RM has now released their final results for the year ended 2017.

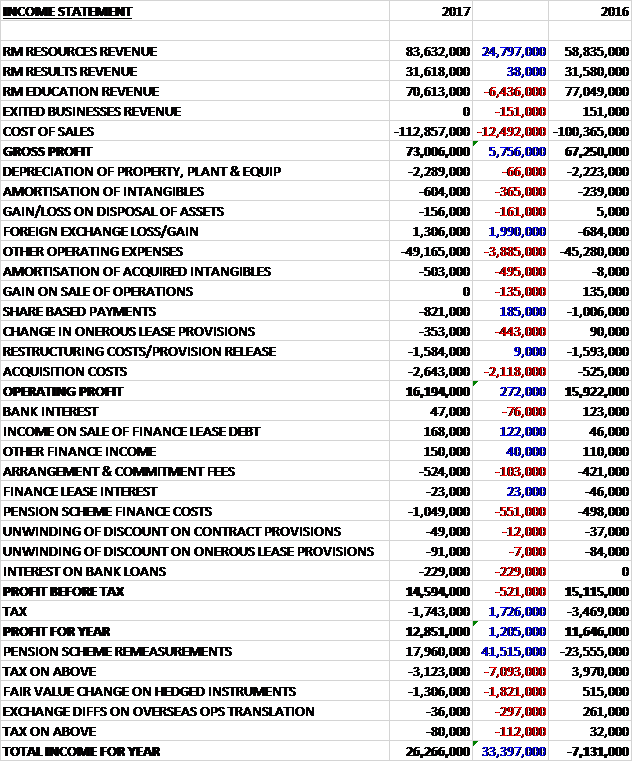

Revenues increased when compared to last year as a £6.4M decrease in RM Education revenue was more than offset by a £24.8M growth in RM Resources revenue. Cost of sales also increased to give a gross profit £5.8M higher. There was a £2M positive movement to a forex gain but amortisation was up £365K and other operating expenses increased by £3.9M. We also see a £495K increase in the amortisation of acquired intangibles, a £443K increase in onerous lease provisions and a £2.1M increase in acquisition costs which meant that the operating profit was just £272K higher. We then see a £551K increase in pension finance costs and a £229K growth in loan interest so after the tax charge fell by £1.7M (due to adjustments in respect of prior years) the profit for the year came in at £12.9M, a growth of £1.2M year on year.

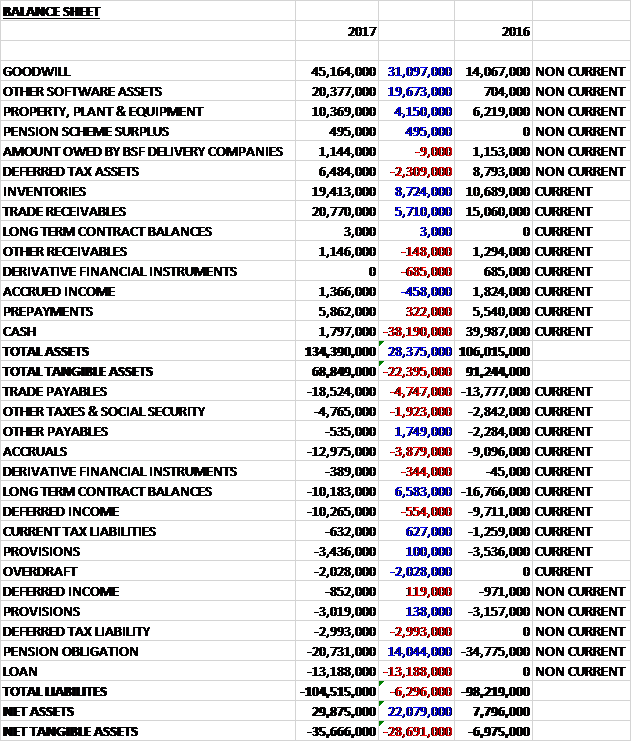

When compared to the end point of last year total assets increased by £28.4M, driven by a £31.1M growth in goodwill, a £19.7M increase in software assets, an £8.7M increase in inventories, a £5.7M growth in trade receivables and a £4.2M increase in property, plant and equipment, partially offset by a £38.2M decrease in cash and a £2.3M fall in deferred tax assets. Total liabilities also increased during the year as a £14M decrease in pension obligations and a £6.6M fall in long term contract balances were more than offset by a £13.2M new loan, a £4.7M increase in trade payables, a £3.9M growth in accruals, a £3M increase in deferred tax liabilities and a £2M overdraft. The end result was a net tangible asset level of -£35.7M, a deterioration of £28.7M year on year.

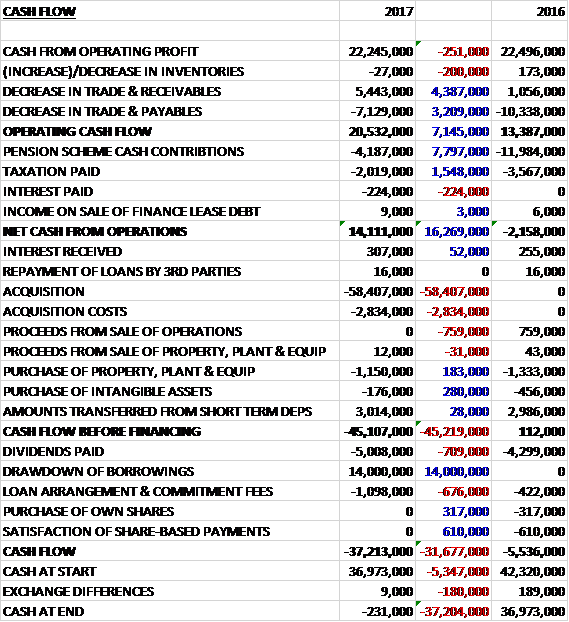

Before movements in working capital, cash profits declined by £251K to £22.2M. There was a cash outflow from working capital, but this was less than last year and after pension contributions declined by £7.8M and the tax payment was down £1.5M the net cash from operations was £14.1M, a positive movement of £16.3M year on year. The group spent £1.3M on capex and £61.2M on acquisitions to give a cash outflow of £45.1M before financing. They spent a further £5M on dividends and took out a £14M loan to give a cash outflow of £37.2M and a cash level of -£231K at the year-end.

