Pan African Resources is a mid-tier South African focused gold and platinum miner and explorer. They have three main segments. Barberton Mines is a low cost, high grade, greenstone belt producing operation with three gold mines which has contributed significantly to the group’s successful track record. The mine’s production capacity is 95K ounces of gold from underground and 20K ounces from the Tailings Retreatment Plant (BTRP) per annum. Evander Mines was acquired in 2013 and is another gold mine that has production capacity from underground operations of 95K ounces and 10K ounces from ETRP per annum. Phoenix Platinum is a tailings retreatment plant designed to extract 10K ounces of platinum group metals per annum from chrome tailings who sell platinum group metal concentrates to West Platinum, a subsidiary of Lonmin.

The Barberton Mines have resources of 9MT at 10.7g/t and 3M ounces along with reserves of 4.3MT at 10.1g/t and 1.4M ounces. The cash cost is $840 per ounce. The BTRP has resources of 20.4MT at a grade of 1.3g/t (900K ounces), and reserves of 13.4MT at 1.5g/t (600K ounces). The cash cost of the BTRP is $480 per ounce. The Evander mines has resources of 83.5MT at 9.7g/t and 25.9M ounces along with reserves of 28.8Mt at 8.5g/t representing 7.9M ounces with a cash cost rather higher at $1,291 per ounce. The ETRP has resources of 205.3MT at 0.3g/t representing 1.9M ounces along with 38.1MT at 0.3g/t representing 400K ounces with a cash cost of $688 per ounce. Phoenix Platinum has resources of 6MT at 3.1g/t representing 600K ounces along with reserves of 4.8MT at 3.2g/t representing 500K ounces with a cash cost of $578 per ounce.

The company has a dual listing, both on AIM and the JSE. The largest shareholding is Shanduka Resources with 23.83% and they are a black empowerment partner.

Pan African Resources has now released its final results for the year ended 2015.

Revenues decreased when compared to last year as a £1.2M growth in platinum sales was more than offset by a £7.9M fall in Barberton gold sales and a £6.8M decline in Evander gold sales. Salaries and wages decreased by £676K and engineering & technical services fell by £1.3M but most other costs were up with a £2.9M increase in gold processing costs, a £1.4M growth in gold mining costs and a £928K adverse movement in the inventory valuation adjustment which meant that gross profits decreased by £18.1M when compared to 2014. The director and share option expense fell by £830K and there was a £904K positive movement in the rehabilitation trust fund value which meant that the operating profit was some £16.2M below that of last time. Finance costs increased with a £486K growth in interest costs and a £1.1M increase in the rehabilitation provision interest but the tax charge declined by £3M which gave a profit for the year of £11.7M, a decline of £15.1M year on year.

