Avon Rubber has now released their final results for the year ended 2017.

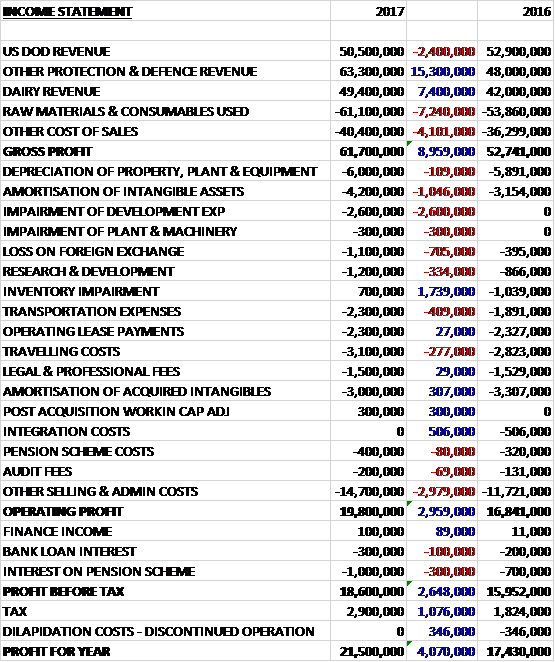

Revenues increased when compared to last year as a £2.4M decline in US DOD revenue was more than offset by a £15.3M growth in other protection and defence revenue and a £7.4M increase in dairy revenue. Raw material costs were up £7.4M and other cost of sales grew by £4.1M to give a gross profit £9M higher. Amortisation increased by £1M, there was a £705K increase in losses through forex, R&D costs were up £334K and transportation expenses increased by £409K. We also see a £2.6M impairment of development expenses and a £300K impairment of tangible assets, offset by a £1.7M reversal of inventory impairments and an £800K reduction in post-acquisition expenses. Other selling and admin costs grew by £3M to give an operating profit £3M higher. Interest payments were up £400K but tax income increased by £1.1M and there were no losses from discontinued operations, which were £346K last year. All of this gave a profit for the year of £21.5M, an increase of £4.1M year on year.

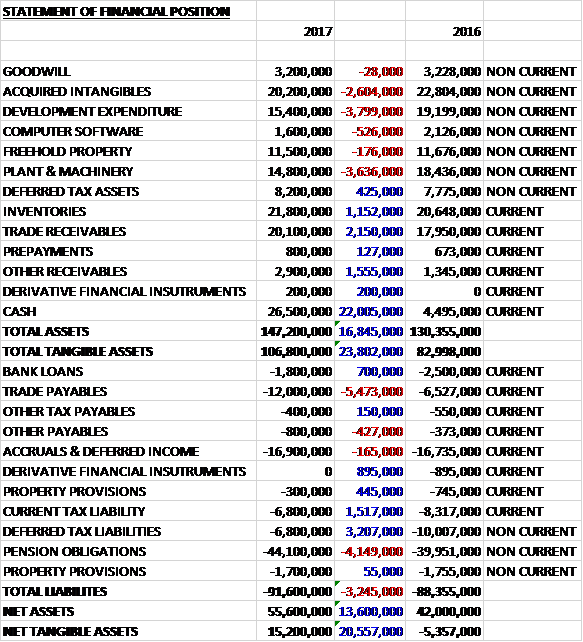

When compared to the end point of last year, total assets increased by £16.8M, driven by a £22M growth in cash, a £2.2M increase in trade receivables, a £1.6M growth in other receivables and a £1.2M increase in inventories, partially offset by a £3.8M decline in development expenditure, a £3.6M fall in plant and machinery and a £2.6M decrease in acquired intangibles. Total liabilities also grew during the year as a £3.2M fall in deferred tax liabilities and a £1.5M decrease in current tax liabilities were more than offset by a £5.5M growth in trade payables and a £4.1M increase in pension obligations. The end result was a net tangible asset level of £15.2M a growth of £20.6M year on year.

