As a result of the reallocation of resources and a change in the group’s internal reporting, the segments have been redefined as Strategic Marketing, Marketing Activation and Books. The Strategic Marketing segment comprises all the businesses that were previously reported under the Marketing Services segment other than the Field Marketing business which is now reported under the Marketing Activation segment. The segment comprises the Data, Digital and Consulting businesses.

The Marketing Activation segment includes the Field Marketing business, and all the group’s Marketing Print businesses that were previously reported under the Print Services segment other than Clays which is now reported under the Books division. The Marketing Activation segment comprises the group’s Exhibitions and Events, Point of Sale, Print Management and Field Marketing businesses. The Books segment comprises Clays that was previously reported under the Print Services division.

St. Ives has now released its final results for the year ended 2015.

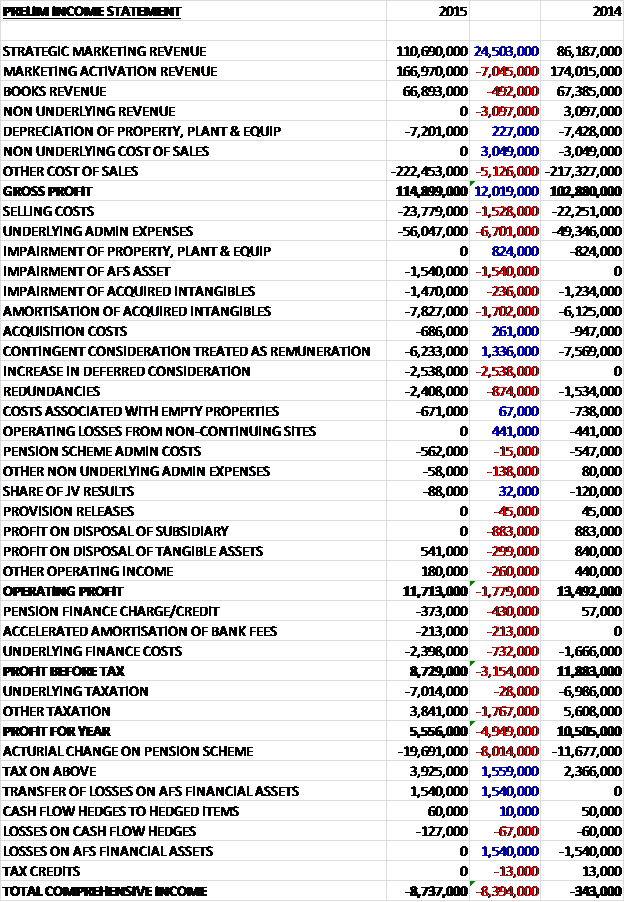

Revenues increased considerably when compared to last year, although organic revenue fell as a £7M decline in Marketing Activation revenue, a £3.1M elimination of non-underlying revenue (broadly offset by a fall in non-underlying cost of sales) and a £492K fall in books revenue was more than offset by a £24.5M increase in strategic marketing revenue. Cost of sales also increased to give a gross profit some £12M above that of last year. We then see selling costs up £1.5M and an “underling” admin cost increase of £6.7M before we get to a huge list of “non-underling” admin costs. We have a £1.5M impairment of an available for sale asset, a £236K increase in impairments of acquired intangibles and a £1.7M increase in the amortisation of acquired intangibles, a £2.5M increase in deferred consideration, an £874K increase in redundancy costs, an £883K decline in profit on disposals of subsidiaries and various other items – most of these happen every year so don’t seem to be very “non-underlying” to me.

The upshot of all this is a £1.8M decline in operating profit compared to 2014. We then see an increase in the pension charge, an accelerated amortisation of bank fees, and an increase in “underlying” finance costs and after an increase in tax, the profit for the year came in at £5.6M, a decline of just under £5M year on year.

