TT Electronics has now released their final results for the year ended 2017.

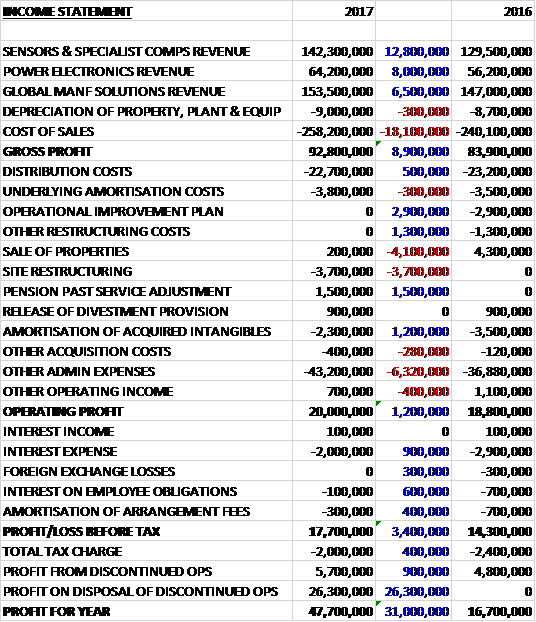

Revenues increased when compared to last year due to a £12.8M growth in sensors revenue, an £8M increase in power electronics revenue and a £6.5M growth in global manufacturing solutions revenue. Cost of sales also increased to give a gross profit £8.9M higher. Distribution costs were down £500K, the amortisation of acquired intangibles fell by £1.2M and there were no operational improvement plan costs, or other restructuring costs, which accounted for £2.9M and £1.3M respectively. There was also a £1.5M gain from pension past service adjustments but the group brought in £4.1M less from the sale of properties, and incurred £3.7M of site restructuring along with £6.3M more other admin costs, all of which gave an operating profit £1.2M higher. Interest expenses and pension interest fell during the year and the tax charge declined by £400K to give a continuing profit of £15.7M, a growth of £3.8M year on year.

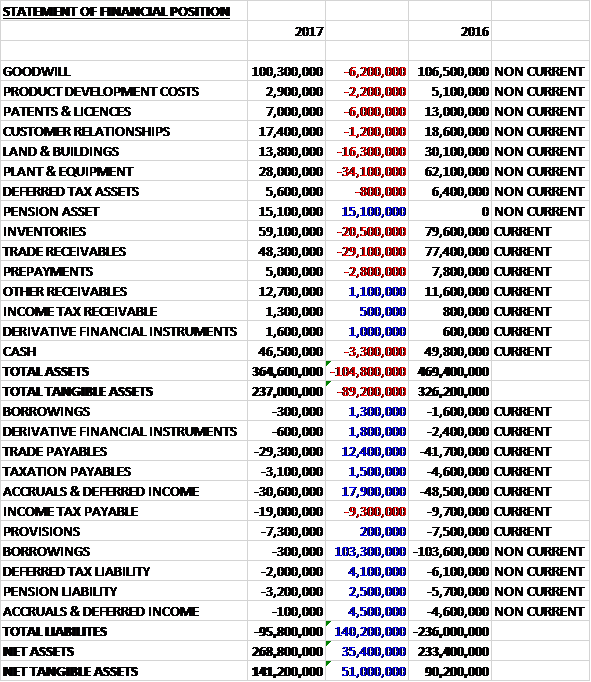

When compared to the end point of last year, total assets declined by £104.8M driven by a £34.1M fall in plant and equipment, a £29.1M decrease in trade receivables, a £20.5M fall in inventories and a £16.3M decline in land and buildings, partially offset by a £15.1M growth in the pension asset. Total liabilities also declined due to a £104.6M fall in borrowings, a £17.9M decrease in accruals and deferred income and a £12.4M decline in trade payables, partially offset by a £9.3M growth in tax payables. The end result was a net tangible asset level of £141.2M, a growth of £51M year on year.

