Gem Diamonds has now released its final results for the year ended 2015.

Revenues declined by $21.4M when compared to last year due to a reduction in volumes sold and the average diamond price achieved at Letseng. With cost of sales falling to a lesser degree, the gross profit decreased by $1.5M. Royalty and Selling costs fell by $2.8M, however, and corporate expenses declined by $687K. We also see an $8.1M reversal of accrued tax expenses that did not occur last time, a $1.4M foreign exchange gain and a $1.5M forex gain on the tax settlement which meant that the operating profit increased by $13.3M when compared to 2014. The bank deposit income fell by $1.5M and other financial income was down $448K but this was partially offset by a $1.7M decline on the interest payable on loans before a $3.1M positive swing to profit from the discontinued operation and a $3.5M decline in tax charges meant that the profit for the year came in at $77.7M, a growth of $19.7M year on year, although it is worth noting that Ghaghoo has bypassed the income statement.

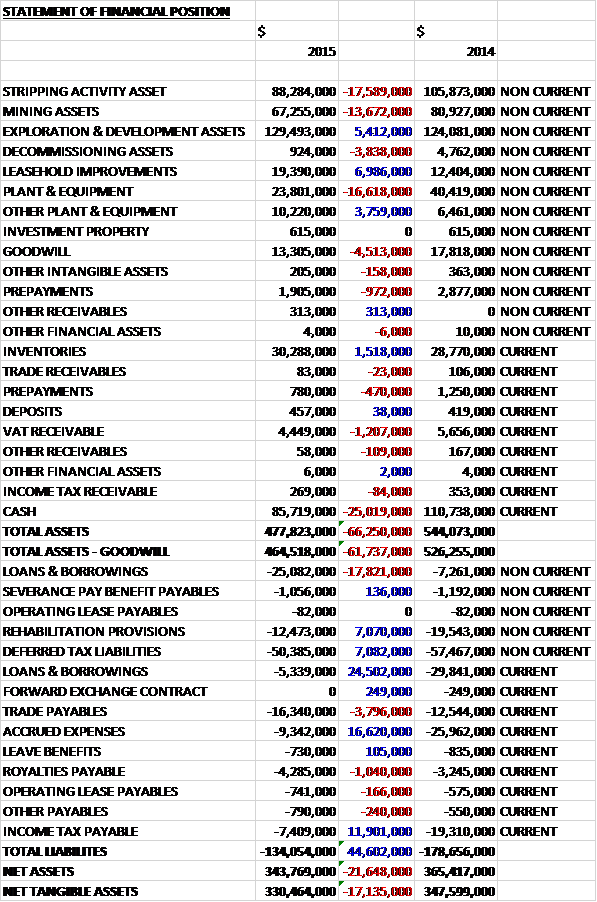

When compared to the end point of last year, total assets declined by $66.3M, driven by a $25M fall in cash, a $17.6M decrease in the stripping activity asset due to forex differences, a $16.6M fall in plant & equipment (also forex related), a $13.7M decline in the value of mining assets (forex again!) and a $4.5M decrease in goodwill, partially offset by a $7M growth in leasehold improvements and a $5.4M increase in exploration assets. Total liabilities also declined during the period as a $6.7M fall in borrowings, a $16.6M decline in accrued expenses, a $7.1M decrease in deferred tax liabilities and a $7.1M fall in provisions as a result the annual assessment of the estimated closure costs relating to the weakening of local currencies, and changes in the discount rate (about half attributable to each effect) was partially offset by a $3.8M growth in trade receivables. The end result is a net tangible asset level of $330.5M, a decline of $17.1M year on year.

