Keller has now released their final results for the year ended 2017.

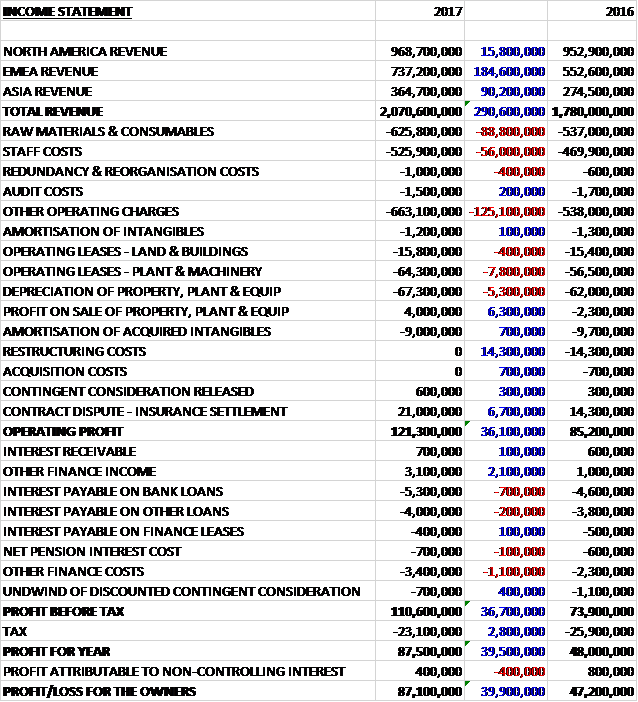

Revenues increased when compared to last year with a £184.6M growth in EMEA revenue, a £90.2M increase in Asia revenue and a £15.8M growth in North America revenue. Raw material costs increased by £88.8M, staff costs were up £56M and other operating charges increased by £125.1M. WE also see am £8.2M increase in operating lease costs and a £5.3M growth in depreciation. Offsetting this was a £6.3M profit on the sale of assets, a £14.3M reduction in restricting costs and a £6.7M increase in the insurance settlement following the contract dispute. All this meant that the operating profit grew by £36.1M. Finance income increased by £2.2M but interest payments grew by £800K and other finance costs were up £1.1M. After tax charges reduced by £2.8M, due to the credit for the revaluation of US deferred tax liabilities, however, the profit for the year was £87.1M, a growth of £39.9M year on year.