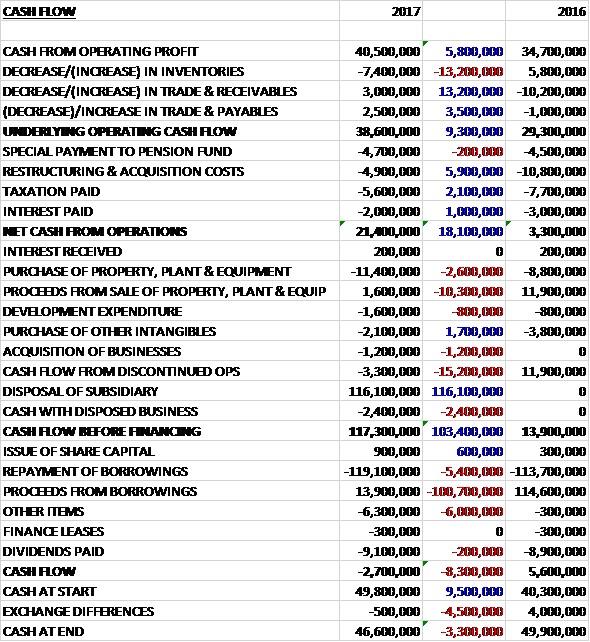

Before movements in working capital, cash profits increased by £5.8M to £40.5M. There was a cash outflow from working capital but this was less than last year. Restructuring costs were £5.9M lower, tax payments fell by £2.1M and interest payments were down £1M to give a net cash from operations of £21.4M, an increase of £18.1M year on year. The group spent £11.4M on property, plant and equipment, £1.6M on development expenditure, £2.1M on other intangibles and £1.2M on acquisitions. They also gained £110.4M from the disposal of the business so before financing there was a cash flow of £117.3M. Of this, a net £105.2M was used to repay borrowings, £9.1M went on dividends and £6.3M on “other items”. This gave a cash outflow of £2.7M for the year and a cash level of £46.6M at the year-end.

The operating profit in the Sensors and Specialist Component division was £18.8M, a growth of £3.3M year on year. This represents a 21% increase and a 15% increase at constant currency. Revenues increased by 6% at constant currency as a result of market share gains and a positive market. The profitability also increased as a result of operational leverage on the organic revenue growth and margin mix improved in the second half expected.

Management have identified three areas of their focus areas for growth and where they are concentrating their R&D spend; current sensing, circuit protection, optoelectronic assembly solutions; and automotive power inductors.

They have delivered strong growth in current sensing, circuit protection and signal conditioning product lines. This is a result of strong demand coupled with market share gains, backed by favourable lead times and increased capacity. They have increased sales to customers in industrial and consumer goods, with an existing aerospace and defence customer ramping up an existing programme.

Their optoelectronics assemblies have seen good growth, primarily driven by industrial and automotive customers in the US where market conditions have been favourable. Their magnetics business has focused on power inductors for automotive where one of their customers has won a new programme with a German OEM.

During the year they increased their spend on R&D in the division by 7%, and launched ten new products. This includes four new products launched in the current business responding to customer demand for smaller and lighter components, and extended capabilities to protect circuits from greater power surges.

The operating profit in the Power Electronics division was £6.2M, an increase of £1.2M when compared to last year. Revenues increased by 12% on an organic basis including the one-off last time buy activity, now complete, associated with moving production from Fullerton to Bedlington. The growth was a result of continued platform growth in aerospace and defence and the ramp up of product lines that were outsourced to the group from a global engine manufacture.

In the first half the group acquired Cletronics, a small US-based manufacturer of electromagnetic components for the aerospace industry for £1.2M. The acquisition helped accelerate the strategy for their power electronics capabilities in North America and adds product and technical breadth to the capabilities acquired with Aero Stanrew in 2015. The business contributed £200K of underlying operating profit in the nine months of ownership.

The group has seen good growth from their partnership with Rolls Royce to provide power and control microcircuits used in the engine control unit for the next generation of aerospace engines. They have also seen good growth from the ramp up of product lines that were outsourced to them from a global engine manufacturer. In addition they have also seen an increase in volumes associated with winning additional content on the Gulfstream business jets and the ramp up of the Airbus A350XWB.

During the year they launched six new products in partnership with their customers, underpinning their future growth. New products launched include a magnetic component for an Electronic Load Management System for aerospace and defence applications and power and control microcircuits including their application-specific integrated circuit product ranges.

The operating profit in the Global Manufacturing Solutions division was £6.5M, a growth of £200K when compared to 2016. This represents a 3% increase but a 3% decline at constant currency. Organic revenue increased by 2% with growth stronger in the second half, especially in Asia driven by customers in the medical and transportation markets. Likewise, the operating profit improved in the second half.

In the US the aerospace and defence market strengthened and the group was selected as a strategic partner and won multi-year contracts with an OEM customer. This win was complemented by four further aerospace and defence contracts won with new and existing customers. Medical markets also strengthened with macro drivers in Asia maintaining strong investment. The group won a number of new customers for PCBA, systems integration and cable assemblies in medical markets in both the US and Asia. In Asia, they also won a new contract for a rail infrastructure project.

