RM has now released its final results for the year ended 2015.

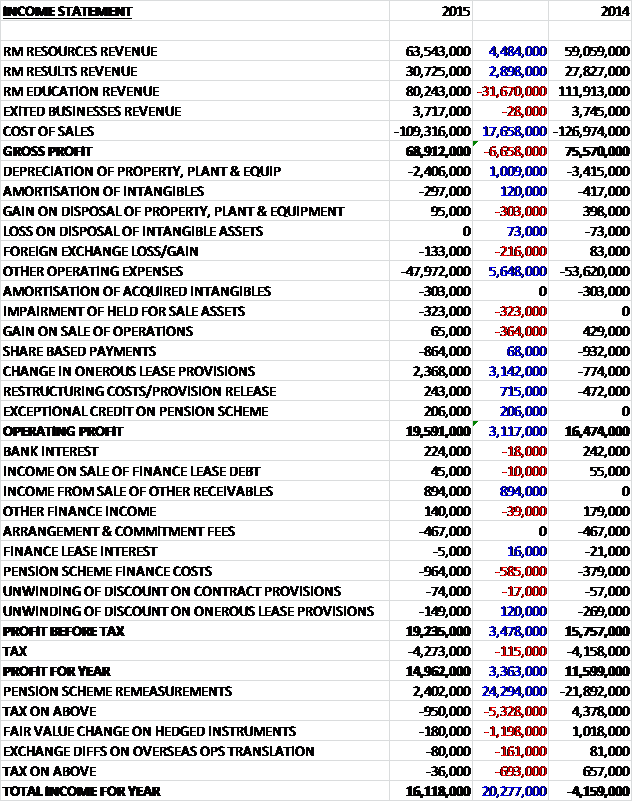

Revenues collapsed when compared to last year as a £4.5M growth in RM Resources revenue and a £2.9M increase in RM Results revenue was more than offset by a £31.7M fall in RM Education revenue. Cost of sales also fell but to a lesser degree than revenues so that gross profit fell by £6.6M when compared to 2014. Depreciation fell by £1M and other underlying operating expenses declined by £5.7M and this year also benefited from a 3.1M onerous lease provision release following the sublet of their old building, a £715K swing to a restructuring provision release and a £206K exceptional credit on the pension scheme which meant that the operating profit was £3.1M up on last time. The group also made £894K from the sale of some receivables which was partially offset by a £585K increase in the pension scheme finance costs and after tax payments were slightly higher, the profit for the year came in at £15M, an increase of £3.4M year on year.

When compared to the end point of last year, total assets decreased by £10.5M, driven by a £7.5M decline in trade receivables and a £2M fall in deferred tax assets, partially offset by a £1.2M growth in assets held for sale. Total liabilities also decreased during the year due to a £5.8M fall in long term contract balances, a £4.9M decline in the pension obligation, a £4.2M fall in provisions, helped by the £2.4M release of onerous lease provisions, a £3.4M decline in deferred income, a £1.5M decrease in accruals, a £1.3M fall in trade payables and a £1.3M decline in other payables. The end result is a net tangible asset level of £4.5M, an improvement of £11.5M year on year.