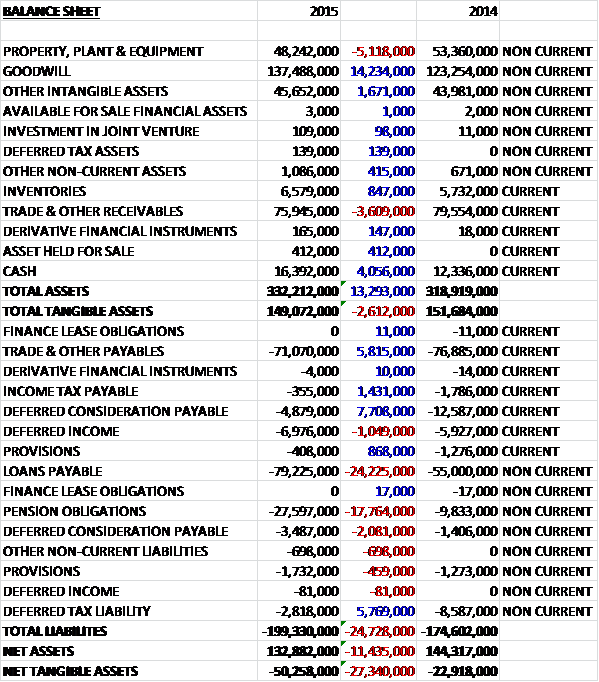

When compared to the end point of last year, total assets increased by £13.3M driven by a £14.2M growth in goodwill, a £4.1M increase in cash and a £1.7M growth in other intangible assets, partially offset by a £5.1M fall in the value of property, plant and equipment along with a £3.6M decline in receivables. Liabilities also increased during the year as a £17.8M growth in pension obligations, and a £24.2M increase in loans was partially offset by a £5.8M fall in deferred tax liabilities, a £5.6M decline in deferred consideration, a £5.8M fall in payables, and a £1.4M fall in income tax payables. The end result is a net tangible asset level of -£50.3M, a detrimental movement of £27.3M year on year – this is not a good balance sheet at the moment!

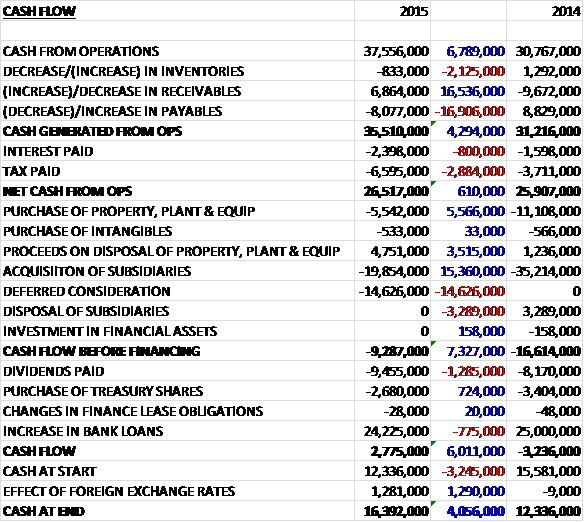

Before movements in working capital, cash profits increased by £6.8M to £37.6M. A fall in receivables was more than offset by an increase in inventories and a decline in payables; and interest was up £800K with a £2.9M growth in tax paid so that net cash from operations came in at £26.5M, an increase of £610K year on year. The group then spent £5.5M on fixed tangible assets relating in part to £3.5M invested in the book segment to meet the additional volume generated by the Penguin contract, £533K of intangibles and £14.6M on deferred consideration. They also made £4.8M on the sale of fixed assets and spent £19.9M on acquisitions to give a cash outflow of £9.3M before financing. We then see a £9.5M dividend payment and £2.7M spent on treasury shares. This was all paid for by a £24.2M increase in bank loans to give a cash flow for the year of £2.8M and a cash level of £16.4M at the year end. I am not sure if this company will ever be self-sustainable as it seems to have to buy growth through acquisitions that it can’t afford out of its own cash flow.

The “underlying” result in the Strategic Marketing segment was £16.3M, an increase of £4.5M year on year which included full year contributions from Realise and The Health Hive acquired last year, along with Solstice acquired in March. Revenues at the data business fell by £2.3M to £33.2M with the fall due to a significant one-off software sale within Occam in the previous year (worth £2.4M)and a change in work mix in Response One but both of these factors helped to improve the margin in the year. Response One introduced a new analytics proposition and improved its digital capabilities. In addition, Occam has significantly expanded its remit within JLR and they are now delivering services intro them through both Occam and Amaze One. Occam has also secured a number of new wins, including Car Giant, Healthspan, Sainsbury’s Retail Technology Services and the RAC.

The digital division saw revenues increase from £27.8M to £45.5M. Amaze saw a number of significant new client wins throughout the year. It has established a core strength in advising manufacturers who are transacting directly with their customers for the first time and in the delivery of B2B commerce solutions with both areas currently experiencing significant market growth. Following the launch of Amaze One, the CRM collaboration between Amaze and Occam, the business has progressed well, winning projects for the Arcadia Group and Royal Mail while also extending its CRM remit with Northern Rail.