Before movements in working capital, cash profits increased by £6.8M to £37.2M. There was a modest cash outflow from working capital and after tax payments increased by £1M the net cash from operations was £32.5M, a growth of £2.2M year on year. The group spent £2.9M on development costs and £2.6M on property, plant and equipment to give a free cash flow of £27M. Of this, £3.2M went on dividends, £1M on their own shares and £800K on loan repayments to five a cash flow of £22M and a cash level of £26.5M at the year-end.

The underling profit in the Protection division was £18.8M, an increase of £5.2M year on year. A £24.2M increase in orders received together with favourable currency movements drove an increase in revenue of 13%. On a constant currency basis, revenue grew by 3.6% with flat military revenue, 6.1% growth in law enforcement and fire growing by 18%. Margins have improved due to the mix of product shipped and cost efficiencies.

Military revenue was up nearly 10% due to favourable forex movements. On a constant currency basis they were flat with the 37,500 FM50 general purpose respirator order offsetting lower DOD revenues. The group delivered 150,000 M50 mask systems and 144,000 filter pairs, compared with 189,000 mask systems and 122,000 pairs of filter spares in 2016. DOD spares and development costs revenue increased by £2.7M due to higher development costs relating to the M69 air crew mask. At the year-end there was an order book of 49,000 systems, including spares of £4.1M relating to 15,000 M50 face piece assemblies. Since the year-end they have received further orders for 118,000 filters and £4.5M of spares from the DOD.

Revenue from ROW military increased by £8.9M to £13.7M primarily due to the delivery of the 37,500 FM50 general purpose mask order. AEF had another soft year with revenues falling by £800K to £4M, reflecting the variability in timing of certain DOD procurement programmes for fuel and water storage tanks. The business experienced strong order intake in Q4 and enters 2018 with an order book totalling £4M. The group’s acquisition strategy will result, in the medium time, in AEF losing the benefits it currently enjoys under the US small business regime and the board are therefore considering the options for the business.

Within Law Enforcement, North American revenues grew by 22% on a constant currency basis to £20M, driven by strong performance in hoods and mask systems as the group continues to convert police forces to their C50 mask. The increase in fire revenue was driven by solid contributions from both SCBA and thermal imaging cameras.

During the year the group has been nominated as the preferred bidder for the resupply and in-service support of the UK MOD general service respirator. They group are actively pursuing further opportunities to broaden their military customer base.

During the year they experienced strong sales momentum in the law enforcement market and have seen increased demand for their escape products. In the US in particular, the group is expanding their market share. Over the mid-term, the board expect market share gains to continue. To cross-sell a broader range of CBRN systems, they look forward to launching their US powered air range once NIOSH approvals are received.

Their market for self-contained breathing apparatus in the fire sector remains competitive and with a fragmented customer base. The board see an opportunity to leverage their technology capability to enhance the product offering in this segment, however, and are in the process of upgrading their system to comply with the new 2018 NFPA standards. They have developed a revised sales strategy to ensure they deliver sustainable growth over the mid-term. The Argus thermal imaging camera technology they acquired in 2015 has been a significant addition to the fire products portfolio and has enabled them to open cross-selling opportunities across the product range.

Going forward, the previously reported M53A1 powered air respirator and M69 aircrew mask opportunities continue to progress with initial DOD orders expected in 2018. The board anticipate that the initial orders under these programmes will offset the non-recurrence of the 37,000 FM50 general purpose respirator order and anticipated lower M50 mask systems deliveries to the DOD during 2018 resulting in stable military revenues.

They expect similar levels of law enforcement revenue growth in 2018 driven by continued conversion of North American police forces to their C50 mask system and continuing demand for their hoods from a range of global customers. They also expect sales of their new PAPR range to build momentum once NIOSH approvals have been obtained. The board anticipate slower revenue growth in fire in the coming year as the growth rate for Argus thermal imaging cameras reverts to a more normal level.

