Braemar have now released their results for the year ending 2013.

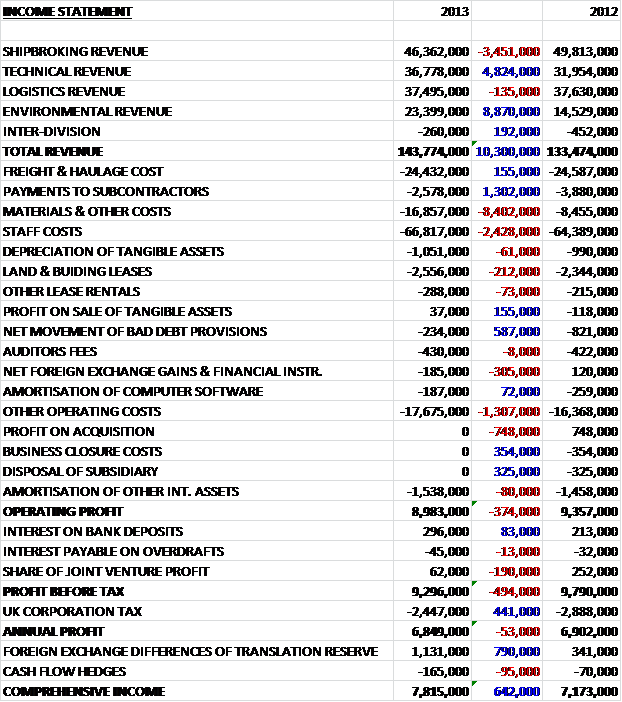

Although total revenue is up by £10.3M, the high margin Shipbroking Revenue is down by £3.5M to £46.4M. Environmental Revenue, of which the vast majority is work on the stricken containership Rena, was up nearly £9M but this revenue stream is forecast to come to an end shortly. Perhaps more pleasing is the £4.9M increase in Technical Revenue. The largest increase in costs comes from materials and other costs, which were up £8.4M to £16.9M. We have also seen a £2.4M rise in staff costs, which have helped to cause the operating profit to fall by £374K when compared to last year, at just under £9M. As a cash rich company, this was boosted somewhat by a £300K interest on bank deposits but the share of joint venture profit collapsed to £62K. This, along with a lower amount paid in tax left the annual profit just £95K lower at £6.9M. A positive foreign exchange difference pushed the comprehensive income £642K up to £7.8M.