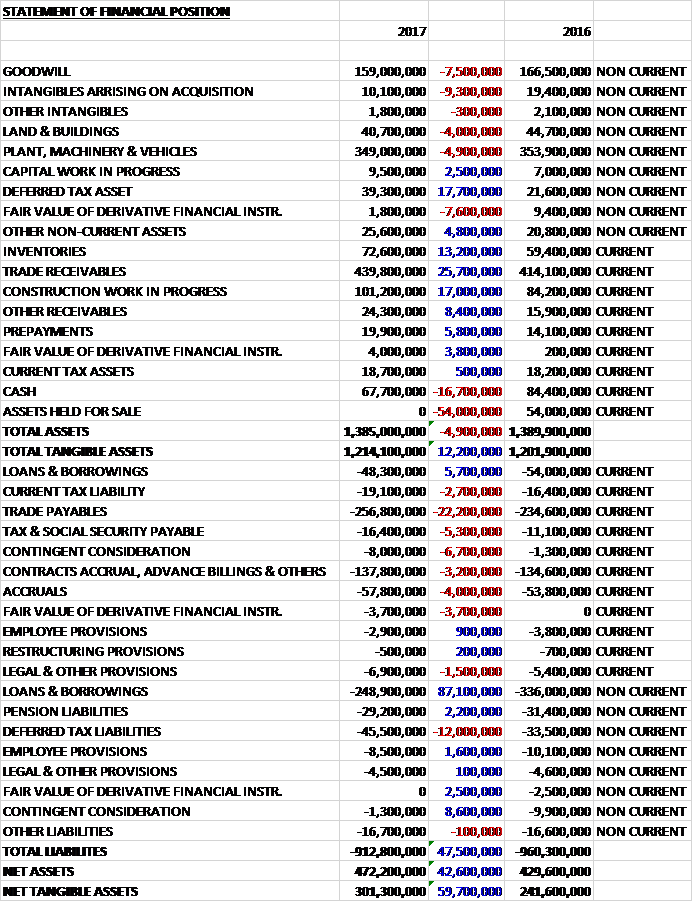

When compared to the end point of last year, total assets declined by £4.9M, driven by a £54M reduction in assets held for sale, a £16.7M decline in cash, a £9.3M fall in acquired intangibles and a £7.5M decrease in goodwill, partially offset by a £25.7M growth in trade receivables, a £17.7M increase in deferred tax assets, a £17M growth in construction work in progress and a £13.2M increase in inventories. Total liabilities also declined during the year as a £22.2M growth in trade payables was more than offset by a £92.8M fall in borrowings. The end result was a net tangible asset level of £301.3M, a growth of £59.7M year on year.

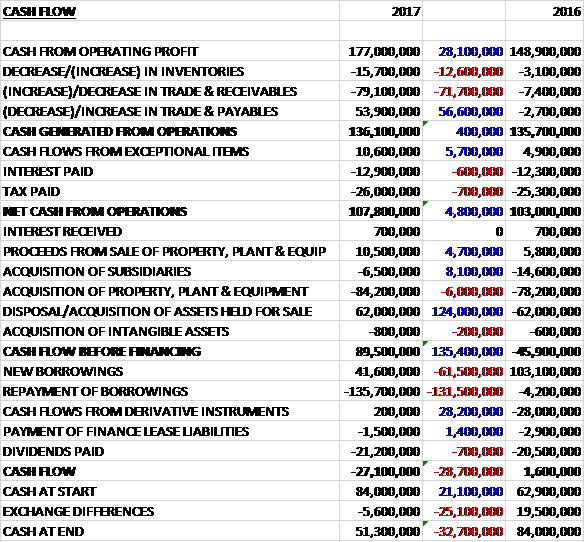

Before movements in working capital, cash profits increased by £28.1M to £177M. There was a cash outflow from working capital but the £600K increase in interest payments and £700K growth in tax payments were more than offset by the £5.7M increase in cash flows from exceptional items to give a net cash from operations of £107.8M, a growth of £4.8M year on year. The group made £10.5M from the sale of assets and £62M on an asset held for sale. They spent £6.5M on acquisitions, £84.2M on fixed assets and £800K on intangible assets to give a free cash flow of £89.5M. Of this, £21.2M was paid out in dividends and a net £94.1M was used to pay back borrowings. This gave a cash outflow of £27.1M and a cash level of £51.3M at the year-end.

The operating profit in the North America division was £78.7M, a decline of £8.2M year on year. In the first half, revenue decreased by 10% but the division returned to growth in the second half in revenue terms. Profits were still lower than in 2016, however, largely due to the impact of hurricanes Harvey and Irma in Q3 which has an estimate impact of £3M on profits. The year-end North American order book was 5% above last year, which, together with the improving trend in underlying trading, gives the board confidence for 2018.

The US construction market as a whole remains solid but with significant regional and sectoral variations. Residential construction grew by 10% but public expenditure on construction was down 3% and private non-residential spend was flat. The group’s US business had a mixed year. Hayward Baker produced record results and its business model of undertaking a wide variety of small to medium sized contracts across a broad range pf products continues to produce good results. Following some management changes early in the year, there was an improvement in the business’ Western region which disappointed over the past two years.

This strong performance was offset by lower profits at both Case and HJ Foundation which, between them, reported profits £16M lower than last year. For HJ Foundation the reduction reflects a return to more normal levels after the boom period in Miami which attracted a major competitor to the market. Case had a very disappointing year as a result of fewer large projects, particularly in Chicago, as well as some difficult projects. The business starts 2018 with a strong order book, however, and performance is expected to improve next year.

Bencor had a steady year, continuing work on the major remediation project at East Branch Dam and McKinney, which had a disappointing 2016, reported an improved result this year.