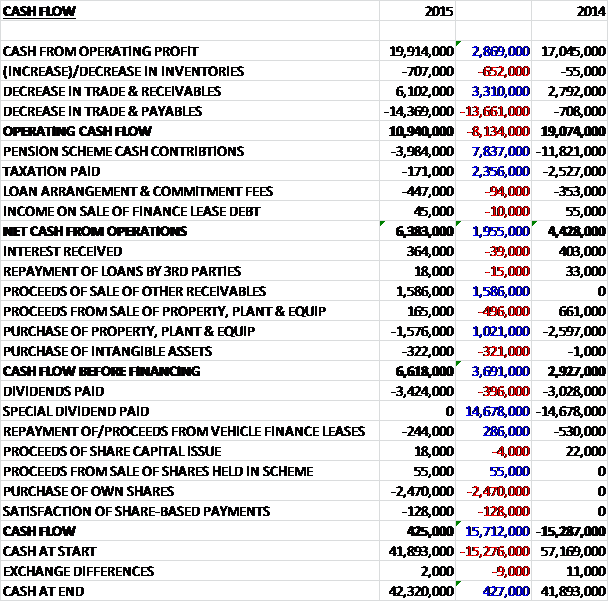

Before movements in working capital, cash profits increased by £2.9M to £19.9M. There was a big cash outflow from working capital, however, mainly due to a large fall in payables which is expected to continue next year too, but after a £7.8M fall in pension scheme contributions and a £2.4M decline in tax paid, the net cash from operations came in at £6.4M, a growth of £2M year on year. The group received £1.6M on the sale of “other receivables” which paid for the expenditure on property, plant and equipment so after a £322K purchase of intangible assets, there was a free cash flow of £6.6M. Of this, £3.4M went on dividends and £2.5M was spent on own share purchases to give a cash flow of £425K for the year and a cash level of £42.3M at the year-end.

Market conditions in the UK education sector will continue to be subdued as a result of increased pressure on school budgets.

The adjusted operating profit in the RM Resources division was £11.1M, a growth of £793K year on year on revenues that increased by 7.6% as the group gained market share in the UK and increased international revenues by 31.6%. Divisional revenue increased by 12.2% in the first half but only by 3.7% in the second half of the year as first half sales benefited from the curriculum changes that drove strong sales of new products.

At TTS UK Direct Marketing, revenues in the first half of the year were very strong, increasing by nearly 12% but in the second half, revenues fell by 2.9% reflecting tighter budgets within schools in the second half. The board expect the UK education resources market to continue to be subdued as a result of increased pressure on the discretionary element of school budgets and their focus will be on maintaining margins while looking to retain market position. At TSS International, revenues increased by 31.6% driven by growth in Europe and the Americas and included a large contract in the Middle East. The board expect international revenues to continue to grow in the coming year. At TTS UK Distributers, revenue from sales to UK trade partners decreased by 1.5% to £4.1M reflecting tightness of budgets in the wider UK education resources marketplace.

The adjusted operating profit in the RM Results division was £5.6M, an increase of £906K when compared to last year on revenues that grew 10.4% reflecting operating margins that increased from 16.7% to 18.1%. During the year the business secured a three year contract with the education charity AQA, the largest UK schools exam awarding body, to provide e-marketing services alongside the current provider.

Internationally the business is pursuing opportunities for the onscreen marking of paper-based exams as well as onscreen testing, often bidding with partner organisations. In the UK, exam and curricula changes introduced by the English Department for Education have significantly changed the phasing of exams so that the vast majority are taken in the summer term which has moved revenue phasing into the second half of the year (paving the way for a poor first half of 2016?) There is a long term trend from paper based to onscreen testing in the assessment market, though the adoption of such systems for school based examinations is low.

The educational data side of the business is heavily dependent on the Department for Education, principally through the National Pupil Database and RAISE Online contracts. These contracts include the capture and publishing of data for the school performance tables in England and both are up for retender over the next year. It is worth noting that the group have managed these contracts for over ten years, although of course that is no guarantee that they will retain the contracts. They are also in the process of exiting a number of other smaller data services and non-profit making contracts. The board are targeting the growth opportunities in e-assessment to more than outweigh reduced revenues in the educational data business, thereby allowing them to maintain good operating margins.

The adjusted operating profit in the RM Education division was £5.5M, a decline of £2.2M when compared to 2014. Market trends affecting this business include the demand from schools for solutions which are low-cost yet can cope with an increasingly diverse range of hardware and software. In addition, purchasing decisions in England have been increasingly devolved to schools and academy groups and away from central government and local authorities which has required a change in the way the division engages with its market and has resulted in an increased focus on the top couple of thousand customers.

As anticipated, the change of strategy away from selling hardware devices and a reduction in new school openings under the Building Schools for the Future scheme led to overall revenue in the division declining by 28% and the £2.2M fall in operating profit represents a broadly stable margin of 6.8%. The managed services offering is primarily the provision of full IT outsourcing services to schools and colleges and as anticipated revenues this year again declined with a reduction in new school openings under the BSF programme. Managed Services revenues decreased by 35.5% to £32.2M but the retention rates of existing customers increased significantly to 80% and 44 new schools signed managed services contracts in the year.