In the second half of the year the group announced that the Romania site would close in H1 2018 as part of the separation of the transportation division. Customer qualification to move production to the UK and China is progressing as expected. Although the European operations have faced challenging conditions, they have made good progress with a transportation customer with whom they have doubled their revenues over three years.

In October the group disposed of the Transportation Sensing and Control division to AVX Corp for £125.6M in cash. In the year the business generated profit of £5.7M and the generated a profit of £26.3M on disposal.

In 2016 the triennial valuation of the UK pension scheme showed a deficit of £46M. The group agreed additional fixed contributions until 2020 which amount to £4.9M, £5.1M and £3.9M over the next three years. This year the group paid £2.4M. Both the UK and US schemes are closed to future accrual.

During the year total restructuring costs amounted to £1.6M of which £3.7M related to costs associated with site restructuring, a credit in respect of a pension past service adjustment under which members agreed to exchange future pension increases for an additional amount of initial pension and a profit arising on the sale of certain properties (£200K). In December new legislation was enacted changing the basis of US tax which resulted in a one-off benefit of £1.8M arising due to enacted changes in tax rate. During the year acquisition and disposal related costs amounted to £2.7M which related to £400K of acquisition costs and £2.3M of amortisation of acquired intangible assets.

In February 2018 the group announced the cash offer for Stadium Group for a total consideration of £45.8M plus net debt acquired of £11.8M. The business is a leading supplier for design led technologies for the industrial, aerospace and defence, medical and transportation sectors.

Going forward, the momentum in the operational performance and the improved order book (in part due to customers placing orders further ahead than at this time last year) give the board confidence that despite current forex headwinds, they will make strong progress in 2018.

At the year-end the group had a net cash position of £47M compared to £55.4M at the end of last year. At the current share price the shares are trading on a PE ratio of 25.8 which falls to 19.2 on next year’s consensus forecast. After a 4% increase in the total dividend the shares are yielding 2.4% which increases to 2.5% on next year’s forecast.

On the 10th May the group released a trading update covering the first four months of the year. Revenues was up 4% on an organic basis. Order intake has been good and the order book across all three divisions continues to be ahead of last year. The order book strength is in part due to customers continuing to place orders further ahead than at this time last year as a result of ongoing industry-wide component shortages but provides increasing confidence of delivering growth in the year.

Good growth translated into margin progression in the Sensors and Global Manufacturing solutions divisions. As a result of continued strong demand in the Power Electronics division, additional investment has been made to meet customer schedules and to build capacity to deliver anticipated future growth. These costs, together with the absence of last year’s high margin one-off sales will impact the division’s margin in the first half, which is expected to normalise for the full year.

In April the group completed the acquisition of Stadium for an enterprise value of £59.7M. In the first four months of the year, its revenue is up 5% at constant currency. The order book is ahead of the prior year, providing confidence of the business meeting the board’s trading expectations.

The group is investing £3M to create a fit for purpose facility to support strategic development and during the period they realised net proceeds of around £4M from the sale of a surplus site in the UK. Overall the board have increasing confidence of making strong progress in 2018 and they continue to review a number of acquisition opportunities.

Overall then this has been a decent year for the group. Profits have increased, net assets are up and the operating cash flow has improved with some free cash being generated. The Sensors and specialist components division and power electronics business both performed well but the GMS division struggled with a decline in constant currency profits. The performance perked up somewhat in H2, however. The New Year has started fairly well but Power Electronics division saw margins temporarily decline. The forward PE of 19.2 and yield of 2.5% looks rather expensive to me but momentum is with the shares and I will likely hold on for now.

On the 4th June the group announced the acquisition of Precision Inc for an initial consideration of $23.5M and up to an additional $4M contingent consideration. The business is headquartered in the US and is a designer and manufacturer of precision electromagnetic product solutions for critical applications. They have medical, industrial, aerospace and defence markets.

The business brings new design, simulation and manufacturing capabilities to the group in electromagnetics, one of the four focus areas for growth. Their products are primarily sold into medical applications including pacemakers, neurological implants and other in-body equipment as well as external diagnostic equipment such as dialysis machines and MRI scanners. They also serve industrial, aerospace and defence customers in applications including satellite power supplies and aerospace guidance systems.

Last year the business reported EBIT of $2.3M and gross assets of $7.8M and the acquisition is expected to be earnings enhancing immediately.