Origin Enterprises has now released its interim results for the year ending 2016.

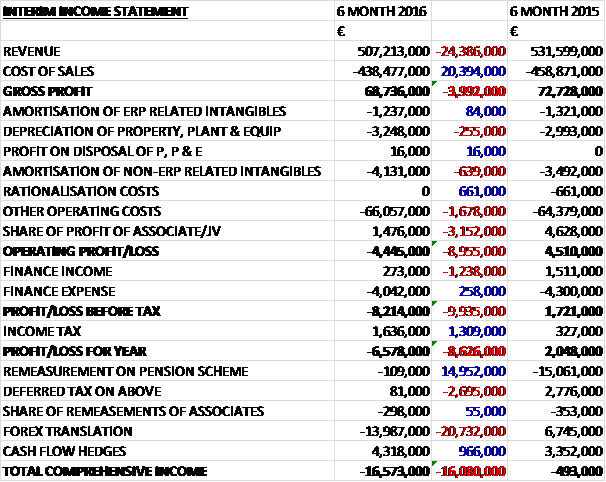

Revenues declined by €24.4M when compared to the first half of last year reflecting lower fertilizer volumes and prices, lower agronomy services and crop protection volumes and prices as well as lower crop marketing volumes and prices. Cost of sales fell by €20.4M to give a gross profit €4M below that of H1 2014. Depreciation was up €255K and non-ERP intangible amortisation increased by €639K although there were no rationalisation costs which accounted for €661K last time. Other operating costs increased by €1.7M and the share of profit from the associates reduced by €3.2M to give an operating loss of €4.4M, a detrimental movement of €9M. We then see finance income down €1.2M, offset by a finance expense that reduced by €258K and a tax charge that was €1.3M lower to give a loss for the first half of €6.6M, a detrimental movement of €8.6M year on year.

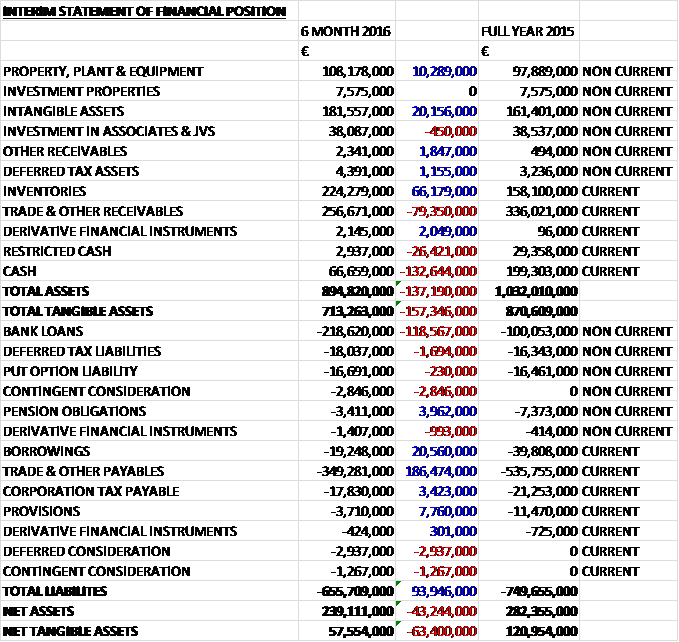

When compared to the end point of last year, total assets declined by €137.2M, driven by a €132.6M fall in cash, a €79.4M decline in receivables, and a €26.4M decrease in restricted cash, partially offset by a €66.2M growth in inventories, a €10.3M increase in property, plant & equipment relating to the acquisitions and a €20.2M increase in intangible assets, also from the acquisitions. Total liabilities also declined during the period as a €186.5M fall in payables, a €7.8M decline in provisions as €7.3M were paid during the period, a €4M fall in pension obligations as a result of the €4.5M contribution paid into the scheme, and a €3.4M decrease in corporation tax payable was partially offset by a €98M growth in borrowings, a €2.9M increase in deferred consideration and a €4.1M growth in contingent consideration. The end result is a net tangible asset level of €57.6M, a decline of €63.4M over the past six months.