The underlying profit in the Dairy division was £6M, a growth of £600K when compared to last year. Revenue increased by nearly 18% due to favourable currency movements and 6.6% on a constant currency basis. On a constant currency basis, Interface grew revenue by 4.3%, PCI by 20% and Farm Services by 19%. The growth trends reflect increased farmer confidence following sustained improvements in the milk price as the market recovers. Margins have softened due to increased investment to deliver growth in response to the improved conditions.

Interface revenue grew by 4.3% at constant currency driven by growth in Brazil and Europe. North American revenues declined by 1.1% reflecting a further decline in OEM revenues. In Europe, revenue grew by 15.6% and Latin America grew liner revenues by 29% reflecting market share gains in Brazil. Asia Pacific liner revenues declined by 1% as a result of difficult market conditions in China. Sales of PCI products have benefited from increased farmer confidence resulting in higher investment spend. Revenue grew by 20% driven by growth in Europe of 30% and 83% in Latin America, again reflecting their good performance in Brazil. In North America, PCI growth was 3.3%.

Farm Services has continued to show good growth with constant currency growth of 19%, driven by hikes in North America of 17% and 23% in Europe. At the end of the year, Cluster Exchange had grown by 25% to 35,000 cluster points serving 1,891 farms. To increase their European capacity they plan to open a Farm Services exchange centre in Italy in the coming year. During the year they launched the Pulsator Exchange in North America and from a zero base have introduced 478 Pulsators onto 11 farms. Tag Exchange will follow in 2018 with farm pilots underway and progressing successfully. They plan to launch Tag Exchange in both North America and Europe in 2018.

Going forward, the dairy market environment continues to be positive with improved milk prices and low feed costs reflected in increased farmer confidence. In this environment, the board expect that the growth trends experienced this year will continue into the next year, albeit with a moderation in the PCI revenue growth rate to around 10%.

In Avon Protection the most significant investments have been in further developing the M69 aircrew mask, the Deltair SCBA and MCM100 product range. In Milkrite, investment has been focused on expanding their PCI product range. The group has agreed to increase pension payments by £500K next year.

The £2.6M impairment of development expenditure and the £300K impairment of plant and machinery represents the write-down of costs of developing the Emergency Escape Breathing Device. Further development of this product has been terminated as there are limited commercial opportunities in the current market. This product is outside the core CBRN and respiratory range and was primarily developed for a US Navy contract that was awarded to a competitor in 2015.

Last year’s integration costs relate to the acquisition of the Argus thermal imaging camera business and the relocation of the manufacturing of their Melksham site. Last year’s loss from discontinued operations relates to dilapidations costs of former leased premises of a business that was disposed of in 2006.

As can be seen, the group once again received a tax credit this year. The tax credit this year included £7.2M (£4.4M) in respect of previous periods with a £2.3M credit in connection with company restructuring in previous years and the release of provisions following an updated assessment of uncertain tax positions.

This year an error was identified in the process for valuing the share based payments charge to the income statement. The comparative figures for 2016 have been restated to correct the charge which has increased the payment charge from £100K to £1M and to reduce the operating profit by £900K. This is quite a substantial error!

Going forward, the closing order book of £34M together with £26.6M of orders received after the year-end provides good visibility and the group is well positioned to deliver further growth in 2018. Within Avon Protection, the board expect initial orders for the M53A1 powered air respirator and M69 aircrew respirator programmes in 2018, with these orders offsetting the non-recurrence of the 37,000 FM50 general purpose respirator order and anticipated lower M50 mask systems deliveries to the DOD during 2018. In the medium term these programmes together with the UK General Service Respirator revenues are expected to offset any revenue reduction from anticipated lower M50 deliveries once the ten year sole-source contract ends in 2018.

The dairy market environment continues to be positive with improved milk prices and low feed costs reflected in increased farmer confidence. In this environment, they anticipate that the growth trends experienced by the business will continue to the new financial year.