Suncoast, which mainly serves the residential construction market, had healthy revenue growth in 2017, benefitting from the continued increase in housing starts where it operates. The business faced some significant raw material price increases, however, which it was unable to recover from customers in full. As a result, profits were significantly lower than last year.

The Canadian business continues to operate in a difficult market and in June they announced changes in leadership and some other cost cutting measures. These, together with good progress on the major $43 Toronto subway contract, and the refocusing of the business towards urban areas, have resulted in the business returning to profit in the second half of the year.

The operating profit in the EMEA division was £53.3M, a growth of £23.1M when compared to last year. This increase is largely the result of two large projects, both of which were substantially complete at the year-end; the Caspian project and Zayed City in Abu Dhabi. Between them, these projects accounted for around £30M of profit and most of the year on year increase. As these are now mostly complete, the division profit in 2018 will be well down on 2017. 2018 is still expected to be better than 2016, however, as a result of a healthy order book and further improvements in the underlying business.

The core businesses in central Europe all performed well, reflecting strong project disciplines and growing construction markets in Germany, Austria, Poland. The South East Europe business unit, centred around Austria, had its best ever year with record revenue and profit. The UK had a solid year, working on a wide variety of commercial and infrastructure projects. They have seen a notable slowdown in orders in recent months, however, and expect 2018 to be a challenging year. The major infrastructure projects coming up in the UK should mean that the market should pick up in 2019.

The excellent execution of the major project in the Caspian region continued but it is now over 90% complete. The group had a very busy year in the Middle East, largely due to working on two major projects; an urban development project in Zayed City, Abu Dhabi, which is now complete, and the East Port Said development complex in Egypt which will complete in H1 2018. As a result revenue was more than double the 2016 total. There are a number of good prospects in the region and the current challenge for the business is to replenish the order book.

Tecnogeo in Brazil continues to struggle in a very difficult market. Franki Africa performed well, increasing profits. The £40M design and build contract for a foundation solution in the Clairwood Logistics Park development near Durban has exceeded original expectations. The division’s order book at the year-end is 20% down on last year reflecting the ending of some large projects.

The operating loss in the APAC division was £16.5M, an improvement of £1.5M when compared to 2016. The losses are largely as a result of two major contracts in Australia where adverse ground conditions, technical issues and a contractual dispute resulted in a total loss of £14M on these contracts. The group are changing the leadership of the division with Peter Wyton joining from AECOM in February 2018 as president.

The difficult markets in the region are slowly recovering, with encouraging signs of new Australian mining and infrastructure projects. The year-end order book was more than 20% above last year which means the board remains confident of a return to divisional profitability in 2018.

The group’s geotechnical business in Australia had an improved year and losses were materially reduced. Pricing remains challenging but investment in infrastructure in Australia is robust, the business has a good order book and they are hopeful of winning some major work on the Melbourne metro extension project. As a result, the board are confident that the business will return to profit in 2018.

It was a very mixed year for the near-shore marine businesses in Australia. Waterway was already having a difficult year in a tough east coast market before being hit by a negative arbitration outcome in December in connection with a contract dispute on a project in NSW. The business has subsequently negotiated a settlement with the customer and are undertaking remedial works.

Austral, which operates mainly in the west of Australia had an improved year and has been very busy bidding work in recent months as investment in the resources industry returns. The business has an excellent order book and is poised for a strong 2018.

Revenue in ASEA was broadly flat with a significant increase in Malaysia as a result of an improving market and the introduction of new products, offset by a significant decrease in Singapore following the downsizing of the piling business.

The business was still loss making in the year but at a lower level than 2016. It continued to be challenged by a very difficult pricing environment for heavy foundations projects, some legacy resource piling contracts and additional costs and teething problems associated with introducing new products. On the positive side, project execution improved in the second half. The ground improvement side of the business was profitable, helped by the large vibro-compaction constract at Changi airport. The Indian business performed well with revenues doubling and margin increasing.

During the year the group extended their branch network and product range. They have two new branches in Hamburg and Charlotte; brought their soil mixing capability into Singapore and Malaysia; won their first diaphragm wall jobs in India; and introduced new ground improvement techniques into South Africa. They also invested in a new marine team to leverage their experience in Australia in near-shore marine construction into new geographies.

