Sylvania Platinum have now released their interim results for the year ending 2019.

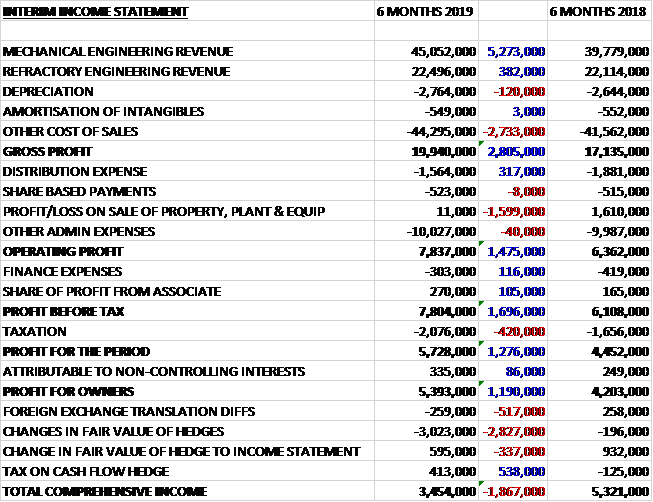

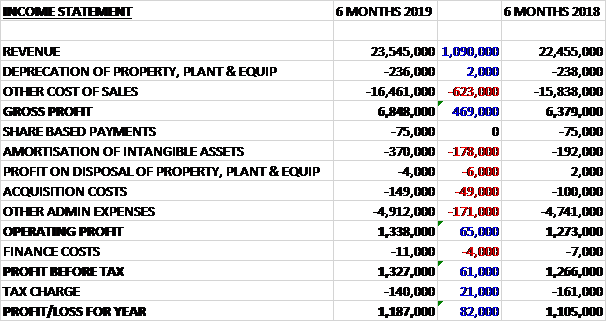

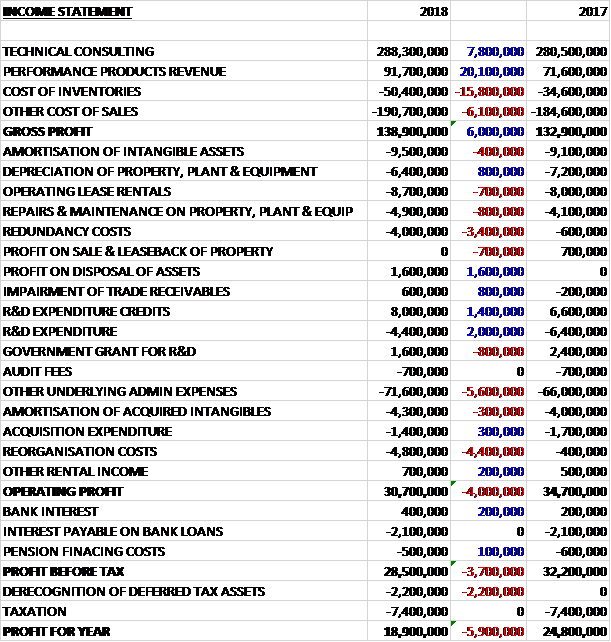

Revenues increased by $3.9M and after cost of sales was up $2.2M, including a £493K increase in depreciation the gross profit grew by $1.7M. General and admin costs grew by $226K but other income was up $29K and the operating profit was $1.5M higher. Finance income was down $46K and finance costs were up $45K but the tax charge reduced by $137K to give a profit for the period of $7M, a growth of £1.6M year on year.

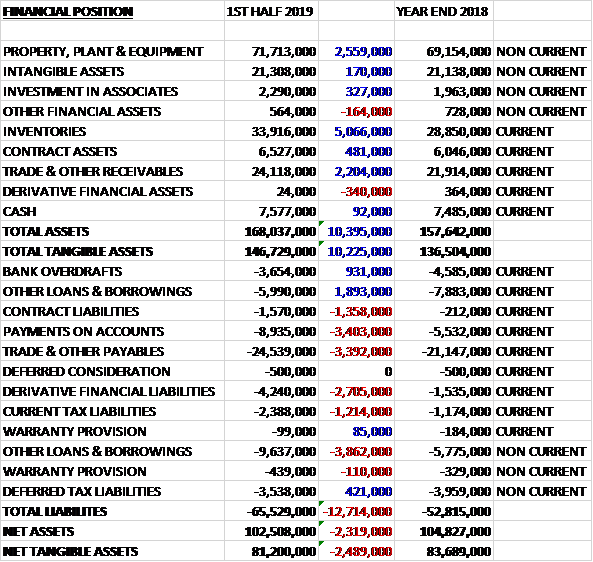

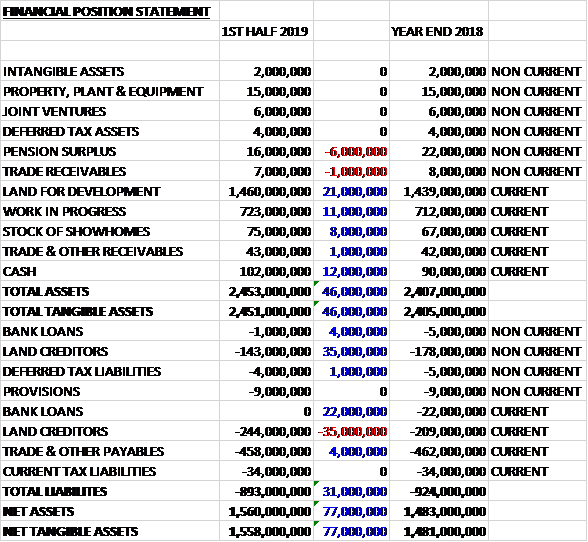

When compared to the end point of last year total assets declined by $405K driven by a $14.5M decrease in receivables, a $6M decline in property, plant & equipment, a $1.3M decrease in exploration and evaluation assets, a $573K fall in loans to Ironveld and a $571K elimination of the rehabilitation guarantee investment, partially offset by a $14.1M growth in contract assets, a $7.6M increase in cash and a $922K increase in loans receivable. Total liabilities have declined during the period due to a $1.7M fall in deferred tax liabilities. The end result was a net tangible asset level of $57.5M, a growth of $2.7M over the past six months.