Branded3 has achieved a number of new business wins throughout the year, securing the search engine optimisation account for First Direct, which further extends their remit with the company, as well as winning contracts for Halfords, Chelsea FC and Durham University. Realise has continued to build its business both within the UK and internationally. Highlights included a digital transformation project for Greyhound in the US and international digital marketing campaigns for Disneyland Parks and Expedia. In addition, the business has had a number of new significant new business wins including Nikon in Europe and Hewlett Packard & Sutter Health in the US. Moving forward it is the intention to bring the digital businesses closer together in order to collaborate on large scale multi-discipline, multi-territory digital client mandates.

The consulting business saw revenues of £32M, an increase of £9.1M when compared to last year. Incite continues to grow internationally in response to client demand. It has seen strong growth in New York and Singapore having opened offices in both markets during 2013, and has secured a number of significant new business wins. Following this expansion, the business opened an operation in Shanghai this year, winning its first new client mandates in the region at the end of the financial year.

Pragma has also seen an increase in demand for overseas projects with airports and commercial spaces in particular being high growth areas with the business advising on the commercial strategy of Mexico City International Airport. Hive, the healthcare communications consultancy the group acquired in May 2014, has integrated well into the group and continues to add new clients to its roster with substantial wins from three pharmaceutical companies. Its patient journey mapping product is a strong growth driver for the business with recent new project wins from Bayer, Novartis and AbbVie with this area expected to see continued momentum into next year.

The “underlying” profit in the Marketing Activation division was £10.9M, a decline of £409K when compared to last year. Trading conditions within the division were mixed with growth in Service Graphics and SIMS offset by a reduction in POS revenue caused by ongoing pressures within the UK grocery retail sector. Within Service Graphics the group won new clients during the year such as the MOD, Moorfields Eye Hospital and Rolls Royce. Within SIMS they have delivered significant growth due to new client wins including Adidas and Pernod Ricard, as well as securing organic growth from the existing client base.

Despite a difficult year due to increased competitive pressures within the grocery retail market, Tactical Solutions has also had a number of new business wins over the year, including Revlon and Quorn. They continue to invest in new data and technology capabilities and have recently launched a bespoke data tool, TSeye, to continue to differentiate the business in a crowded market place. They have also developed the creative marketing and design offering. The Shop, which sits in the SP operation, has extended their European remit with international client engagements such as Adidas. In addition, since the end of the year they have re-signed and extended contracts with many of their leading clients. These contract extensions provide an increased level of visibility and a stable foundation for market share growth over the next two to three years.

The “underlying” result in the Books segment was £8.1M, a fall of £303K when compared to 2014. Revenue in Clays was broadly in line with the prior year with a slight decrease in margins. The business is the market leader in UK trade monochrome book production services and continues to extend its range of value added services to the publishing market through digital and supply chain related investment which has included the introduction of a new self-publishing service that is seeing rapid volume growth.

Sentiment in the physical book market has improved with e-reader penetration appearing to have levelled off within the UK and the US and with physical book volumes stable for the first time in a number of years. During the year the group reached an agreement with Penguin Random House to provide all of their UK monochrome book production under a new multi-year contract. This represents a significant market share gain for the business and, along with a number of other recent contract wins and extensions, secures about 80% of Clays’ workload for the next three to six years.

During the year the group acquired Solstice, a mobile first marketing and technology business for a total consideration of £28.1M comprising £19M in cash, £4.7M in shares and £5.1M in future consideration. The acquisition generated goodwill of £12.8M with further intangible assets of about £11.7M. During the period Solstice contributed £1.6M to operating profit which seems decent enough. The acquisition of Solstice in March broadened the group’s digital capabilities and enhanced their international credentials. The businesses’ offering of mobile product design and engineering services compliments existing digital businesses and creates opportunities for increased collaboration at an international level.

As mentioned, there are a huge number of “non-underling” items that affect the group so let’s have a look at some of them. The restructuring items during the year relate to the closure of the Burnley site of £1.3M, redundancy costs of £764K relating to the restructuring of the former Print Services division to the Marketing Activation segment and costs relating to empty properties of £671K. Profit on disposal of property, plant and equipment includes £411K relating to the sale of a property recorded in the Books segment, and a net gain of £159K from the sales of properties in Blackburn, Leeds and Plymouth. A loss of £29K on disposal of assets related to the closure of the Burnley site was recorded in the Marketing Activation segment. Whether these are really non-underlying or whether they are normal costs in a constantly evolving business is open to debate.

Charges related to the amortisation of acquired customer relationships, proprietary techniques, trademarks and software intangibles of £7.8M were incurred. Contingent consideration of £6.2M in respect of acquisitions required to be treated as remuneration rather than consideration and deferred consideration of £2.5M are both recorded in the Strategic Marketing segment. For a company such as St. Ives where the business strategy is very much to acquire growth, these acquisition costs definitely need to be included in my view.

