MPAC has now released their final results for the year ended 2017.

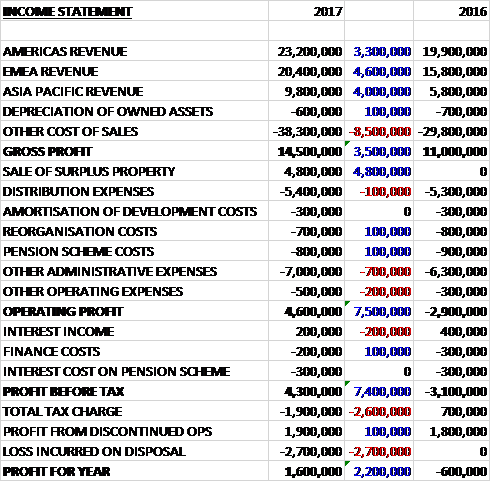

Revenues increased when compared to last year due to a £4.6M growth in EMEA revenue, a £4M increase in Asia Pacific revenue and a £3.3M growth in Americas revenue. Cost of sales increased by £8.5M to give a gross profit £3.5M ahead of 2016. The group made £4.8M on the sale of a surplus property but other admin expenses increased by £600K and other operating expenses were up £200K to give an operating profit £7.5M higher. Interest income declined somewhat and the total tax charge increased by £2.6M to give a continuing profit of £2.4M, a growth of £4.8M year on year.

When compared to the end point of last year, total assets declined by £1.9M driven by a £10.6M decrease in inventories, a £7.8M decline in goodwill, a £6.3M fall in product development costs, a £3.1M decline in land and buildings and a £2.9M decrease in deferred tax assets, partially offset by a £21.3M growth in cash and a £13M increase in the pension asset. Total liabilities also declined during the year as a £4.3M growth in deferred tax liabilities was more than offset by a £7M decline in bank borrowings and a £2.6M decrease in deposits received on account. The end result was a net tangible asset level of £41.9M, a growth of £21.7M year on year.

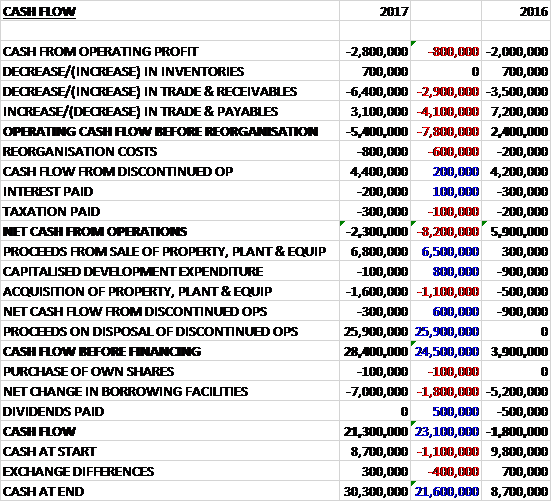

Before movements in working capital, cash losses widened by £800K to £2.8M. There was a further cash outflow from working capital and after reorganisation cost increased by £600K and £4.4M cash inflow from the discontinued operation was taken into account, the net cash outflow from operations was £2.3M, a detrimental movement of £8.2M year on year. The group received £6.8M from the sale of fixed assets and £25.9M from the sale of the discontinued operation and spent £1.6M on property, plant and equipment to give a cash inflow of £28.4M before financing. This was used to pay off £7M of loans to give a cash flow of £21.3M for the year and a cash level of £30.3M at the year-end.

The gross profit in the OE business was £9.2M, a growth of £3.8M year on year. Order intake was 29% ahead of last year. In the Americas and EMEA significant increases in order intake were seen across healthcare, pharmaceutical and food and beverage markets. Asia also saw strong order intake with orders received primarily from the food and beverage markets. Sales in the food and beverage markets grew by 47% and sales to the healthcare market saw a growth rate of 38%.

Americas sales increased by £2.8M with sales to the food and beverage market more than doubling and sales to the healthcare market seeing growth of 23%. EMEA sales increased by 41%. In the pharmaceuticals market the investment plans of a major customer were directed towards Europe which resulted in sales to the region increasing significantly. In 2016 a similar sale to the same major customer was recorded in the Americas. Sales to the healthcare market increased by 60% but a change in mix saw sales to the food and beverage market reduce by 17%.