The operating profit in the RM Resources business was £11.6M, a growth of £1.4M year on year which is attributable to the acquisition of The Consortium. Excluding the acquisition, organic revenues declined by 5% as a 23% growth in international revenue was offset by a 12% decline in UK revenue. The operating profit was further affected by a more competitive pricing market and exchange rate impacts which accounted for a £900K decline.

The reduction in UK revenues is a result of primary schools and nurseries focusing their resources budgets more on commodity items due to discretionary budgets being negatively impacted by unfunded increases in staff pension and NI costs. The decline was more pronounced in the first half before recovering somewhat in the second half, reflecting some improvement in the market, but the group expect that tight budgets will keep the UK market subdued. They continue to invest in online channels with online orders now making up around half of UK direct education sales.

The increase in international sales was driven by growth of the group’s own designed products to overseas resellers and international schools. They expect international revenues to continue to grow in the coming year with the increased product range following the acquisition significantly adding to the combined proposition going forward.

The integration of the acquisitions is progressing well. Better synergies coupled with more scope for operational efficiencies are now expected to realise benefits of around double the initial expectations of £2M per annum. The board is not expecting a significant uplift from revenue synergies due to the subdued nature of the UK market and the increased risks of new online entrants but combined purchasing contracts, the inclusion of own designed products into the Consortium’s sales channels and a joint approach to maximising the opportunity in English curriculum international schools are three of the initiatives being worked on.

The operating profit in the RM Results business was £7.8M, an increase of £963K compared to last year. Revenues remained flat, however as the e-assessment part of the business grew by 7%, offsetting the planned exit of a number of contracts in the data business (-21%). The business signed a five year agreement for the provision of a global assessment platform to Oxford University Press. The contract provides item and test authoring, online test delivery and online marking of a range of OUP English language testing products through an integrated technology platform.

The division has also secured several key contract renewals and extensions with existing customers such as a three year contract extension to continue to provide e-marking services until 2021 to the education charity, AQA; a two year extension with the Department of Education for the National Pupil database contract; and an extended e-marking contract with the Caribbean Examinations Council.

The business is targeting the growth opportunities in e-assessment whilst maintaining operating markets, and it is well placed to respond to the increasing digitisation of high stakes exams in the UK and internationally.

The operating profit in the RM Education business was £6.6M, a growth of £732K compared to 2016. Revenues declined by 8%, however, with the planned contract completion of several Building Schools for the Future contracts and the decline of some of the lower margin legacy infrastructure business. The profit figures benefited from a 12% reduction in the cost base. Managed services revenues decreased by 15% with several large BSF contracts coming to an end. Retention rates of existing customers during the year was 94% and, in addition, 49 new schools signed managed services contracts in the year.

Digital platforms revenues increased by 5% and the division signed a new contract for five years with Education Scotland to continue to provide RM Unify to all schools in Scotland. Infrastructure revenues decreased by 5% as the division continues to move away from lower margin transactional business. A significant new three year contract was won to provide technology services to over 500 schools in Hertfordshire.

In June the group acquired The Consortium, a supplier of own-branded products to educational institutions, for a cash consideration of £59M. The acquisition generated goodwill of £31.1M and in the five months of ownership, the business made a profit of £800K. Had it been part of the group for the whole year, it would have contributed £1.2M.

During the year an onerous provision was created for the top floor of the head office property and an onerous provision release was made for the continued sub0letting of a property, the result of which was a charge of £353K. The group also incurred professional advisor costs relating to the acquisition and integration of The Consortium (£2.6M) with further restructuring costs of £1.6M.

Going forward, despite the continued subdued UK education market, the year has started in line with expectations and the board are confident of a year of good progress

At the current share price the shares are trading on a PE ratio of 14.4 which falls to 9.7 on next year’s consensus forecast. After a 10% increase in the full year dividend the shares are yielding 2.9% which increases to 3.4% on next year’s forecast. At the year-end the group had a net debt position of £13.4M compared to a net cash position of £40M at the end of last year.

On the 21st March the group released a trading update covering Q1. Trading was in line with expectations. In March, RM Results signed a 32 month contract with Singapore Examination and Assessment Board to deliver their new integrated Digitisation of Scripts and Electronic Marking system with the option to provide an additional four years of support and maintenance. Net debt as of the end of February was £26.1M, above the £13.4M reported at the year-end.

Overall then this has been a bit of a mixed performance for the group. Profits increased as a reduction in tax charges offset an increase in acquisition costs. Net tangible assets deteriorated further and is now fairly heavily negative. The operating cash flow improved but this was due to favourable working capital movements and cash profits declined.

RM resources saw profits increase due to the acquisition, organic profits declined due to continued pressure on UK school budgets, forex movements and more competitive pricing. RM Results saw profits rise due to improved margins and RM Education saw a growth in profits due to a lower cost base. In none of the divisions did organic revenues grow. The acquisition seems to be bedding in well and the forward PE of 9.7 and yield of 3.4% make the shares look decent value but the lack of growth and continued pressure on UK school budgets is making me think about taking profits here.