Before movements in working capital, cash profits increased by $1.7M to $155.3M. There was a cash outflow through working capital, however, with a growth in inventories reflecting the timing of production cut-off for tender purposes, and an increase in receivables which meant that before tax and interest, the cash from operations fell by $2.1M. There was a big growth in tax payments, with an $11.8M increase, to give a net cash from operations of $119.1M, a decline of $14.6M year on year. The group then spent $48.6M on property, plant & equipment along with $61.4M on waste costs to give a free cash flow of $9.5M. This all went on dividends to non-controlling interests with a further $4.4M of financial liabilities paid back and $6.9M in dividends to shareholders to give a cash outflow of $13.6M for the year and a cash level of $85.7M at the year-end.

Revenues this year exclude any contribution from Ghaghoo on the basis that the mine had not reach full commercial production by the end of the year, although the mine did generate sales of $14.4M. Net of this income, Ghaghoo operating expenses were $15.8M during the year, capitalised to the carrying value of the asset during the year.

The year was characterised by continuing global macro-economic volatility and the sentiment in the diamond market as a whole remained cautious. These conditions, together with continued liquidity constraints and high levels of stock, plagued the diamond market throughout the year, placing downward pressure on both rough and polished diamond prices with diamond indices showing a decrease in the average diamond prices across all diamond producers in excess of 19%.

Letseng’s high value diamond prices remained resilient, increasing by 3% compared to the reserve price estimates set out at the start of the year. During the year the price per carat achieved for the Ghaghoo production decreased from $210 per carat in February to $150 per carat in December.

The significant drivers of the diamond market during the year included the continuing economic recovery in the US which had a positive impact on diamond sales in the country during the year but on the flip side, this resulted in a stronger US dollar which, due to diamond sales being US dollar denominated, had a negative impact on sales in countries whose currency was negatively impacted by the strengthening dollar. Other factors were weakening demand from China as economic growth there slowed; funding constraints due to the closure of the Antwerp Diamond bank at the end of 2014 and tightening of lending criteria, particularly in India; and high levels of polished inventory in the manufacturing sector towards the end of 2015 following the reduced demand from China.

At Letseng, 108,579 carats were recovered compared to 108,569 in 2014 and ore treated increased from 6.4M tonnes to 6.7M tonnes. This increase in ore treated, particularly in the second half of the year, reflects the benefits of the Plant 2 Phase 1 upgrade project implemented at the beginning of the year. Of the total ore treated, 71% was sourced from the main pipe and 29% from the satellite pipe, which is a similar split to last year. Waste tonnes mined increased by 21% in line with the optimised LoM plan which allows for increased levels of higher grade ore from the higher value satellite pipe to be mined. The average price per carat declined from $2,540 last year to $2,299 in 2015.

A new optimised life of mine plan was published in May. The plan makes provision for increased levels of higher grade ore from the satellite pipe to be mined annually. In accordance with this plan, satellite ore production will ramp up to 2M tonnes per annum in 2020 and remain at that level to the end of the life of the mine which extends to 2038. A key feature of the plan is the use of steeper pit slope angles as significant improvements to side wall control and blasting of the pit slopes has allowed the mine to safely increase the angles. This will result in lower stripping ratios, thereby significantly reducing the total cost of mining and increasing open pit ore tonnage.

During the second half of the year, a third 300 tonne excavator and five additional 100 tonne dump trucks were acquired, equipping the mine to achieve the new waste stripping target. Furthermore, the optimised plan made provision for the increased treatment capacity of 250,000 tonnes per annum following the recent Plant 2 Phase 1 upgrade with the full benefit of the upgrade expected to be seen in 2016.

The expansion of the open pits has necessitated the relocation and construction of an expanded mining support services complex. The first phase of this project has been approved and will establish the infrastructure where daily service maintenance on the 100 tonne trucks can be carried out and will be completed by the end of Q2 2016 at a cost of less than $1M. Initial high-level studies suggest there is a case for an underground mine in both the satellite and main pipes. Further studies will be undertaken to determine the optimal timing of when underground construction needs to start.