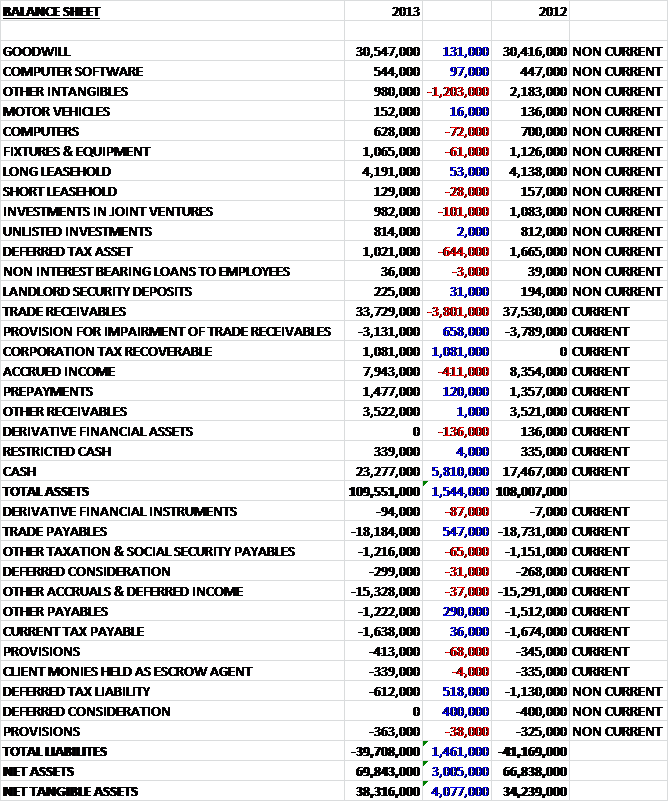

Within the £1.5M increase in total assets, the major changes are a £5.8M increase in cash, counteracted by a £3.8M reduction in trade receivables and a £1.2M reduction in other intangible assets due to them being somewhat impaired from the lower than expected performance of the acquired Casbarian Inc. Within those reduced trade receivables were £3.1M that were impaired. This was lower than last year but still seems like a lot to me. As far as liabilities were concerned, there was a £550K reduction in trade payables and a £400K reduction in deferred consideration relating to the acquisition of Casbarian where the performance targets are not going to be met within a total £1.5M reduction in liabilities. This caused the net tangible assets to increase by £4.1M to £38.3M.

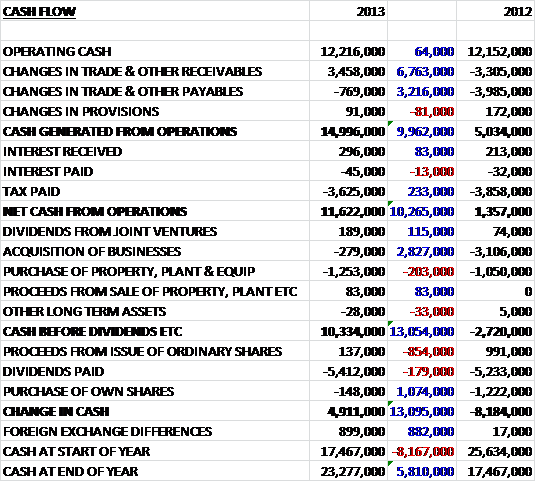

The group achieved a flat operating cash flow compared to last year at £12.2M, but a much better control of capital – especially the reduction in receivables that meant the cash generated from operations was nearly £10M better than last year at almost £15M. A reduction in tax and an increase in interest meant that net cash from operations was £10.3M better off at £11.6M. A much lower amount spent on acquisitions and a slight increase in the amount paid out in cash meant that the group achieved a £4.9M cash inflow as opposed to a £8.2M cash outflow last year. A much better performance which was driven by a better control of receivables and payables.

Although on the decline, the group still gains most of its profit from shipbroking. In 2013, that accounted for £4.6M of profit, Technical for £2.8M, Environmental £2.7M and Logistics £1.9M. Given the fact that Ship Broking still does not seem to have bottomed out and environmental will all but disappear once the Rena clean-up is completed, this is a little concerning. No customer accounted for more than 10% of group revenues, however, so the client base seems quite diverse.

During the year there was quite a bit of board upheaval and Quentin Soanes & Alan Marsh, both founding members of the company retired during the year. The finance director, James Kidwell replaced Alan as CEO and Martin Beer has arrived as the new Finance Director from Unigate.

During the year the Shipbroking division achieved more transactions than last year but the value of each transaction was significantly lower due to lower ship values, freight rates and less orders coming from the forward order book. The technical division increased revenues across most areas but in particular Offshore in Asia did well. In Logistics, ship agency revenues grew but these were counteracted by a lower project forwarding activity. Of the £23.4M of revenue recorded by the Environmental division, £18.9M was relating to the Rena project so it can be seen what an affect the end of that project will have on revenues.

The Shipbroking division has continued to struggle due to the on-going over capacity of marine tonnage which is showing no real signs of reversing and this year the deliveries of new ships continued to be higher than the scrapping of old tonnage, further increasing the over supply problems. After a fall this year, the future order book going into next year has fallen by a further £8M to just £11M but the group is seeing vastly increased business in the spot market. In the bulk shipping market, seaborne trade increased by 4.4% year on year but available tonnage increased by 10%, which shows the problem. Next year the fleet is expected to increase by 8% so the situation is likely to get worse.

The freight market for Crude tankers is at its lowest point and the product tanker market is roughly at break-even levels. The situation is such that many owners are not able to cover expenses for the year. The pattern of trade is changing as the US increasingly moves towards energy self-sufficiency and more oil and petroleum products are being consumed in Asia. The majority of business is happening on the spot market. The Chemical and gas markets look a little better, although they are affected by the same issues as other markets. The group has recently arranged a 15 year coverage for a number of gas carriers to carry Ethane from the Shale gas developments in the US to Europe.

