Keller has now released their final results for the year ended 2016.

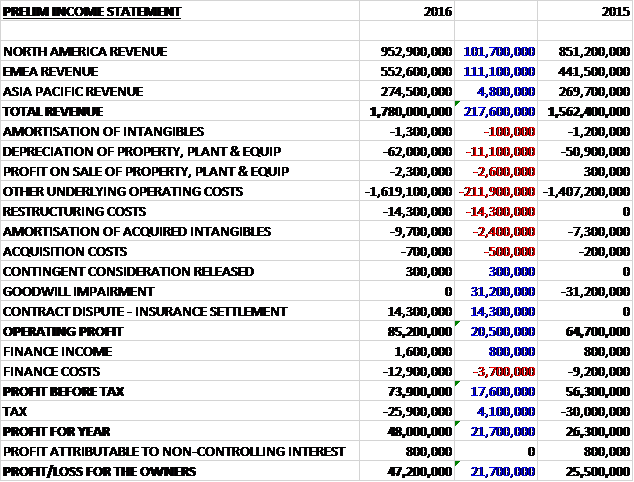

Revenues increased when compared to last year due to a £101.7M growth in North America Revenue, a £111.1M increase in EMEA revenue and a £4.8M growth in Asia Pacific revenue. Depreciation charges grew by £11.1M, there was a £2.3M loss on the sale of property, plant and equipment and other underlying operating costs increased by £211.9M. We also see £14.3M of restructuring costs, a £2.4M growth in amortisation of acquired intangibles and a £500K increase in acquisition costs being offset by the lack of any goodwill impairments which accounted for £31.2M last year and a £14.3M profit relating to the insurance settlement on the contract dispute. This all meant that the operating profit grew by £20.5M. Finance costs increased by £3.7M but tax charges reduced by £4.1M to give a profit for the year of £47.2M, a growth of £21.7M year on year. Excluding the big one-offs, however, and profit fell by £9.5M.

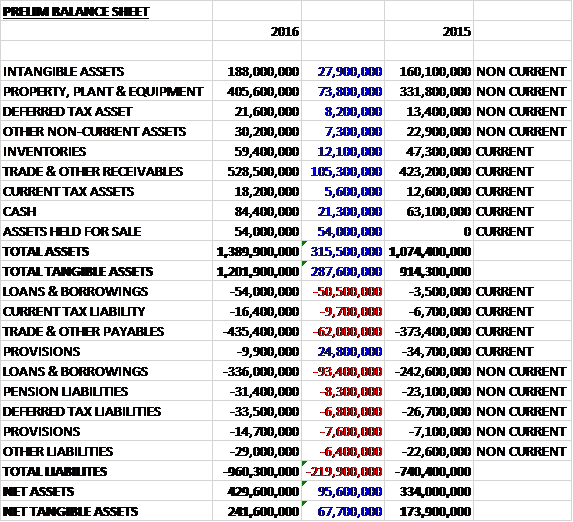

When compared to the end point of last year, total assets increased by £315.5M driven by a £100.3M growth in receivables, a £73.8M increase in property, plant and equipment, a £54M growth in assets held for sale, a £27.9M increase in intangible assets, a £21.3M growth in cash and a £12.1M increase in inventories. Total liabilities also increased during the year as a £17.2M decline in provisions was more than offset by a £143.9M growth in borrowings. The end result was a net tangible asset level of £241.6M, a growth of £67.7M year on year.