During the year the company continued to benefit from the investments made in previous years. The introduction of optimised secondary crushers at Letseng in 2013 was an important milestone towards reducing diamond damage. In addition, a change in mine blasting practices has resulted in improved fragmentation of the ore delivered to the treatment plants which further contributed to a reduction in damage of the valuable Type II diamonds.

Reducing diamond damage remains an area of key focus at Letseng. A number of schemes are underway to reduce damage and are starting to yield results which is evident in the increase in the number of larger diamonds that were recovered during the year with 11 diamonds greater than 100 carats having been recovered which was a new record for the mine. The Plant 2 Phase 1 upgrade was completed in Q1 of the year. This project was completed at a cost of $3.5M on schedule and the expected increase in the annual plant capacity as a result of the upgrade has been realised. The new Coarse Recovery plant was finalised in Q2 at a total amount of $11M, being below the original budget. The plant is operating and has met most expectations, although some minor refinements will be introduced during Q2 2016.

Skills attraction and retention remains a principal risk at Letseng. Localisation demand, challenges in obtaining work permits for skilled ex-patriots and increasing demand for skilled personnel from other companies in Lesotho have exacerbated the risk. Extensive engagement with government officials on this matter and initiatives to mitigate the skills risk by enhancing remuneration practices and conducting development programmes for local employees are ongoing.

The focus for the mine in 2016 is to continue the ramp up of the waste stripping in line with the optimised mine plan, intensified focus on costs, enhanced efficiencies through continuous improvement programmes, construction of the first phase of the mining equipment support services complex, progress the underground mine studies, and to progress innovation work streams to further reduce diamond damage.

Letseng sources its power through the Lesotho Electricity Corp which in turn sources its power from Eskom, in South Africa. Eskom has had challenges in providing consistent power in South Africa and the neighbouring states. In light of this, improvements in power supply monitoring, and the provision of additional back-up power supplies were undertaken last year to minimise the impact of lengthy outages. During the year, Eskom’s downtime didn’t materialise to the extent expected and the mine experienced less than 88 hours of outages, of which 64 hours were countered with backup power.

The Ghaghoo mine treated 326,922 tonnes during the year and recovered 91,499 carats, achieving a recovered grade of 28cpht. The Autogenous Mill technology proved successful and recovered grades were 1% above the reserve estimate. This was further enhanced after installing a surge bin ahead of the AG mill in early 2016 to improve its performance, confirming the plant’s ability to run at its nameplate capacity of 60,000 tonnes per month. The majority of the ore treated during the year was sourced from Level 1 and a total of 1,751 metres of tunnelling was completed. During the year, 30 diamonds larger than 10.8 carats were recovered, including a 48 carat diamond, the largest diamond recovered at the mine to date. A number of fancy coloured diamonds, although predominantly in smaller sizes, were also recovered.

The mine continued to experience difficult underground conditions. At the end of November, caving at the end of tunnels two and three propagated through to the surface. Although this was expected to occur as the volume of ore extracted underground increased, it occurred some six months earlier than anticipated. Actions required to create a buffer zone to limit sand dilution have been put in place and underground mining has resumed. This will result in the deferment of extraction of about 300,000 tonnes of ore. A notable achievement this year was establishing a sustainable solution for the water fissure on Level 1 and the intersection on the ramp to level two.

Diamond prices achieved from the three sales held in 2015 were lower than the reserve estimate due to the current depressed state of the rough diamond market and the overall finer size of the recovered diamonds. Based on this fall in prices, various options were reviewed with the aim of minimising operating losses in the coming year. It was decided, that in the short term it was prudent to downsize current production to achieve a modified target of about 300,000 tonnes for 2016. Options are being assessed to expand the operation in order to achieve acceptable financial returns as and when diamond prices improve.

The focus in 2016 will be on cost optimisation and restructuring of the operation, sampling of the VK-Main phase of the orebody, the continuation of Level 2 development, and assessing options to expand the operation.