In contrast to other markets, the demand for offshore supply vessels has been strong and the group have extended their coverage to Latin America, Asia and East Africa. The performance of the offshore desks has been good and this performance is expected to continue in the future. As with other markets, the Container market is currently oversupplied to a tune of 36% and charter rates have fallen year on year. This is not likely to improve over the next year.

The ordering of new vessels during the year was thin and due to the already over supplied market, the number of transactions has been limited. The second hand market for bulkers and tankers was even worse with prices continuing to fall and the availability of finance low but the group managed to increase transactions during the year, at a cost of lower values. Unsurprisingly the demolition of old tonnage is growing and during the year the group sent 80% more ships to demolition compared to last year.

In contrast to the Ship Broking segment, the lower margin Technical Division did rather well during the year, growing sales by 15%. A portion of this was from the acquisition of Braemar Casbarian but the majority of the growth was from Braemar Offshore where the group won a number of contracts to provide marine warranty surveys for long term offshore energy contracts in the Asia Pacific region and the group opened a new offshore office in Thailand. The market is expected to be buoyant going forward.

The adjusting business had a year of transition and further expansion occurred when an office was opened in Dubai whilst non-core operations in Latin America were sold. Despite this, performance was stable during the year. Braemar SA, who provide damage surveys, loss prevention and marine consultancy, increased revenues by 8% due to the acquisitions last year taking full effect but like for like sales were actually down on 2012. In the Engineering sector, the group won a new contract in LNG that will add a lot of revenue and the increasing demand for LNG means the group expect this sector to do well in future.

Braemar Casbarian, acquired in 2011 provides services to the offshore industry in the Gulf of Mexico. The work in this area was below expectations, partly as a result of the slow pace of recovery following the Deepwater Horizon accident. The cost base of the business has been reduced to take this into account.

Within the flat revenues in Logistics, the Ship Agency business performed well and a large contact was won for agency work at Grangemouth and Finnart. The group has grown staff numbers to support this new business. Logistics did not perform so well when compared to last year due to a number of one-off contracts that occurred last year and the negative affect the Olympics had on the business. Things have started off fairly well in the first few months of the next reporting period. During the year the group broadened their geographical reach into Houston and Oslo.

Going forward, there is no real prospect of an up-turn in the shipping markets in the short term and the recent subdued performance in Ship Broking is likely to continue, growth is expected in the Technical market, however but as already stated the end of the Rena contract will result in much lower activity levels in the Environmental sector.

The dividend remained unchanged for the year and the yield at the current share price is a stonking 6.2%. It has to be said that this yield is only covered 1.2 times by earnings but the large cash reserves mean that is it not particularly under threat. The recent rally in the share price means that the P/E ratio is no longer ridiculously cheap, at 13.1 but if the brokers are to be believed an increase in EPS next year would give a predicted P/E of 11 at the current share price, which is starting to look good value. I am not sure where the analysts expect the extra profit to come from though.

So, this year was a fairly good performance in my view, given the underlying market situation but the excellent cash flow was only really achieved by reigning in the outstanding receivables. Going forward, we know that profit from Environmental will definitely be lower as the Rena work comes to an end and the Ship Broking profit is also likely to be lower given the continued over supply of capacity. The outlook is somewhat better for the Technical and Logistics sector but I don’t really see that they will make up the short fall. Having said that, I think the dividend is fairly safe and the group continues to be debt free. I see these as a hold.

On 19th June, Braemar released an interim statement. They informed the market that performance of the chartering desks have been strong and while there was some recovery in freight rates, this is not expected to be sustained. The offshore desk and demolotion desk also performed strongly. The Technical division made a good start to the year, mainly driven by Braemar Offshore which experienced a good level of activity in the Asian energy market. The adjustment segment performed well and Braemar Engineering started work on the three month contract to design and supervise the build of 6 new LNG carriers. The Logistics segment had a solid start in a difficult market and the Environment division performed steadily, not withstanding the end of the Rena contract. In summary, the group seems to have made a good start to the year but there is no change in the outlook for the year ahead.