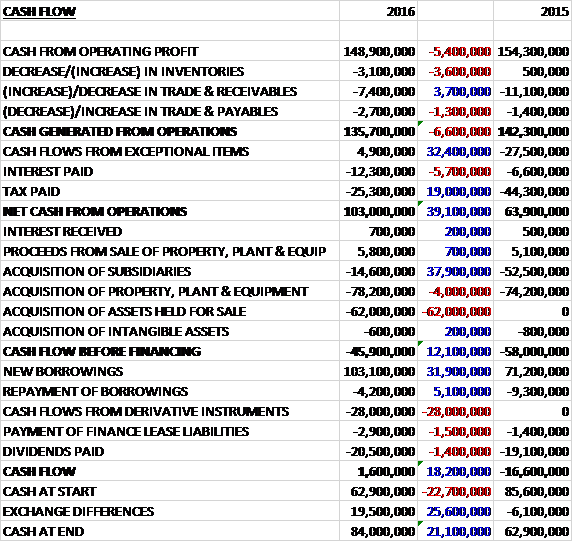

Before movements in working capital, cash profits declined by £5.4M to £148.9M. There was a cash outflow from working capital and interest costs increased by £5.7M. This was offset by a £32.4M positive swing to cash inflows from exceptional items and a £19M reduction in tax payments to give a net cash from operations of £103M, a growth of £39.1M year on year. The group spent a net £72.4M on property, plant and equipment, £14.6M on acquisitions and £62M on acquiring the building at the heart of the contract dispute. This meant that there was a cash outflow of £45.9M before financing. The group therefore took out a net £98.9M of new borrowings but saw a £28M cash outflow from derivative instruments and spent £20.5M on dividends to give a cash flow of £1.6M and a cash level of £84M at the year-end (aided by forex movements).

The operating profit in North America was £86.9M, a growth of £10.5M year on year although some £9.2M of that came from forex movements and the underlying profit growth at constant currency was £1.3M. The profit increase reflects a 4% growth in the US, partially offset by a deterioration in Canada which recorded a small loss.

The growth in the US was aided by a steadily growing construction market, driven by a growth in private construction. Hayward Baker increased profits despite fewer major contracts. Suncoast had an outstanding year, benefiting from the continued increase in housing starts where it operates, particularly in Texas. They installed new, more automated cut lines in their two largest facilities in the second half which should lead to significant productivity improvements.

These good performances were offset by reduced profits in the US piling businesses. Case and HJ Foundation returned to more normal levels of profitability due to fewer large jobs and increased competition in Chicago and Miami. McKinney had a number of poorly performing projects so the business was altered to introduce a more centralised management model. Bencor continued to perform well with its $135M project to repair and upgrade the East Branch Dam in Pennsylvania progressing to plan.

Canada continues to be a very tough market, particularly in the West. The business continued to struggle and recorded a small loss for the year. They have undertaken further cost reduction measures, reducing overheads and closing an office. Some C$8M of annualised costs have been taken out. The result was also adversely impacted by the delay in the C$43M project in Toronto in connection with the expansion of the city’s metro system. This was originally scheduled to begin in April 2016 but is now due to start in the spring of 2017.

The operating profit in the EMEA region was £30.2M, an increase of £8.9M when compared to last year and £2M of that increase came from forex movement. This much improved result reflects good performances from all the most significant European business and in particular, excellent project execution at the large project in the Caspian region.

The businesses in central Europe performed well, helped by slowly improving markets. Germany, Austria and Poland continue to benefit from the introduction of new products and ongoing improvements to existing products and techniques. All are also leading the way in helping businesses units elsewhere in the world to expand their product ranges, offering significant expertise, resources and training.

The UK also had a good year, working on a wide variety of commercial and infrastructure projects. The business had fewer poorly performing contracts than in recent years, following extensive work on tendering and execution disciplines. Whilst they have seen some market slowdown recently, much effort is currently being devoted to securing significant work on the major infrastructure projects coming up in the UK. The major project in the Caspian region was the group’s best performing contract during the year. They recently received noticed to proceed for a further $80M which will take the total project to around $180M.

The group had a difficult year in the Middle East and Africa. Revenue in the Middle East can be lumpy, being relatively dependent on large projects and there were few such projects in the first half of the year. The result also suffered from a poorly executed project completed in the first half. The revenue run rate improved in the second half and should improve significantly in 2017 following the award of two major projects; the £45M East Port Said development Complex in Egypt, and the £25M urban development project in Abu Dhabi.

Franki Africa had a very difficult year as the South African construction market contracted significantly as a result of the economic and political uncertainty in the country and many projects elsewhere in sub-Saharan Africa were delayed. Cost reduction measures allowed the business to record a small profit, however. The business recently started work on a £40M design and build contract for a foundation solution at the Clairwood Logistics Park development. This project is using a technique new to the South African market and has been introduced in conjunction with Keller experts from Europe.

The newly acquired business in Brazil saw difficult trading in a depressed economy with political challenges. The existing business is being integrated into Tecnogeo and operations from the Rio location have been transferred to Sao Paolo.

The operating loss in the Asia Pacific region was £18M, a detrimental movement of £29.7M when compared to 2015 with forex movements having a positive impact of £1.1M.

