Waterman has now released their interim results for the year ending 2017.

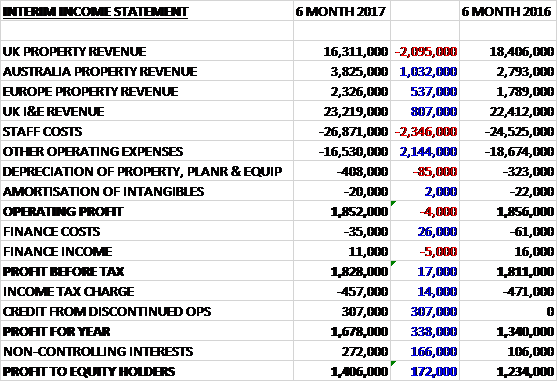

Revenues increased when compared to the first half of last year as a £2.1M reduction in UK property revenue was more than offset by a £1M growth in Australia property revenue, an £807K increase in UK I&E revenue and a £537K growth in European property revenue, aided by forex movements. Staff costs increased by £2.3M but other operating expenses reduced by £2.1M. An £85K growth in depreciation meant that the operating profit was broadly flat, falling by just £4K. Finance costs were down £26K and tax charges fell by £14K before a £307K credit from discontinued operations relating to forex gains on the liquidation of the Moscow entity meant that the profit for the period came in at £1.4M, a growth of £172K year on year.

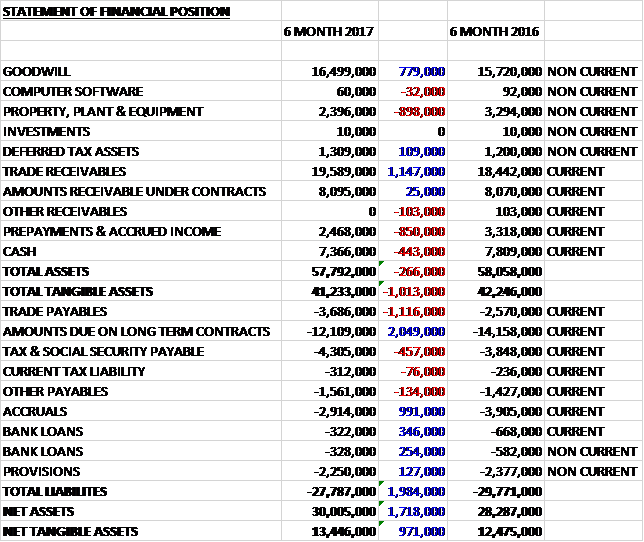

When compared to the end point of last year, total assets declined by £266K driven by an £898K fall in property, plant and equipment, an £850K decline in prepayments and a £443K decrease in cash, partially offset by a £1.1M growth in trade receivables and a £779K increase in goodwill. Total liabilities also declined during the period as a £2M decline in amounts due on long term contracts and a £991K fall in accruals was partially offset by a £1.1M growth in trade payables. The end result was a net tangible asset level of £13.4M, a growth of £971 over the past six months.

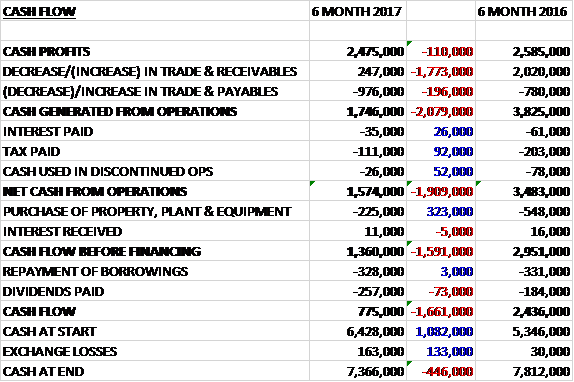

Before movements in working capital, cash profits declined by £110K to £2.5M. There was a cash outflow from working capital and after tax payments fell by £92K the net cash from operations was £1.6M, a decline of £1.9M year on year. The group spent just £225K on capex to give a free cash flow of £1.4M, of which £328K went on loan repayments and £257K was paid out in dividends. This all meant that there was a cash flow of £775K for the period and a cash level of £7.4M at the period-end.

The operating profit for the UK property business was £579K, a decline of £693K year on year with a fall in margins. The UK structural team have continued to perform well, securing new commissions from a range of clients including British Land, Land Securities, Hammerson, Lend Lease, AVIVA, Berkeley, Barratt and Kier. Whilst the building services team in London have suffered from delayed starts to projects in the commercial and residential markets during the period, it is expected that the situation will improve during the year. Outside London the regional offices have performed better with a wide range of projects in education, performing arts, leisure, student accommodation and healthcare markets.