An impairment charge of £1.5M relates to an impairment of goodwill of £296K and to customer relationships of £1.2M where there has been a higher level of customer churn in the Field Marketing business. An impairment charge of £1.5M was recorded on the disposal of the group’s investment in Easypress for a nominal amount in July. The same argument really applies to this as to the acquisition costs but these impairments are certainly more “one-off” in nature. The group conducted a project to offer those members of the defined benefits pension scheme over the age of 55 independent advice on their pension options. These costs of £268K have been treated as a non-underlying item. This last cost is definitely non-underlying in my view so I have finally found one!

One real potential problem has become the pension scheme. The group will continue to make deficit funding contributions of £2M per annum and a contribution of £400K towards the cost of the admin. The deficit has increased from £9.8M to £27.6M during the year caused by an increase in scheme liabilities due to a fall in the discount rate used to value the liabilities and an increase in the inflation rate.

After the period end the acquisition spree continued with an acquisition of FSP ltd, a UK based retail consultancy which will work closely with the Pragma Consulting business particularly in the airport, travel and commercial space sectors. The group have suggested they are going to continue with the acquisitions which of course they need to do as there seems to be no organic growth here.

The outlook for the Marketing Activation business remains challenging, impacted by the competitive trading conditions in the UK grocery retail sector, which are expected to continue this year. The new year has started in line with the board’s expectations and they continue to invest in their higher margin strategic marketing activities. Assuming current market conditions continue, they are confident that they will make further progress in the year ahead.

At the current share price the shares trade on a PE of 44.9 but the “underlying” PE is 9.6 which falls to 9.4 on next year’s consensus forecast so I can’t work out how to value this share – my gut feeling is that it is being over-valued when relying on underlying figures. After a 9% increase in the full year dividend, the shares currently yield 4.1% which increases to 4.2% on next year’s forecast which looks good but when so much is spent on acquisitions, can they really afford it? The net debt seems quite high here and at £62.8M it was considerably higher than the £42.7M at the end of last year but there are unutilised commitments of £35.8.

Overall then, this is a very difficult company to value. Profits are down year on year mainly as a result of an increase in deferred consideration and the impairment of the for sale assets but it’s hard to say what the underlying profit actually is. The balance sheet looks pretty terrible, net tangible assets are very negative and getting worse due to large increases in the pension deficit and bank loans. The cash flow sheet is interesting, operating cash flow did improve and if we discount the acquisitions, there is some free cash flow here although there is an outflow before financing due to the constant acquisitions.

Strategic Marketing seems to be going well but profits in the other divisions are falling, partly as a result of the competitive UK grocery market. Sentiment does seem to be improving in the books division and there is good earnings visibility there at least. The headline PE is predicted to be 9.4 next year but this is pretty meaningless as it is no doubt based on whatever form of underlying profit the analyst sees fit. The yield of 4.2% is not bad though. In conclusion then I am staying clear of this company for the moment – there doesn’t seem to be any organic growth and the constant barrage of acquisitions is taking its toll on the debt levels and balance sheet. I would much rather they took a rest, and had a couple of years where they used their strong operating cash flow to repair the balance sheet but I don’t think that is going to happen.

There does not seem to be much of a strong trend here.

On the 17th December the group released a trading update covering the first four months of the year. Trading overall was in line with management expectations with revenue running approximately 4% ahead of the same period last year and the full year expectations remaining unchanged.

Trading across the Strategic Marketing segment was strong and significantly ahead of the equivalent period last year, with organic growth of 15% driven by a combination of international expansion and greater collaboration across the group businesses, combined with acquisition driven growth of 20%. The segment continues to extend its range of services, primarily through acquisition. The integration of the recently acquired Solstice Consulting and FSP is progressing well and as planned, the group is continuing their investment in additional headcount to support growth.

Trading conditions in the Marketing Activation segment continue to be challenging due to the ongoing pressures within the grocery retail market. As a result, revenue in the sector was 10% lower than last year with flat margins as new business wins, cost reductions and efficiency improvements helped mitigate this pressure. Diversification of the client base to reduce the dependency on the grocery sector remains a priority.

Within the books business, revenue was 3% behind last year as trading in November dropped below expected levels, although they have yet to see the full impact of the Christmas trading period. The board expect to experience significant incremental volume in the business from January as part of the additional market share secured through the Penguin Random House contract win.

Despite quite liking this company operationally, I have decided that due to the weak balance sheet and heavily negative tangible book value, that I will no longer be covering these shares unless something changes on this front.