In May the group acquired the freehold of a processing and warehousing facility in Avonmouth for a consideration of £62M. The group’s final liability with regards the historic contract dispute involving the property is in part dependent on the value of the property. In order to maximise this value, the group decided to acquire the property with a view to marketing it to third parties. At the end of June the property was held at a fair value of £48M and had already been impaired by £14M by that point. As of the year-end, the fair value of the property based on an external valuation was £54M so there was a £6M impairment reversal.

As usual there were a number of exceptional items during the year. The £14.3M restructuring charge relates to asset write downs, redundancy costs and other reorganisation charges in markets experiencing significantly depressed trading conditions (Singapore, Australia, Canada and South Africa). This includes the write-down, redundancy of surplus equipment to current market values where it is not being relocated to more active parts of the group. Additional contingent consideration provided relates to the Bencor and Ellington Cross acquisitions.

The £14.3M of exceptional credits relate to the contract dispute settled in 2014. These credits are attributable to insurance proceeds received after an initial settlement with insurers, rental income less operating costs from the acquired warehouse facility and the release of the portion of the contract provision that was dependent on the valuation of the property. The contingent consideration provision released relates to amounts payable for the Austral, Franki Africa and Geo Foundations acquisitions. After the year-end the group received a further £5.9M of insurance proceeds relating to the contract dispute which will be recognised as an exceptional income in 2017.

In February the group acquired Tecnogeo, a business based in Brazil, for an initial cash consideration of £12.8M. Contingent consideration of up to £13.2M is payable based on total EBITDA in the two year period following acquisition. The acquisition generated goodwill of £6.6M. During the year, the business contributed £13.4M to revenues and a net loss of £800K. In April the group acquired Smithbridge, a business based in Australia, for an initial cash consideration of £1.8M which reflected the fair value of net assets acquired.

Conditions in the group’s major markets are not expected to change materially in 2017. The US construction market if forecast to continue to grow steadily and the group are well placed to benefit from any acceleration of infrastructure spending, although they think that this will likely be an opportunity for 2018 and beyond. The main European markets should continue to be relatively solid although they may see a slowdown in the UK. Elsewhere markets are expected to remain challenging and while they board expect to see a material improvement in the Asia Pacific results in 2017, they do not expect to see a return to profitability until 2018.

The group begin 2017 with a record order book with work to be undertaken over the next year 20% above last year on a constant currency basis. Also, the order book contains some major projects in some of the most challenging markets such as Australia, the Middle East, South Africa and Canada. The group are also beginning to see tangible results from a number of the strategic initiatives launched in the last year; product capabilities are being transferred faster, global product teams are positively impacting contract performance and real benefits are coming from improved procurement. As a result, the board is confident in the group’s prospects for 2017.

At the current share price the shares trade on an underlying PE ratio of 14.1 which falls to 9.8 on next year’s consensus forecast. After a 5% increase in the total dividend the shares are yielding 3.1% increasing to 3.3% on next year’s forecast. At the year-end the group had a net debt position of £305.6M compared to £183M at the end of last year, partly due to currency differences.

On the 12th April the group announced that it had acquired instrumentation and monitoring company GEO-Instruments in North America. The business supplies, manufactures, installs and integrates monitoring systems for buildings, excavations, bridges, railways, roads etc. It is based in Rhode Island and has annual revenues of around £4M so just a small acquisition.

On the 11th May the group released a trading update covering the first four months of the year. There has been no significant change in market trends since the final results. For the group as a whole, both revenue and profit are ahead of last year.

The North America division has had a solid start to the year but is behind the same period of 2016. EMEA has continued its growth trend of recent years, helped by ongoing good contract execution on large projects. Asia Pacific’s results show a significant year on year improvement with encouraging growth in revenue but, as expected, the division still recorded a loss in the period.

Tendering activity and contract awards remain generally healthy. The order book has increased during the year and, at the end of April, the group order book of work to be undertaken over the next year was 15% higher. As a result, the group remains on course to meet the board’s expectations for the full year.

Also the group has announced the sale of its processing and warehouse facility in Avonmouth for a cash consideration of £62M. They acquired the property in May 2016 following a dispute arising on a project completed in 2018 and since the acquisition they have received around £4M of rental income. The property was held on the balance sheet at a value of £54M so the sale realises a profit of £8M.