Asia Pacific sales, dominated by the food and beverage market, more than doubled in the period. Overall order prospects remain strong and activity levels across the business remain high such that the business is well positioned to move into the coming year.

The gross profit in the Service business was £5.4M, a decline of £200K when compared to last year. Overall order intake was 3% ahead of 2016 and turnover increased by 3%. A new services Director joined in July and by the end of the year the group further increased focused on the expansion of the business with the recruitment of a number of additional staff and the order intake increased towards the end of the year.

Americas sales in the period increased by £500K. Sales to the food and beverage market increased by 20%, offsetting a slight reduction in sales to the healthcare market. Overall order intake in the region was ahead of 2016 with order prospects remaining strong in 2018. EMEA sales in the period were flat and order intake was broadly in line with sales. The region saw a change in mix in sales with an increase in sales to the pharmaceutical market offset by a softening in healthcare activity. Asian sales declined by £200K. A change in mix from spare parts to additional equipment sales reduced service gross margins in the year.

In August the group completed the sale of the Instrumentation and Tobacco business to Coesia for a gross consideration of £30M. Net proceeds were £23.5M and the business generated profits of £1.9M during the year.

In line with the plans to improve the operational efficiency of the group, in December they completed the sale of a freehold property in Canada for a gross consideration of $11.7M , generating a profit on disposal of £4.8M, with the business moving to a new purpose built facility in the region, which incurred restructuring costs. The new facility is only leasehold, however, with a ten year lease at a cost of $600K per year. The group also invested in a new expanded facility in Singapore. These new leased facilities provide a modern office environment which provides a platform for future development of sales in the Asia Pacific region.

The net non-underlying profit for the year was £3.3M. This comprised £800K of admin costs relating to the pension scheme (not non-underlying in my opinion), and reorganisation and restructuring costs of £700K. A profit of £4.8M was realised on the sale of property in Canada. The group is defining the restructuring costs as changes made to the senior management team, and the new locations in Canada and Singapore, which again, I’m not sure are really non-underlying.

The group paid a one-off amount to the pension fund of £2.4M, representing 10% of the proceeds of the sale of the Instrumentation and Tobacco machinery division. They will continue to pay a sum of £1.8M per annum to the fund in deficit recovery payments with more to pay should profits and dividends meet certain levels. The scheme’s assets have benefited from strong returns in the year which has increased the schemes surplus. The recovery plan will be reassessed as part of the 2018 actuarial valuation which is expected to be completed in the second half of 2019.

Going forward the group entered 2018 with a stronger order book than a year before and with order intake and sales both ahead of last year, the group’s future prospects remain positive.

At the year-end the group had a net cash position of £29.4M compared to £800K when compared to the end of last year. The directors have decided not to recommend the payment of a final dividend. The group made an underling loss so there is no PE ratio but on next year’s consensus forecast it is 22.3.

On the 19th April the group released a trading update covering Q1 which was ahead of last year and in line with board expectations. It was also announced that Chairman Phil Moorhouse was stepping down from the board for personal reasons having been in the position for seven years. Andrew Kitchingman will be appointed as Chairman.

Overall then this has been a bit of a mixed performance from the group. Profits increased due to the sale and subsequent lease of properties in Canada, otherwise they would have been flat. Net assets improved strongly but the cash losses widened. The remaining OE business is performing well and growing strongly but the Services business is more sluggish with profits falling slightly. So far this year, Q1 is ahead of last year but despite the net cash, these shares look rather expensive with a forward PE of 22.3. Things remain sound for the moment however so I am holding on for now to see what is done with that cash pile.

On the 18th July the group released a trading update covering the first half of the year. It was noted that despite a positive start to the year and a continued increase in revenues, the business climate has softened significantly as the year progressed. This was attributable in part to general economic as well as Brexit related uncertainty, leading to customers deferring machinery investment decisions.

The group’s financial performance during the period has also been impacted by two significant, technically challenging legacy projects which will now not be completed until the end of the year. The resulting cost overruns will have a material impact on the group’s profits this year.

Despite this, the implementation of their strategic objectives has allowed them to achieve some significant efficiency gains. The benefits have been reduced by the time taken to change the location and management in a facility in Canada which has now been completed.

As a consequence of the above developments, the board expects that whilst revenue for the full year will be in line with market expectations, the closing order book will be lower and profits are expected to be around £1.2M below current market expectations.