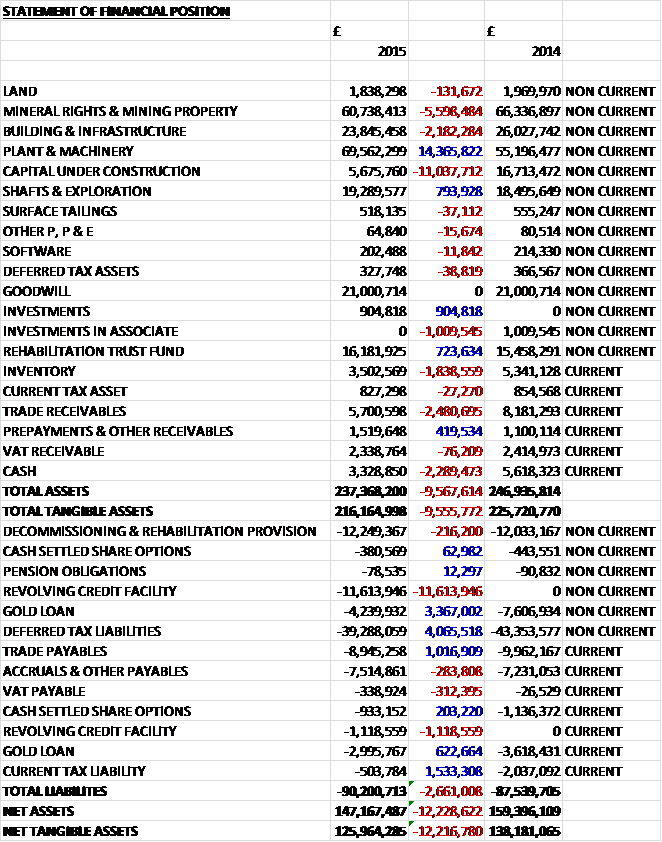

When compared to the end point of last year, total assets declined by £9.6M driven by an £11M fall in assets under construction, a £5.6M decline in the value of mineral rights and mining properties due to the depreciation of the Rand, a £2.5M decrease in trade receivables, a £2.3M fall in cash, a £2.2M decline in building infrastructure and a £1.8M decrease in inventory relating to a fall in mineral stocks and gold, partially offset by a £14.4M increase in the value of plant and machinery after some was transferred from assets under construction. Total liabilities increased during the year as a £12.7M increase in the revolving credit facility as partially offset by a £4M fall in the gold loan, a £4.1M decline in deferred tax liabilities and a £1.5M fall in current tax liabilities. The end result was a net tangible asset level of £126M, a decline of £12.2M year on year mainly relating to the depreciation of the rand.

Before movements in working capital, cash profits nearly halved to £25.3M. There was a modest inflow of cash from working capital and a fall in income tax was offset by an increase in royalties paid and finance costs to give a net cash from operations of £19.6M, a decline of £17.2M year on year. The group spent all of this cash on property, plant and equipment so after a £1M purchase of intangible assets was partially offset by the sale of an associate there was a cash outflow of £666K before financing. The group then took out more loans so it could pay the dividends of £14.3M so that there was a cash outflow of £2M for the year and a cash level of £3.3M at the year-end.

This year has been a challenging one for the gold industry as the gold price declined by 7% and the rise in US interest rates reduced the attractiveness of holding gold as an investment. Although the price of gold in Rand terms has not fallen so far, the country has been hit by inflationary pressures such as employee costs and energy that has contributed to eroding margins. The group also experienced some operational difficulties, mainly due to the Evander Mine’s low grade cycle continuing through most of the year and the impact of oil contamination at the Biox plant at Barberton mines which affected gold production. Going forward, however, the Evander mine grades have increased considerably as expected.

While the wide-spread labour unrest continues to pose significant risk to the industry in South Africa, the group are endeavouring to maintain good relationships with the unions and they did not experience significant labour disruptions at their operations during the year. The road ahead in the country’s labour environment remains challenging, however.

Overall the group’s total ounces of gold sold during the year was 175,857 ounces compared to 188,179 ounces last year and was below the planned annual production. With the strategic initiatives in place, the board anticipates achieving a target of about 215,000 ounces of gold and 10,000 ounces of platinum in 2016. In the longer term there is a significant undeveloped resource of over 30,000,000 ounces at Evander Mines. Capex was focused on the commissioning of the ETRP, capital development on Evander 25 level to gain access to the higher grade panels and ensuring the infrastructure of both gold operations was maintained.

The profit at the Barberton Mines was £18M, a decline of £5.6 when compared to last year. The total amount of gold sold by the mine decreased by 5.2% to 105,776 ounces and the cash cost per ounce increased by 2.4% to $758 per ounce. Excluding the BRTP, the amount of gold sold fell by 8.2% to 81,493 ounces. This was due to the BIOX plant oil contamination and operational safety stoppages enforced by the DMR. Operational and maintenance systems have been implemented to mitigate the risk of future oil contaminations and safety improvements.

Excluding the BTRP, the cash costs increased by 8% to $840 per ounce, and much more in Rand terms. This was exacerbated by the lower gold production and higher wages and engineering costs. The total all in cash cost per ounce fell by 1.9% to $916 per ounce, however, but this was entirely due to the weakening Rand and on local currency terms, the costs increased by 11.7%. The group received an average $1,212 per ounce compared to $1,309 last year with all-in costs of $916 per ounce.

Expansion capital of ZAR14.7M was spent on the development of the Fairview ventilation raise borehole project to improve operating environment conditions. New ore reserve and exploration drilling projects have yielded positive results, confirming the down dip extension of the high grade 11 Block of the MRC orebody by a further 170 metres. This extension to the MRC orebody has resulted in an annual increase in the mine’s mineral reserves by 236,162 ounces, thereby extending the life of mine to twenty years.

Looking ahead, the mine aims to improve levels of production by focusing on BIOX recoveries, increased tonnages aligned with their incentive system in conjunction with cost containment in order to avoid margin erosion. The management team also aims to reduce safety stoppages. Gold sold from the BTRP was 24,283 ounces, up from 22,885 ounces last year. Tonnes processed improved to 971,627 tonnes at a lower grade of 1.4g/t. The cash costs at the plant fell from $493 per ounce last year to $482 per ounce this year. Looking ahead, the Sheba and New Consort tailings dams will provide potential future sources of tailings which has supported the increased BTRP life of operation to 15 years. The plant payback period was 18 months since commissioning in July 2013 so the increase in the life of operation will result in further surplus free cash flows.

