Swallowfield has now released its interim results for the year ending 2017.

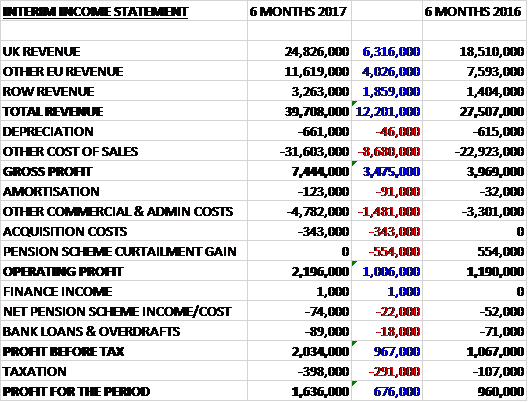

Revenues increased when compared to the first half of last year due to a £6.3M growth in UK revenue, a £4M increase in other EU revenue and a £1.9M growth in ROW revenue. After an increase in cost of sales the gross profit was up £3.5M. There was a £1.6M increase in admin costs and £343K in acquisition costs along with the lack of a £554K pension scheme curtailment gain that occurred last year which meant that the operating profit increased by £1M. Pension and interest costs increased modestly and tax charges were up £291k to give a profit for the period of £1.6M, a growth of £676K year on year.

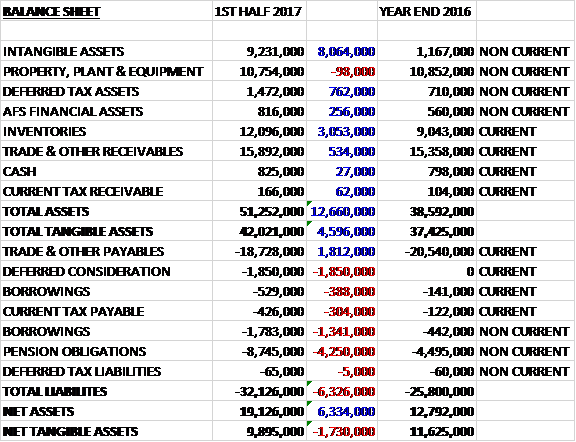

When compared to the end point of last year, total assets increased by £12.7M to £51.3M, driven by an £8.1M increase in intangible assets, a £3.1M growth in inventories, a £762K increase in deferred tax assets and a £534K growth in receivables. Total liabilities also increased during the period as a £1.8M decline in payables was more than offset by a £4.3M increase in pension obligations, a £1.9M growth in deferred consideration and a £1.7M increase in borrowings. The result was a net tangible asset level of £9.9M, a decline of £1.7M over the past six months.

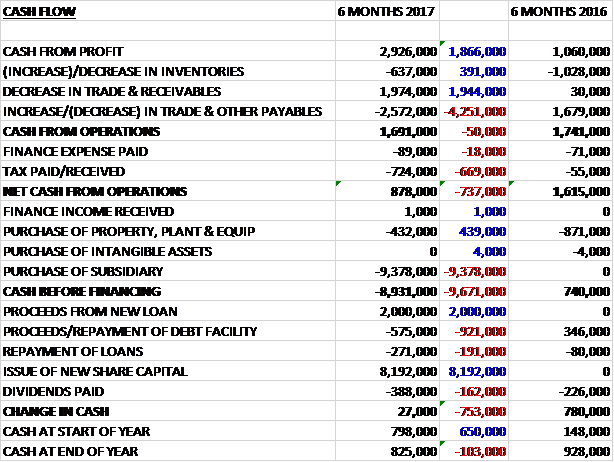

Before movements in working capital, cash profits increased by £1.9M to £3M. There was a cash outflow from working capital and after tax payments increased by £669K the net cash from operations was £878K, a decline of £737K year on year. The group spent £432K on property, plant and equipment along with £9.4M on acquisitions to give a cash outflow of £8.9M before financing. They then took out a net £1.2M of new borrowings to help pay for the dividends of £388K and after the issue of new share capital to raise £8.2M there was a cash flow of just £27K and a cash level of £825K at the period-end.

On the 6th July the group released a trading update covering the year. Overall revenues are expected to show growth of 30% at constant currency to about £74.1M. Like for like revenues, excluding acquisitions, were up 2% on a constant currency basis. Revenue growth has been supported by the strong performance of owned brands, in particular the Brand Architekts’ portfolio acquired in June last year. In the manufacturing business, revenues continued to perform solidly on the back of a stream of innovative new product launches.

As a result of the above, underling business performance is expected to be significantly ahead of last year and in line with market forecasts. At the year-end the group had a net debt position of £3.7M compared to £4.3M at the end of last year. This all seems fine, I continue to hold.