Tangent Communications has now released its interim results for the year ending 2016.

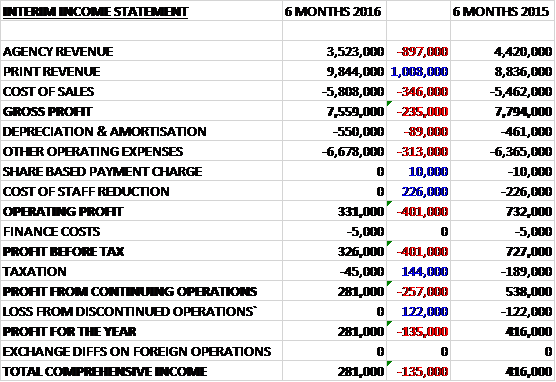

Revenues increased when compared to the first half of last year as an £897K decline in agency revenue was more than offset by a £1M growth in print revenue. Cost of sales also increased, however, to give a gross profit some £235K down. Depreciation and amortisation increased by £89K and other operating expenses increased by £313K but the lack of the £226K charge for staff redundancies that occurred last time offset this somewhat so that after a £144K reduction in tax and the elimination of the £122K loss from discontinued operations, the profit for the six months came in at £281K, a fall of £135K year on year.

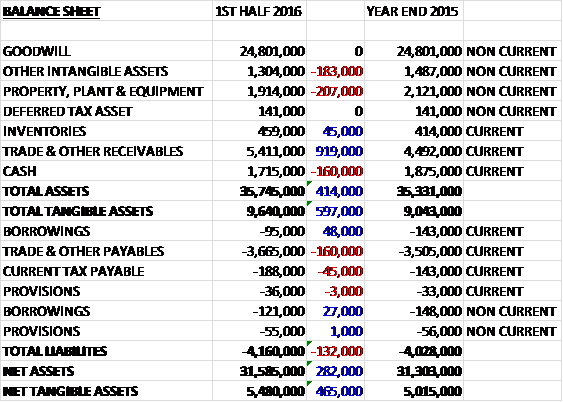

When compared to the end point of last year, total assets increased by £414K driven by a £919K growth in receivables partially offset by a £207K fall in property, plant and equipment along with a £183K decline in intangible assets. Total liabilities also increased during the period as a £160K growth in payables was only partially offset by a £75K fall in borrowings. The end result is a net tangible asset level of £5.5M, an increase of £465K over the past six months.

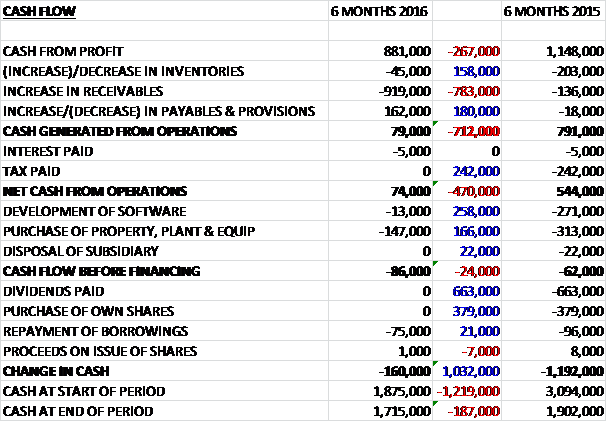

Before movements in working capital, cash profits fell by £267K to £881K. A large increase in receivables due to a spike in revenues in July and a subsequent poor cash collection period (which has now returned to normal), partially offset by no tax being paid, gave a net cash from operations of just £74K, a decline of £470K year on year. The group then spent £147K on property, plant and equipment relating to £68K spent on additions to plant, equipment and computers and a further £27K on improvements to leasehold property, and £52K spent on fixtures and fittings along with £13K on software development so that before financing there was an £86K cash outflow. There was then a £75K repayment of borrowings to give a cash outflow of £160K for the first half of the year and a cash level of £1.7M at the period-end. The group expect to be cash generative in the second half of the year.

The operating profit at the Agency business was £457K, a growth of £263K year on year on sales that were flat. The group downsized Tangent Snowball in Q2 in response to the poor new business pipeline mentioned in the last update. This pipeline has not yet improved but sales to existing clients have been better than expected so the business remained on budget during the first half of the year. The success of some of their contracts represents an opportunity to build upon, although the second half of the year remains more challenging.

The operating profit at the Print business was £47K, a collapse of £951K when compared to the first half of last year on sales that were up 1%. Sales through the printed.com website increased by 17% due to the integration of Goodprint customers and products which was completed and business cards are now the biggest selling product in this division. There has also been an increase in sales of products that are manufactured externally which enables the group to compete with new entrants to the market.

Previously printed.com had manufactured all its products in-house but they have begun to build partnerships with third party printers allowing them to expand into areas of the market in which they had not previously competed. As a consequence, they have felt some pressure on operating margin which they expect to impact performance in the second half of the year. There is growth in online print purchasing but there is similarly a growing numbers of online suppliers of print and pricing is becoming ever more visible which leads to competition increases.

Ravensworth services had a difficult period. After a strong period for residential property transactions in 2013 and early 2014, the market slowed markedly. These muted market conditions have persisted through the first half of this year and continue into the second half. There has also been a slower than expected take up of data, digital marketing and photo products which the business aims to upsell to their customer base alongside their print and design offer. T/OD performance has been comparable to the prior year. Advertising agencies continue to outsource their print production projects, providing a niche market that the business is well located to serve.

Ominously the group mentions a full review of their intangible assets at the year-end so I think it likely that we might see some impairments after that. I have noticed that the group sells goods and services to Nails Inc, a company that Michael Green has an interest in. During the period they sold £109K to them and there was £165K owed to Tangent from Nails Inc. These figures aren’t huge but it seems to me that Nail Inc. are a bit late on their payments which is perhaps something to keep an eye on?

At the end of the half the group had a net cash position of £1.5M compared to £1.6M at the end point of last year. Overall the board expect to end the year in line with its current expectations.

Overall then, this has been a fairly difficult period for the group. Profits were down, as was operating cash flow with no free cash generated. The net assets did improve, however, and they seem to have a pretty strong balance sheet. The performance in the Agency business was a bit better than I was expecting, it seems due to sales of existing customers, but they really need to start generating some new business. The print division really suffered during the period, however, it seems mainly due to increasing competition in the online print space and the poor performance of the estate agency business due to low property transactions.

So, this is an interesting one. The print business seems to be pretty doomed as it is in the commodity side of things with huge amounts of cheap competition but there is obviously something worthwhile at the agency side of things with current clients using the company more often – if (and this is a big “if”), they can win some new substantial business, improve the estate agency offering and perhaps get rid of the print business, the strong asset backing and net cash should be enough to see them through to profitable growth. I am not rushing to own the shares, but perhaps one to watch in my view?

On the 23rd December the group announced that non-executive director David Steyn resigned from his role. He has recently been appointed CEO and Chairman of Robeco Group so this is fair enough.

On the 10th February the group announced that an entity owned by Chairman Michael Green was making a bid for the company. Under the terms of the offer, shareholders are being offered 2.25p per share which represents a 63.6% premium on yesterday’s closing price and value the company at £6.7M. He has received irrevocable commitments from shareholders representing 55.5% of the total share capital.

I suppose this makes sense given the size of the company but I am sure some long-term shareholders will be very unhappy at this opportunistic bid by the management team here given their destruction of value of the past couple of years.