The group continued generating additional margin on selected high-value diamonds through its manufacturing facilities and partnership agreements. The diamond manufacturing operation in Antwerp contributed $3.8M to group revenues through additional polished margin generated, and $2.9M to underlying EBITDA. During the year, 336 carats valued at a rough market value of $4.6M were extracted from the Letseng exports for manufacturing. In total, polished diamonds with an initial rough value of $13.4M were sold during the year and $6.2M remained in inventory at the year-end compared to $15M at the end of last year.

In order to help determine the location, size and shapes of the basalt mega-xenoliths in both Letseng pipes, the ahead of face drilling programme continued in 2015. This assists in guiding mine planning to ensure that rafts are not blasted together with clean ore, minimising dilution and diamond damage. A total of 48 holes or 3,179 metres were drilled and the data gathered from this programme will also be used to improve the 2016 geological model. A total of 768,396 tonnes of discrete samples were collected during the year and this additional sampling information will be incorporated in the 2016 resource estimates.

Letseng’s mineral resources were re-estimated in 2015 which reflects slight changes to resources and reserves due to mining depletion and updates to orebody volumetric and estimation models and there are now 4.95M carats of resources, a decline of 1%. The Ghaghoo statement will be updated during the course of 2016.

In December the company settled an interest-bearing tax liability for an amount less than previously provided for, resulting in the reversal of accrued expenses of $8.1M. In addition, this liability was payable in Australian dollars, resulting in a foreign exchange gain of $1.5M. In June the group sold its manufacturing facility in Mauritius for an agreed price of $400K to be paid in quarterly instalments starting in October 2016 which, given the net liabilities recognised in the business, led to a gain on disposal of $1.7M.

The group is benefiting from the strength of the US dollar and a 10% further strengthening of the currency would have had the effect of increasing pre-tax income by $2.8M.

During the year the group appointed Michael Lynch-Bell as an independent non-executive director. Michael was previously a senior resources partner at Ernst & Young and is a current non-executive director at three other mining companies, including Kaz Minerals. After eight years of service as Chief Operating Officer, Alan Ashworth announced his intention to retire in June 2016.

At the year-end, the group has $16.1M of undrawn facilities representing the three-year revolving credit facility at Letseng. After the year-end, the company’s existing $20M three year unsecured revolving credit facility was refinanced for an increased amount of $35M for a further three years.

Going forward, although 2016 has seen a positive start with improved rough diamond prices being reported across the industry, significant global economic uncertainty remains. In the short term, the downward pressure on both rough and polished prices in the diamond market remains a challenge, particularly for the more commercial Ghaghoo operation. The prices achieved for Letseng’s large high value production are expected to remain resilient during a continued uncertain and difficult short term period facing the global diamond market. Next year, the Letseng mine will have the full benefit of the Coarse Recovery Plant and the Plant 2 Phase 1 upgrade should further enhance the potential at the mine.

At the current share price the shares are trading on a PE ratio of 4.3, including the exceptional income following the tax settlement. On next year’s consensus forecast, however, the shares are trading on a forward PE of 9.6 which seems pretty cheap to me. After the announcement of a special dividend, representing the cash saving arising from the settlement of a previous tax assessment, the shares are currently yielding 5.3% which falls to 3.8% on next year’s forecast.

Overall then, this has been a mixed year for the group. Profits were up but when we consider the $9.6M benefit from the tax settlement, the $3.1M swing from the sale of the Mauritius operation and the $15.8M of losses that bypassed the income statement relating to the Ghaghoo mine, the profit looks less impressive and taking all these into account, profits declined year on year. Net assets also declined but this was mainly due to the weakness of local African currencies against the dollar. The operating cash flow declined too but this was as a result of an increased tax payment and a growth in inventories and cash profits increased – although, once again, this does not include the cash sink that has been Ghaghoo and once the Lesotho government got its dividends from Letseng, there was no free cash left.