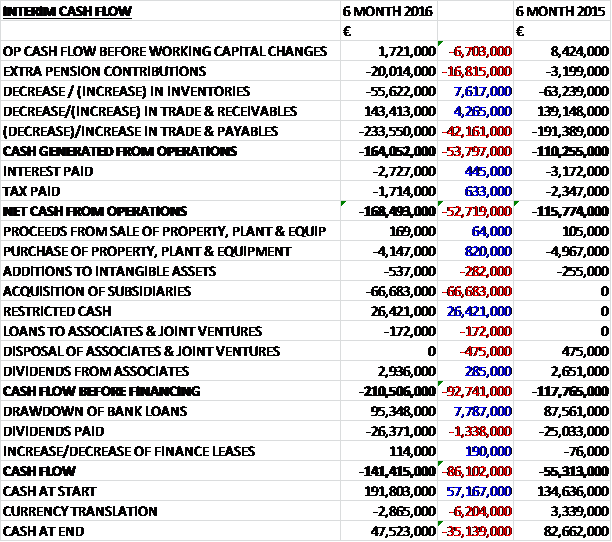

Before movements in working capital, cash profits declined by €6.7M to €1.7M. There was a big outflow of cash through working capital, reflecting seasonal requirements, with a €233.6M decrease in payables and we also see a €20M extra contribution to the pension scheme. After this and a slightly smaller interest and tax payment, the net cash outflow from operations is €168.5M, an increase of €52.7M year on year. The group also spent €4.1M on property, plant and equipment; €537K on intangible assets and €66.7M on acquisitions, of which €26.4M came from restricted cash. We also see €2.9M in dividends from associates to give a cash outflow of €210.5M before financing. The group spent €26.4M on dividends and drew down €95.3M of new bank loans to give a cash outflow of €141.4M in the six month period and a cash level of €47.5M at the period-end.

Trading for the first half of the year has been slow and challenging. Highly adverse and unseasonal weather patterns significantly limited in-field crop maintenance activity during Q2 and this, combined with weak farmer confidence reflecting the current pressures on primary producer incomes, is expected to result in a greater of concentration of demand in the second half of the year.

The loss recorded at the Agri-Services business was €1.8M compared to a profit of €4.1M in the first half of last year which was mainly attributable to lower fertilizer volumes and prices along with lower agronomy services and crop protection volumes and prices, partially offset by improved performance in the feed ingredients business. In the UK, the business recorded lower agronomy revenues and margins in the seasonally quiet first half, largely reflecting the impact of a delayed harvest and poor weather. Record rainfall across much of the UK during December and January led to widespread flooding. In-field crop maintenance and cultivation activity was significantly curtailed during Q2 due to these weather patterns which resulted in poorer ground conditions. This contrasts with excellent in-field conditions towards the end of Q1 which supported robust crop planting activity.

While it can be expected that there will be a minor level of crop damage in those areas worst affected by the flooding, conditions for crop establishment and growth were generally excellent due to above average temperatures throughout the winter period. Assuming normal weather patterns during the main growing season, the board remain positive regarding catch up agronomy revenue development in H2 as farmers address the current weather effects of higher disease levels in crops, saturated soils and nutrient deficiencies. The challenging market backdrop for primary producers, however, continue to drive greater competitive intensity across the group’s service and input portfolios as farm budgets are rigorously scrutinised for value and returns.

Poland achieved a good first half result with higher agronomy revenues and margins in the period. This performance was driven by the benefit of an extended autumn season, which in combination with the introduction of new service offers, supported solid volume development across the agronomy portfolios. Sustained high temperatures during the summer period led to a difficult maize harvest for farmers and resulted in significantly lower yields. Total autumn and winter plantings are some 2.3% lower than last year, which is in line with expectations with generally favourable weather supporting good crop development.

During the period the group combined Dalgety and Kazgood to form Agrii. Integration is progressing well across commercial, technical and business processes with the combined business now operating a single sales organisation and customer interface. The enlarged business significantly extends the group’s reach and service capability to provide value added solutions and applications that meet the requirements of an increasingly professional and technically oriented customer.

In Romania, the group completed the acquisitions of Redoxim and Comfert in September and December respectively. Business performance was satisfactory and in line with expectations during the seasonally quiet first half. Farmers adopted a cautious approach to investment spend in advance of the main season following delays in the receipt of the single farm payment and the impact of sustained drought conditions last year which significantly reduced yields for spring crops in 2015. Crop establishment over the autumn and winter period has been favourable despite the impact of unseasonably high temperatures on soil condition following the earlier drought.

Notwithstanding that current weather conditions are conducive to crop development, normal rainfall during the early growing season will become an increasingly important requirement in maximising the planted area and the potential of spring crops. Integration planning was started during the period with an initial focus on combined commercial opportunity and the establishment of a technically based agronomy communication infrastructure.