At the current share price the shares are trading on a PE ratio of 17.9 which increases to 18.6 on next year’s consensus forecast, likely as a result of tax charges returning to normal. After a 30% increase in the dividend the shares are yielding 1% which increases to 1.2% on next year’s forecast. At the year-end the group had a net cash position of £24.7M compared to £2M at the end of last year.

On the 8th November the group announced that it had received confirmation from the US DOD of their participation under the joint enterprise contract vehicle. It is a ten year multiple award framework contract which established a group of qualified contractors to compete for orders in relation to chemical, biological, radiological, nuclear and enhanced conventional weapons defence systems, equipment and material.

This is the procurement structure under which two CBRNe programmes, the M53A1 respirator and the M69 aircrew mask system will be purchased. These programmes are potentially significant to the group in the medium term and initial task orders are expected to be received during the course of 2018.

On the 29th November the group announced that CFO Nicholas Keveth acquired 1,794 shares at a value of £20.8K.

On the 6th December the group announced the receipt of an order for 53,000 M50 mask systems worth $14.3M from the US DOD. This order together with the closing order book of 49,000 mask systems at the year-end secures the anticipated sales of the M50 mask systems to the DOD for 2018.

Overall then this has been a good year for the group with increased profits, net assets and operating cash flow, with loads of free cash being generated. Both divisions saw growth with protection being driven by growth in law enforcement and dairy by an improved confidence in the market. Both divisions were aided considerably by favourable forex movements. Going forward, growth is expected again next year with new programmes offsetting a decline in M50 mask deliveries as the contract with the DOD comes to an end. This I think is the main risk at the moment and if the new programmes don’t deliver as expected there could be problems.

The shares are not cheap, with a forward PE of 18.6 and yield of 1.2% but there is plenty of net cash and I am sticking with them for now.

On the 1st February the group released a trading update covering the first four months of the year where they stated that trading has continued in line with expectations. Order intake across the Protection business has remained strong. The military business enjoyed a positive start to the year and continues to build momentum for 2018 and beyond. Orders have been received from the US DOD which secure anticipated sales of M50 mask systems for the current year and contributes towards building the order book for 2019. The ROW military business has received the first commercial orders for the MCM100 underwater rebreather and is seeing increasing interest and orders for the recently launched Powered Air Products.

Law Enforcement delivered a strong start to the year with significant growth in order intake across the portfolio and growing sales of Powered Air Products in Europe and the ROW. The board anticipate receiving US NIOSH safety standards approval for this range in Q2, enabling them to launch in the country later in the year. The fire business has delivered in line with expectations.

Dairy market conditions have remained positive with milk price softness being offset by lower feed prices. The business has continued to perform well with revenue growth within precision control and intelligence and farm services particularly strong.

The continued strengthening of sterling against the dollar will impact results this year. If forex rates remain unchanged for the rest of the year, the adverse translational impact would be around 8% on revenue and profit compared to the previous guidance of 3%.

The net impact of the recently enacted US tax reform will be positive for the group. For the current year, the effective tax rate is around 14%, which includes a one-off favourable revaluation of the US net deferred tax liability and the release of provisions following the positive outcome of certain tax enquired. For future years, the effective rate of tax is estimated to be around 19%.

In conclusion, with a positive start to the year and the continued strong order intake the board is confident of achieving its current year expectations. Forex issues notwithstanding, this looks OK to me and I continue to hold.

On the 15th February the group announced that further to being the preferred bidder for the UK MOD General Service Respirator contract, they have entered into a five year contract with the MOD for the resupply and in-service support of its General Service Respirator. Production is expected to start during the first half of 2019, after product approvals are complete with the contract expected to generate revenues in the order of £16M over the five year period. The group will incur additional capex of £3M across 2018 and 2019 to obtain product approvals and prepare for production.

On the 23rd February the group announced that Chairman David Evans sold 10,000 shares at a value of £117.5K.

On the 3rd April the group announced that it had completed the disposal of Avon Engineered Fabrics, its US-based hovercraft skirt and bulk liquid storage tank business for a cash consideration of $9.25M. The business had been expected to make a small profit during the year.