The loss at Evander Mines was £1.8M, an adverse movement of £6M when compared to 2014 due to the low grade cycle of the mine. The amount of gold sold decreased by 8.5%. Underground and surface sources tonnes milled decreased by 1.2% to 648,209 tonnes largely due to challenges related to underground mining operations and infrastructure constraints, power interruptions and safety stoppages. These issues adversely impacted production output but the mine has implemented corrective actions including improved maintenance protocols on the underground conveyor belt system, thereby improving availability of the conveyor belts from 60% to 80%. The mine also improved the monitoring and pump infrastructure of its No. 8 shaft de-wartering pumps, thereby reducing the risk of shaft flooding.

The total cost of production increased by 8.6% to ZAR999.3M which included additional cost in relation to the new ETRP plant and related surface feedstock, and excluding the ETRP costs, only increased by 2.7%. In dollar terms, the cash cost per ounce increased by 7.3% to $1,238 mainly as a result of the lower grade cycle. The group received an average of $1,216 per ounce compared to $1,295 last year and with an all-in cost of $1,515 per ounce, the problem at this mine is clear.

During the year the group commissioned its ETRP and the first gold was eluted in January 2015. The plant has now ramped up processing to its capacity of 180,000 to 200,000 tonnes per month at 0.3g/t of tailings and 1.1g/t of surface feedstock. Gold production from the plant was on target and its recoveries from tailings source are currently above plan at 48% while additional surface sources aided in increasing the ETRP overall recovery to 53.7%. The plant was operational for four months of the year and its cash costs amounted to $688 per ounce and contributed an additional 2,494 ounces of gold from its tailings sources and 4,029 ounces from surface feedstock. The total construction capital spend on the ETRP was about ZAR174.3M which was below the original ZAR200M project budget.

An internal technical team from the mine has been assigned to assess the merits of developing the Evander South project to the level of a preliminary economic assessment. This project is an opportunity whereby the Kimberley reef can potentially be exploited at shallow depths starting at 300 metres below the surface. Evander South has an estimated mineral resource of 4.9M ounces. In light of the positive results from the ETRP, the group will undertake a preliminary economic assessment on the viability of constructing a tailings retreatment plant at the mine which can potentially treat slimes at a processing capacity of up to 12MT per annum at a grade of 0.28g/t from the Winkelhaak, Leslie and Kinross tailings storage facilities.

The profit at Phoenix Platinum was £842K, a growth of £627K year on year. The amount sold increased by 42.2% to 10,245 ounces and overall plant recoveries increased significantly to 44%. The cessation of IFL’s operations at Skychrome, which mined mostly oxidised material and its replacement with sulphide material from its underground operation at Lesedi resulted in an improvement in the quality of feedstock being treated and this, in conjunction with the introduction of new re-agents in the metallurgical process were the main contributors to the higher recoveries.

The PGE basket price received decreased by 13.1% to $839 per ounce and the cash costs per ounce decreased by 22.5% to $578 per ounce. Looking ahead, Phoenix aims to optimise resources from Elandskraal and Kroondal to maintain production and profitability. In June they signed a new agreement to secure Platinum rights to the Elandskraal resource. The haulage contract to transport this material to the plant at Phoenix has been awarded and processing will start in September. During the coming year, the Elandskraal material will be batch treated in the CTRP to conduct re-agent suite test work. In 2016, 60,000 tonnes of the Kroondal resource will be processed in the CTRP and re-agent test work will be conducted on this material during the latter part of the year.

Electricity is the second largest cost contributor for the group, representing nearly 14% of the total cost of production. Their electricity increases in the current year amounted to 8.6% compared to the NRSA approved Eskom increase of 12.7%. Eskom’s most recent announcement alludes to potential increases of up to 25% in 2016 which will obviously have a material adverse effect on the total production costs if NERSA approves the increase.

During the year, the group appointed a new CEO – Cobus Loots was appointed in March 2015 having previously been finance director of the group and MD of Shanduka Resources.

The group has committed £10.4M to Oakleaf and Shanduka, upon completion of the conditions precedent to the purchase agreement, relating to the Uitkomst Colliery acquisition. The colliery is an existing operational mine and the acquisition is expected to be earnings and cash flow enhancing. It contains a coal mineral resource of 25.7MT, of which 22.1MT can be classed as measured or indicated and the area also has additional exploration potential. Current operations at the colliery demonstrate that it can readily produce yields of high grade coal suitable for export or local metallurgical markets and it currently sells about 400K tonnes of coal per annum. As well as being earnings enhancing, the exposure to coal provides a hedge against an anticipated increase in rising energy prices in South Africa.