The Diamond market has been difficult during the year due to the strong US dollar, weakening Chinese demand and funding constraints to the market. This has all led to the Ghaghoo mine not achieving the prices expected of it which in turn has led to a downsizing of current production. The downturn has had less of an effect on the large diamonds produced from Letseng, however, and that mine continues to be strong.

Going forward, the increase of production from the higher grade satellite pipe at Letseng along with the full benefit from the Plant 2 upgrade and reduced diamond damage should mean that the mine prospers next year. The problem is the Ghaghoo mine which remains a drag and a cash sink. This is a difficult one but I think I am sitting tight at the moment and await further developments.

On the 19th July the group released a trading update covering the first half of the year. Letseng’s high quality large white rough diamonds have seen a modest improvement in prices during the period. Liquidity constraints, high polished inventory levels and the uncertain macro-economic outlook continue to characterise the polished diamond market. It is anticipated, however, that the modest recovery in rough prices will continue into the second half of the year.

Letseng continued to perform well with consistent prices and carat production that is tracking towards the top end of guidance. In all, 57,380 carats were recovered, an increase of 15% and the average grade achieved was 1.72cpht compared to 1.61cpht with a 7% growth in the tonnes of ore treated. The good grades achieved are reflective of the area mined in the Satellite pipe that has historically produced higher than reserve grades albeit at a slightly smaller average stone size. The Coarse Recovery XRT plant is operating at a >5mm size cut off with final materials handling improvements rolled out during June.

The average price achieved was $1,899 per carat, compared to $2,264 in the first half of last year although apparently this decline reflects the mix of diamonds recovered due to a lower-value, higher-grade area being mined. This decline was offset by a 19% increase in carats sold which meant that the total value of sales remained flat at $106.3M. Amongst the exceptional diamonds recovered, an undamaged Type II 160 carat and an 11.8 carat pink diamond, which sold for $187K per carat, were recovered. After the period-end, an exceptional quality 104 carat Type II white diamond was recovered after mining moved to a different are of the Satellite pipe. There has been a modest recovery in the mine’s rough diamond prices towards the end of the period on a like for like basis.

At Ghaghoo, development of production block 2 on level 1 was completed and development of level 2 has started. A sale in Q1 achieved an average price of $160 per carat and a sale that took place in June achieved an average price of $155 per carat due to an increase in the proportion of finer material sold due to an improvement in diamond liberation at the mill. There was a large proportion of ore treated that has been from diluted areas near the pipe extremities with lower recovered grades achieved. Grades have improved, however, as mining in the second block has moved towards the centre of the pipe.

The mine has focused on downsizing from the original production target of 2,000 tonnes per day, improving efficiencies, and progressing operational developments. The quantity of ore treated declined by 51%, the grade fell by 24% to 21.8cpht as a significant proportion of the ore treated was sourced from lower grade areas at the edge of development zones, and the quantity of carats recovered fell by 63% to 20,876.

The group had $66.4M cash on hand as of the period-end, with $53.1M attributable to Gem Diamonds. Also some $28.7M of debt facilities had been drawn down which resulted in a net cash position of $37.7M.

Clearly the market is undergoing some pressure at the moment but the modest increase in prices is promising. I note the reduction in net cash but these shares are actually starting to look a bit cheap now.

On the 10th August the group announced that extreme weather conditions have recently been experienced where the Letseng mine is located, with excessive snow falls and severe winds limiting access to the mine. Following damage to overhead power lines, standby generators installed at the mine have been used to mitigate some of the impact, allowing the plants to operate, albeit at reduced rates. The Lesotho Electric Company is currently on site carrying out repairs to damaged overhead power lines and external power supply is expected to be fully restores in the short term.

Full year guidance for ore tonnes treated and operating costs may need to be reassessed but due to the strong operational performance in the first half of the year, carats recovered are not expected to be affected materially and full year carats recovered will likely be within original guidance.