In March the group acquired Geo Instruments, an instrumentation and monitoring company based in North America, for a cash consideration of £2.8M which generated £500K in goodwill. In the ten months of ownership, the business contributed a profit of £400K so it seems like a decent small acquisition. In January the group announced their intention to acquire Moretrench, a geotechnical contractor in the US. If completed this will further strengthen their US East Coast presence and add new specialist technical capabilities to the group.

There were a number of non-underling items in the year. Additional contingent consideration of £1.6M was provided, relating to the Geo Foundations and Ellington Cross acquisitions. There was a £21M profit relating to the contract dispute representing the gain on disposal of the freehold of the processing and warehousing facility near Bristol which was acquired in 2016 (£8M); rental income less operating costs to the date of disposal; and insurance recoveries in the period. In all, the group has recovered £35.3M of the original £54M provision relating to this dispute and they are not expecting any further recoveries.

Going forward, the year-end order book excluding the Caspian project was up 5%, giving the board confidence for the start of 2018. Most of their markets remain robust and bidding activity is at a healthy level. Overall, despite the completion of the Caspian project, they expect 2018 to be another year of underlying progress, albeit with forex movements offering headwinds. Two significant loss making contracts in the APAC division masked some good progress there and the board expect it to return to profit in 2018.

At the current share price the shares are trading on a PE ratio of 11.4 which falls to 10.4 on next year’s consensus forecast. After a 20% increase in the total dividend the shares are yielding 3.3% which increases to 3.4% on next year’s forecast. At the year-end the group had a net debt position of £229.5M compared to £305.6M at the end of last year.

On the 23rd May the group released a trading update covering the first four months of the year. They have made a positive start with like for like revenue growth and modest profit growth, despite the impact of poor weather across North America and Europe and the wind down of the Caspian project. Tendering activity and contract awards remain healthy and the order book of work to be undertaken over the next year is 4% higher than last year, excluding the Caspian project.

In North America the first two months of the year were impacted by poor weather, but trading improved notably in the next two months. The US construction market as a whole remains solid and continues to growth, although Suncoast is having to contend with rising steel prices. The integration of Moretrench has started well.

In EMEA, despite poor weather across most of Europe in Q1, the core business performed in line with expectations. The Middle East is having a quieter year following the completion of its two major projects and the Brazilian market remains challenging. Excluding the Caspian project, they continue to expect further progress in the region during the year.

In APAC, the actions taken to restructure the business are delivering results. Revenue growth is encouraging, particularly in Australia, as a result of a healthy level of infrastructure work and the continued upturn in investment from the resources industry. Although pricing remains challenging in certain market segments, the board continues to expect that the division will return to profitability in 2018.

Overall the group remains on course to meet the board’s expectations for the full year.

Overall then this has been a fairly decent year for the group. Profits were up, net assets increased and the operating cash flow improved with some decent amounts of free cash being generated (aided by the insurance pay out). The performance in the regions has been mixed. Profits were down in North America, mainly due to the impact of the hurricanes, although Q1 has been hit by poor weather too.

Profits in the EMEA division have been strong, mainly due to the performance of two large contracts which have now been finished. The APAC region is still struggling due to two loss making contracts and weakness in Singapore but there was some improvement in the year and the board are forecasting a return to profit.

It seems that there are a number of headwinds – notably the lack of no new large projects in the Middle East to replace the old ones, an increase in raw material costs and some continued weakness in APAC. This is balanced against the potential return to profit in the region and the decently performing underlying business. The forward PE of 10.4 and yield of 3.4% doesn’t look too expensive and is probably about right.

On the 29th May the group announced a 50:50 joint venture with Intrafor has been awarded a £113M contract for work on the metro tunnel project in Melbourne. The contract is to construct the substructure retention walls and foundation piling for the stations. It will require two diaphragm wall cutters, four wall grabs and up to 12 piling rigs. The joint venture is currently mobilising teams and equipment with work starting this month. The majority of packages will finish mid-2019 but it is anticipated work will continue through to 2020.