The group have teamed up with Stanhope and Mitsui in a UK pilot of the National Australian Built Environment Rating System on the recently completed new Angel Court development designed by Waterman. This study will assess over a year long period the energy use within the completed building and compare that to the design parameters. The building will then be verified by an investment grade rating using the measured data. The London and Australian teams are both involved in this initiative.

The operating profit for the Australian business was £696K, a growth of £360K when compared to the first half of last year with some of that, but not all, coming from favourable forex movements. New commissions have continued to be won, particularly in the healthcare, judicial, residential and telecoms markets. They are currently working for Westpac Bank and Commonwealth Bank on their frameworks for upgrading their existing high street retail outlets and for Aldi on their store refurbishment programme.

The operating profit for the European business was £217K, an increase of £99K when compared to the first half of 2016. In Ireland, the group has designed the tallest and largest building project in Dublin which is currently undergoing construction. The Irish economy has been the fastest growing in the Eurozone for the last three years and the group is benefiting from the increasing demand for consulting engineering services for development in the residential, commercial offices, retail and leisure markets.

The operating profit in the UK I&E business was £585K a fall of £17K year on year following the investment in the recruitment of several senior staff to further expand the revenue from public sector frameworks and highways infrastructure. During the last six months the group has been appointed on a new four year framework for Swindon Borough Council and are currently discussing a two year extension to London Borough of Bexley framework where they have been providing services on the existing framework for 21 years.

The group’s pre-planning team which provides environmental impact assessments and sustainability advice on developments has been particularly busy over the past six months. Since Brexit the group have experienced an increase in activity by their clients. They are currently involved in Battersea Power Station, Canada Water for British Land, Ballymore’s Leamouth South scheme, Old Oak Park for Car Giant and London and Regional, and Brent Cross for Hammerson and Standard Life. These are all significant developments and they will provide future opportunities for the property teams.

The outsourcing team have started a programme to diversify their business model into new areas such as water and environmental services, as well as continuing to target their existing highways and transportation markets. They have made good progress and secured initial secondments into Natural Resource Wales and the Environment Agency.

Going forward the board anticipates that the group will continue to experience a stable trading outlook overall with revenue, profit and operating margin generally in line with the prior year. Whilst trading conditions in the UK are expected to remain challenging, there have been some recently announced large commissions such as the MOD’s Army Basing Programme, the planned extension to the Brent Cross shopping centre and technical advice for the feasibility studies of new schools.

In addition, the specialist highways and transportation outsourcing business is expecting an uplift in secondment activity following the announcement in the Autumn statement confirming the government’s commitment to invest over £1.3BN to ease congestion on roads. Overseas the contribution fr5om the offices in Australia and Ireland is expected to increase due to improved performance. The markets in these two countries are particularly buoyant with investment in public social infrastructure such as hospitals, schools and prisons, and in the private sector in residential, commercial and retail development. Whilst 2017 is proving to be a period of consolidation, the board looks to the future with measured optimism.

At the current share price the shares are trading on a PE ratio of 9.6 which rises to 9.8 on the full year consensus forecast. After a 33% increase in the interim dividend, the shares are yielding 4.7% which increases to 5.5% on the full year forecast. At the period-end the group had a net cash position of £6.7M compared to £6.6M at the same point of last year.

Overall then this has been a sluggish period for the group. Although overall profits increased, excluding the forex gain from the closed Russian business, they declined in the period. The operating cash flow also declined but the group still managed to retain a decent amount of free cash. The Australian and Irish businesses are both doing well, both benefiting from forex movements and increased volumes of work. In the UK times are harder with the I&E business remaining flat with more investments being made for future growth, and the UK property business suffered a decline, not helped by delays in building services projects.

Overall, there does not seem to be much if any growth here, with results weighed down by weakness in the UK. With a forward PE of 9.8 and dividend yield of 5.5%, it could be argued that this is already included in the price. There could be some decent value here but until there is some evidence of growth, I am a little reticent to buy and shares.

On the 28th March the group announced that it secured a two year extension to its existing partnership term contract with the London borough of Bexley until September 2019. It will involve the provision of traffic and transportation engineering services, civil engineering, highways and infrastructure, bridgeworks, drainage, principal designers and technical staff secondment. Over the past year the team has delivered the replacement of Bexley High Street Bridge, the second stage of Bexleyheath town centre revitalisation on public realm design adjacent to the new Crossrail station at Abbey Wood. The framework is expected to generate annual fees of around £1.7M.

On the 9th May the group announced that it had received an offer from CTI Engineering whereby Waterman shareholders will receive £1.40 per share which represents an 83% premium to the closing price on the prior day. This offer values the group at £43M. There only seems to be around 26% of shares acquired so far but this looks a good offer to me and I would not be surprised if it went through.