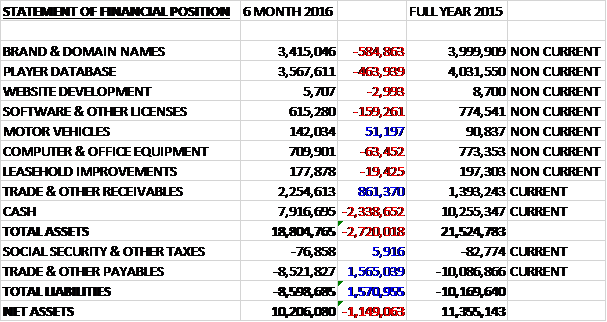

When compared to the end point of last year, total assets declined by £2.7M to £18.8M driven by a £2.3M fall in cash, a £585K decline in brand and domain names and a £464K decrease in the value of the player database. Total liabilities also declined due to a £1.6M fall in payables but this was not enough to prevent a £1.1M decline in net assets to £10.2M.

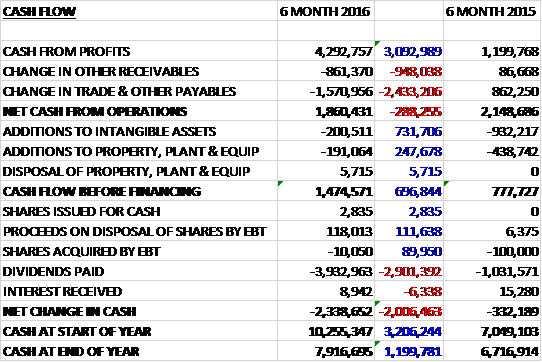

Before movements in working capital, cash profits increased by £3.1M to £4.3M. There was a working capital outflow with a reduction in payables and a growth in receivables so that the net cash from operations came in at £1.9M, a decline of £288K year on year. The group then spent £201K on intangible assets and £191K on property, plant and equipment to give a free cash flow of £1.5M. This did not cover the £3.9M paid out in dividends, however, so there was a cash outflow of £2.3M in the period and a cash level of £7.9M at the period-end.

The 32Red Casino brand continues to achieve strong growth (24%) in direct response to accelerated, returns-driven marketing investment. The launch of a new responsive website in April has also improved retention levels and new player conversion rates. Mobile remained the fastest growing platform, growing by 45%. The Roxy Palace brand will benefit from the roll out of the new website in the second half of the year, before marketing investment is increased to expand this brand.

The growth in revenues from other products is a direct result of increased trade in the sports betting product. In May, the group renewed its commercial arrangement with Kambi sports Solutions, allowing further funds to be allocated to marketing of the sports betting product. Sport betting, whilst still a small part of the overall group, continues to offer a strategic opportunity for the group in terms of customer acquisition, cross-selling and retention, and they will continue to exploit opportunities to leverage the brand in this area.

In August the group aired its first TV advert promoting the sports book and they have signed a twelve month deal to advertise around live sport on Sky, including a number of half time adverts in live Premier League matches. In May they announced a three year agreement to sponsor Leeds United which complements the existing shirt sponsorship of Glasgow Rangers.

The group continues to increase its market share in Italy with revenues up 33% and the business remains on track to break even this year, incurring minimal losses in the first half.

After the period-end, the group agreed a new and extended contract with its digital gaming solutions partner, Microgaming. Under the new agreement, the relationship is extended for a further five years and gives the group the flexibility to utilise alternative providers in order to enable they are able to attract the full spectrum of casino players to the brand.

The group also announced an extension of its exclusive license with ITV allowing them to operate an Ant and Dec Saturday Night Takeaway slot machine game in addition to their current I’m a Celebrity Get Me out of Here game. In addition they have agreed a three year deal to become the sponsor of the King George VI Chase run on Boxing Day and a three year deal to sponsor Haydock Park’s Group 1 Spring Cup run.

Current trading remains strong with like for like NGR up 4% on very strong comparatives in the second half to date, with a 9% growth including the contribution from Roxy Palace. Last time out the group stated that in July, they experienced an unusually weak casino gross win margin which has since started to return to more normal levels. The board remains confident of meeting its expectations for the full year.

At the current share price the shares are trading on a PE ratio of 125.2 which falls to 14.2 on the full year forecast – this is no longer the bargain that it once appeared. After an 18% increase in the interim dividend, the shares are now yielding 4.5% but this falls to 3.6% on the full year forecast as the effect of the special dividend works its way through.

Overall then this has been a good period for the group. Profits are up but net assets have declined. Although the operating cash flow fell with the free cash not covering the dividends, the cash profits rose. There is very strong organic growth here and the sports betting proposition looks like it is gaining traction. So far this year, things don’t seem to be racing along at the same pace. Like for like revenues are up just 4% and the gross margin has suffered in the casino business. This means that the forward PE is 14.2, which is not exactly value territory but the yield of 3.6% is decent. This is a bit tricky, I have a feeling the next set of results might disappoint so am tempted to get out of this for a while.

On the 1st February the group released an update for trading in the year. They delivered an annual NGR 28% higher than last year at £62.3M driven by a combination of a 19% organic growth in the core business and a full year contribution from Roxy Palace. Total casino NGR increased by 26% to £58.5M reflecting the increased marketing investment in the casino brand, a full year contribution from Roxy Palace and healthy growth from the Italian business. Revenue from other products continued to grow strongly, up 60%, primarily driven by the Sports business which is developing as an increasingly important customer acquisition and retention channel. Overall the results are expected to be in line with previous board expectations.

Early trading in 2017 has been strong across the group with revenues in January up 21%. The key contracts signed during the second half of 2016 will help the group deliver its stated growth strategy and the board remains confident of delivering continued progress in 2017.

This all sounds pretty good actually, no mention of margins or EBITDA, however.

On the 23rd February the group announced that they had reached an agreement with Kindred for them to take-over 32Red. Shareholders will receive £1.96 for each share and be entitled to keep the dividend of 4p. This represents a 16% increase on the closing price the previous day. The acquisition has already received irrevocable undertakings relating to 71% of the share capital. This looks to be a done deal which is a shame as I think it undervalues the company. Still, the directors don’t agree with me so I have taken my quick profit from this one.