In Ukraine, Agroscope achieved an improved result in the first half supported by higher early season agronomy revenues. The business is well positioned for the rest of the season with volume growth principally reflecting an increased level of customer commitments secured ahead of the main H2 application period. Trading conditions remain extremely competitive as farmers face heightened cash flow pressures which are due mainly to significant year on year local currency weakness.

The autumn and winter crop planting programme was significantly impacted following the sustained high temperatures and drought conditions last year and about 70% of the target arable cropping area has been completed. The business continues to pursue new development opportunities through the broadening of its agronomy sales force and the regional extension of its farm services distribution footprint along with the creation of service offers that are principally dedicated to the independent farms channel.

Business to business agri-inputs had a challenging first half with lower revenues and margins reflecting slower fertilizer volume development which was partially offset by higher feed volumes. A combination of reduced farmer confidence and delayed seasonal timing due to poor weather drove weak early season fertilizer demand. Lack of certainty on near term fertilizer price development has provided customers with little incentive to buy forward during the period despite a more competitive trading backdrop. The board remain positive regarding the full year fertilizer volume outlook in Ireland with application expected to be underpinned by higher livestock numbers. While lower market volumes are anticipated in the UK for the year as a whole, they expect volume development to improve during the second half.

The amenity business performed satisfactorily during the period. The professional sports turf channel continued to drive new customer opportunity in the period with new product and service innovation underpinning improved brand awareness through the development of advanced turf management and maintenance solutions. Higher volumes and improved margins supported a good first half performance from Feed Ingredients. Volume development in the period reflected favourable spot demand and the board anticipate a stable volume outlook for the full year.

The profit from associates, which now just includes the feed ingredient business following the sale of the consumer foods business, was €1.5M, a decline of €4.8M year on year. This was a satisfactory result in the period against lower volume performance.

During the period the group completed a number of acquisitions in Romania and Poland. In September they acquired Redoxim. Based in Romania, the business is a provider of agronomy services, macro and micro inputs to arable, vegetable and horticulture growers. In November they acquired Kazgod, based in Poland. This business is a provider of agronomy services, inputs, crop marketing solutions and also manufactures micro nutrition products. In December they acquired Comfert, based in Romania. This business is a provider of agronomy services, integrated inputs and crop marketing support to arable and vegetable growers. In all, the acquisitions cost €48.8M, satisfied by €41.5M of cash consideration with the rest in deferred and contingent consideration.

Going forward, reflecting the seasonality profile of the business, for the current year the group will earn over 100% of the full year operating profits from agri-services in the second half (this is not saying much considering it made a loss in the first half!). The board are maintaining their full year adjusted EPS guidance of between 51c and 53c assuming normal weather patterns and no material adverse changes in exchange rates.

At the period-end, there was a net debt position of €171.2M compared to a net cash position of €59.4M at the end of last year and a net debt position of €161.2M at the same point of last year. After the introduction of an interim dividend, the shares are now yielding 3.5% on an annual basis.

Overall then this has been a difficult period for the group. The loss worsened, partly due to the sale of the associate; net assets declined and the operating cash outflow worsened, mainly due to a large fall in payables. Most of the issues have stemmed from the unseasonal weather, especially the flooding experienced in the UK, and weaker farmer confidence given a fall in output prices. These issues had the effect of reducing fertilizer prices and volumes, along with a reduction in demand for agronomy services and crop protection.

The results of this company are always second half weighted but this year even more so as the board expect the performance to catch up in H2 to give an unchanged performance for EPS for the year. The dividend yield of 3.5% does not fully discount the risk that adverse weather or worsening farmer confidence derail this so for now I prefer to wait for guidance as to how trading in the second half is progressing.

On the 28th April the group released a Q3 trading update. Highly adverse weather conditions, combined with a very difficult market backdrop for primary producers, has resulted in increased seasonality with the group earning all its profits in the second half of the year.

Trading for Q3 has been disappointing, with the group achieving lower revenues against the comparative period across its service platforms in Ireland, the UK and Poland. The performance principally reflects the impact of very late spring conditions on activity levels on farm due to the continuation of highly unseasonal weather patterns across Northern Europe. Following a positive start in February, March and April experienced a return to abnormally cold and wet conditions which led to a combination of increased crop losses, slower crop development and re-saturated ground conditions which have limited infield crop maintenance and spring planting activity.

The current seasonal challenges together with the impact of sustained pressures on the incomes and cash flow of primary producers will make for a highly competitive backdrop to trading in Q4 so the board believe that the full year outturn will be lower than the level previously indicated at the time of the publication of the group’s interim results. In light of the current adverse weather, it is not possible at this point to assess the level of delayed service and input application which will carry forward to Q4. Things do not seem to be improving here and I don’t see this decline as a reason to jump in to buy here.