In August the IFL announced that as a result of deteriorating business conditions in its South African subsidiary, International Ferro Metals SA has entered into business rescue, a statuary means of enabling a financially distressed company to continue business, under the supervision of a business rescue practitioner. This is relevant to the group because Phoenix Platinum is situated on the IFMSA property and a 20% portion of the feedstock for the operation is obtained from tailings arising from IFMSA’s current processing activities. They also source electricity, water and some other services form the business. At this stage, Phoenix is not in a position to fully assess the impact of these proceedings but they will work with IFMSA to ensure operations and interests of Phoenix are safeguarded.

The group has two main banking facilities. The new revolving credit facility is for ZAR800M at an interest rate of JIBOR (currently 6%) plus a 2.5% interest rate margin. The final payment date is June 2020 and the financial covenants include net debt : equity less than 1:1; interest cover ratio greater than four times; and the ratio of net debt to EBITDA must be less than 2.5:1. I have to say it is very refreshing to see the banking covenants spelled out so clearly, other companies can learn something from this (all of these covenants were comfortably met this year). Last year a gold loan transaction of ZAR200M was entered into with ABSA Bank, the purpose of which was to provide funds for the ETRP constructed at Evander mines. The loan is repaid quarterly in gold ounces produced from the operation with payments to end in October 2017.

Obviously the group is very susceptible to changes in the gold price with the other major sensitivity is the South Africa Rand exchange rate, both with the US dollar and Sterling. Finally, the borrowings are dependent on the interest rates in South Africa so there is susceptibility there too. Operationally the group has considerable country risk as it operates entirely in South Africa which is susceptible to industrial action and the occasional power interruption.

In the upcoming year, the Evander mine will experience higher grades and there will be a full year of production from the ETRP, as well as the Barberton mines returning to its previous production level. Notwithstanding the recent business rescue decision of IFL, Phoenix should continue to contribute cash flows and operating profit to the group and the Uitkomst Colliery acquisition should be finalised.

At the current share price the shares trade on a PE ratio of 17.3 and I can’t find a forecast for next year sadly. In light of market uncertainties the board has proposed a reduced dividend and at the current share price the shares have a dividend yield of 4.9%.

On the 26th November the group released a trading update. They expect interim EPS to be at least 10.37c per share which is an increase of 91% compared to the prior interim reported. The reasons for this increase include an improved operating performance from both Barberton and Evander Mines, as well as an increase in the Rand gold price during the first five months of the year. In Sterling terms, the EPS is expected to come in at 0.51p per share, an increase of 70% compared to last time.

The cash flows have been robust and good progress has been made in reducing debt. At present the net debt position is at ZAR70M compared to ZAR321M at the year-end, although dividend payments of ZAR210M are due in December.

Overall then this has been a difficult year for the group. Profits more than halved; net assets declined, mainly due to the depreciation of the Rand; and operating cash flow was down with no free cash generated. Obviously like all gold miners, the group has been hit by the weak price of the metal but this has been combined with increasing employee and energy costs along with the lower grade cycle at Evander and oil contamination of the BIOX plant in Barberton, which at least remained profitable unlike the Evander mine.

The Phoenix Platinum business performed well despite the decline in the price of the metal, due to higher quality feedstock. Unfortunately there is a cloud on the horizon here though with the announcement that the company that owns the site they are situated on has entered business rescue which will affect the feedstock and things like electricity supplies – there is no indication of the effect this will have on the business.

The mooted 25% increase in electricity prices is a real concern and perhaps explains why the group are expanding into coal mining – an area that is really under pressure at the moment. Going forward, the Evander mine is entering its high-grade cycle which, despite the price pressures should improve the profitability of the group this year and with a forward PE of 7.7 and dividend yield of 4.9% these shares look decent value – is it worth the risk though?

On the 8th February the group released another trading update. Overall, EPS is expected to come in at 0.57p for the half year period compared to 0.3p last time and up slightly from the 0.51p mentioned in the last update. The Barberton mines produced 56,447 ounces, an increase of 6.6% on the first half of last year; the Evander Mines produced 45,350 ounces, an increase of 34.4% but the Phoenix Platinum project produced just 4,493 ounces, down by 4.6%. There are pretty good numbers and the share price has shot up today but I can’t help thinking that I would like to see in the interims just how this is translating to cash flow, and have some updates on the Phoenix issue with their landlords and how the acquisition is progressing along with any electricity hikes.