Digital platforms revenue increased by 1.4% to £7.7M. Revenue from RM Integris increased following good market share gains including over 350 schools in Derbyshire. The strategy is to increase market share by focusing on the cloud-based platform, competitive price point and investing to develop the product’s relevance in a market dominated by a large competitor, and with low levels of supplier churn. RM Unify is a technology platform to allow customers easy access to the varied digital, cloud-based, educational specific content and materials that are now available online and during the year the Scottish government chose to extend its contract to (providing the product to all schools in Scotland) by another two years to January 2018.

Infrastructure includes the tools, products and services to help schools manage their own IT.

Revenues in the business declined by 25.8% to £40.3M as the group continue to transition from manufacturing their own PC client devices and associated warranties and installations and move to a more technology agnostic service and support provider.

In March the group’s interests in Newham Learning Partnership were sold for £1.6M which generated a profit of £900K which I assume relates to the sale of “other” receivables on the income statement. In May their Milton Park leased premises were sub-let to South Oxfordshire District Council for a minimum period of three years. On sub-letting, some £2.4M was released from the onerous lease provision. At the end of the year, SpaceKraft was identified for disposal and was sold in December. As the group failed to realise the net book value of the business, an impairment of £233K was recognised on its intangible assets and property, plant and equipment.

One key risk for the group is the pension scheme. The deficit did fall from £26.8M last year to £21.9M this year, however. This reduction resulted from the reduction in liabilities due to beneficial membership experience over the three year valuation period, better than assumed returns on the scheme assets and the shortfall contributions paid by the company which has been partially offset by the change in mortality assumptions and a reduction in the inflation risk premium. In December, after the year-end, agreement was reached with the trustees with regards the triennial valuation where the deficit was agreed at £41.8M. The deficit recovery plan comprises an initial cash contribution of £4M into the scheme and £4M into the escrow account together with deficit recovery payments remaining at £3.6M per annum until 2024 so this is going to be a drag for some time.

Another major risk is public policy as the majority of the businesses are funded from UK governmental sources and in a related risk, the group is dependent on a small number of key contracts with government, local authorities and exam boards.

At the current share price the shares trade on a PE ratio of 9.1 which is expected to remain the same on next year’s consensus forecast. After a 25% increase in the normal dividend, the shares are yielding 3.5% which increases to 4.2% on next year’s forecast.

Overall then, this year gone has been a fairly decent period for the group. Profits were up, although this was due to the onerous lease provision release following the sub-letting of a building; and the sale of some receivables so underlying profits actually fell somewhat. Net assets did increase, however, and the balance sheet now looks much better with a positive tangible book value. The operating cash flow improved as a reduced payment to the pension scheme offset a large fall in payables and the cash profits increased and a decent amount of free cash was produced.

Operationally, RM Results performed well but it looks like revenues will be more second half weighted going forward and the league table data contract is out to tender which is a potential risk. The RM Resources business also performed well due to curriculum changes in the first half of the year driving increased sales – unfortunately the second half was much poorer and the market going forward looks subdued. RM Education performed badly as the group continued to move away from hardware sales and fewer new schools were opened.

With a forward PE of 9.1 and dividend yield of 4.2%, the shares look cheap but it seems the business is going to find going much toucher in 2016 and I feel there is scope for a profit warning if things don’t go so well. The repaired balance sheet does make this more investible now but I would like to see some evidence that the first half of 2016 isn’t going to be too bad before buying.

On the 12th February the group announced that CFO Neil Martin purchased 35,000 shares at a value of £47K which represents his maiden share purchase.

On the 23rd March the group released a trading statement where they stated that the UK market for educational products and services remained subdued. Trading in Q1 has been in line with the board’s expectations and cash levels at the end of February were £34.4M after an £8M cash payment into the pension scheme as agreed at the latest triennial valuation.