On the 26th May the group released a trading update covering the first nine months of the year. As outlined previously, trading for Q3 was disappointing with the group achieving lower revenues across its service platforms in Ireland, the UK and Poland. The performance principally reflects the impact of very late spring conditions on activity levels on farm due to the highly unseasonal weather patterns across Northern Europe.

In Agri-Services, revenues for Q3 were 1% lower at €555.5M with a 2.7% decrease over the nine month period. This is despite acquisitions having a 15% favourable impact on the quarter’s trading which means that underlying revenues collapsed by 12.2%. Underlying year to date crop input volumes have decreased by about 8% comprising lower crop protection and fertilizer volumes partially offset by higher feed volumes.

In the UK, Agrii achieved lower revenues in Q3 due to the impact of a very late spring season. Following an unseasonably wet first half, the continuation of higher average and sustained rainfall levels across the main crop growing regions during the quarter resulted in heavily saturated soils and slower crop development. In field crop maintenance and spring planting activity were significantly curtailed as a result. This was the principal factor driving a 20% reduction in agronomy service revenue and crop protection volumes in the quarter.

The board anticipate increased agronomy demand in Q4 reflecting the more concentrated seasonality profile in the year. The missed service and input application carried forward from Q3 is unlikely to be recovered in full, however, due to the agronomic impact of the significantly later season on crop potential against the backdrop of generally weaker sentiment on farm. The business remains focused on prioritising higher value full service and influenced agronomy application through technical strategies that dilute the cost of production and maximise the economic potential of crop enterprises.

In Poland, trading conditions in Q3 were extremely challenging with like for like agronomy revenues some 25% lower. Service and input demand were reduced following prolonged frost conditions combined with an absence of snow cover across the country during March and April. This unusual weather pattern led to a loss of about 1.2M hectares of winter wheat and oil seed rape crops, equivalent to about 20% of the total winter cropping area. Given the seasonality profile and structure of cropping, missed service and input application is not expected to be recovered in Q4. A comprehensive programme of integration and change management was advanced in the period.

In Romania, the total business has performed ahead of expectations in Q3 with increased agronomy and crop input revenues. Solid momentum was achieved across the direct farm and retail customer channels supported by a combination of favourable conditions on farm and the introduction of enhanced technical support to the agronomy sales teams and product specialists. Good progress has been achieved to date in the integration of the acquired businesses with the focus on building new capability, systems and process development along with operational simplification.

In Ukraine, Agroscope achieved higher revenues in Q3 with favourable momentum across all service and input portfolios supported by new customer development through an expansion of the agronomy sales force. Highly competitive trading conditions drove margins lower, however, and largely reflect current cash flow pressures on farm with many primary producers opting for alternative, lower crop investment options.

Business to business agri inputs achieved a satisfactory performance in the quarter reflecting stable fertilizer volume performance against a lower margin sales mix together with the benefit of increased feed volumes.

Fertilizer volume development in both Ireland and the UK improved during the quarter following weak early season demand due to weather delayed seasonal timing and lack of confidence in near term price development. The board remain positive regarding the full year fertilizer volume outlook in Ireland with application underpinned by higher livestock numbers and the requirement to maximise grass production to replenish winter fodder supplies. UK volumes will be lower for the year as a whole due mainly to reduced application of speciality and bespoke fertilizer as primary producers adopt a targeted approach to nutrition investment this year in light of the current pressures on farm incomes.

Amenity performed satisfactorily in the period with the professional sports turf channel continuing to provide solid market opportunity. The business is progressing new product formulation and application development to address customer requirements for technically oriented turf management and maintenance solutions.

Feed ingredients achieved higher volumes in the quarter reflecting active spot demand as unsettled weather drove poor grass growth and led to the requirement to house animals for longer periods due to poor ground conditions. The volume outlook for the year as a whole is indicating a marginal increase on the prior year. John Thompson, the joint venture, delivered a satisfactory result in the period against lower volume performance.

Going forward, demand for services and inputs in the final quarter is expected to be higher when compared with the prior year resulting from a greater concentration of seasonal activity. There has been an encouraging start to the quarter but confidence at farm level remains subdued reflecting the current challenging backdrop to primary output markets which is expected to make for a highly competitive trading environment. In light of the lower Q3 performance, the board are downgrading full year guidance in diluted EPS to a range of between 43c and 46c for 2016.

All the above seems to suggest the market is not getting much easier and I think these shares don’t really reflect the tough trading conditions.