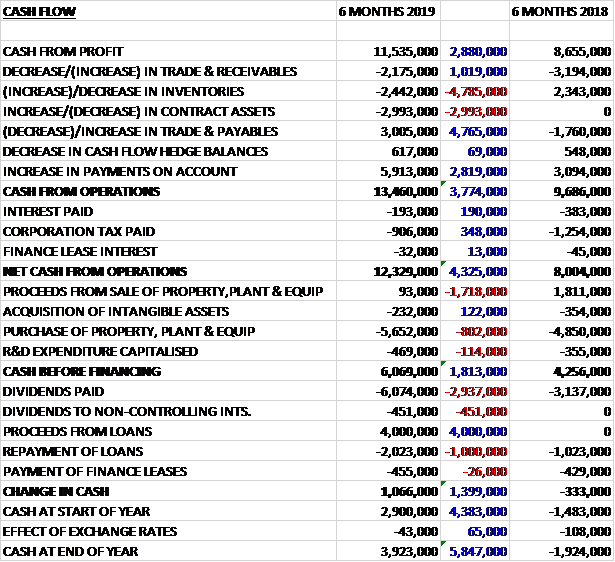

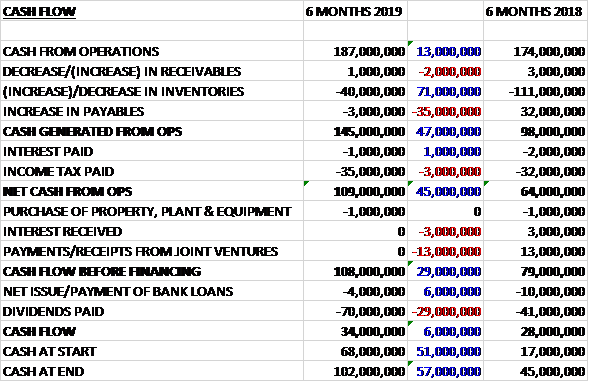

Before movements in working capital, cash profits increased by $6M to $14.1M. Tax payments increased by $1.1M to give a net cash from operations of $11.9M, a growth of $4.8M year on year. The group received $692K as a refund for rehabilitation insurance but spent $3.7M on property, plant and equipment to give a free cash flow of $8.5M, an improvement of $11.1M year on year. They then spent $1.3M on dividends and $120K on their own shares to give a cash flow of $7M and a cash level of $20.2M at the period-end.

The SDO achieved 34,045 ounces for the first half of the year under very difficult operating circumstances. This was a slight improvement on the 33,892 ounces in the same period of last year. The operational challenges experienced in Q2 had a direct impact on ounce production resulting in al lower than expected production performance.

The Lesedi operation experienced significant downtime during November and December due to water shortages in the area, resulting in the plant only being able to treat 52% of its planned treatment tonnage in Q2. In addition, Doornbosch’s dump re-mining, where the current dump is reaching its end of life, experienced significant downtime and feed instability that impacted negatively on plant throughput and recovery efficiencies. Other contributors to lower than planned PGM production for the period were the lower percentage of fresh arisings feed received from the host mines at both Tweefontein and Millsell during the last quarter, following safety stoppages related to underground incidents external to the group’s operations, as well as oil contaminated feed material impacting on recoveries in Q1 at Mooinooi.

Cash costs per ounce increased by 16%, primarily as a result of Lesedi’s larger contribution of PGM ounces which remains higher cost than the other operations. The unit cost was particularly high though due to low PGM production brought about by the water shortages. Additional re-mining cost at Doornbosch related to the re-mining challenges on the current dump. With most of the challenges now resolved and mitigation measures implemented, it is expected that cash costs will improve in line with the forecast increased ounce production in H2 2019. In USD terms, this increase in cash costs was limited to 10% as a result of the weaker ZAR exchange rate. Cost saving initiatives continue at Lesedi and the cost per ounce is expected to reduce going forward as Project Echo and optimisation project ounces come on stream in the second half of the year

The gross basket price was $1,201 per ounce compared to $1,057 per ounce in the first half of last year. Although the price of platinum dropped, the steady increase of both Palladium and Rhodium has had a favourable impact on the basket price. Revenue from by-products increased by $1.4M from the comparative period in the prior year. Ruthenium increased from an average for the period of $98 per ounce to $262 per ounce and Iridium increased from $969 to $1,452 per ounce.

The project Echo MF2 modules are progressing well with the Millsell and Doornbosch modules in operation since early 2018 and Mooinooi module under construction and expected to be commissioned during the last quarter of the year. Doornbosch MF2 performed according to design since commissioning, but Millsell was performing below design and had some initial challenges related to new fines flotation technology which was only resolved with the retrofit and commissioning of new high intensity flotation mechanisms in the circuit towards the end of 2018. The plants at both operations are expected to deliver to full potential going forward.

The Tweefontein MF2 is still delayed due to the constraints on the national power utility’s electricity supply infrastructure to the Tweefontein mining complex. The upgrade by the power utility has started but the completion date is currently undetermined. The Lesedi chrome plant project, comprising of the dismantling and relocation of the redundant Steelpoort chrome circuit, has commenced and is expected to be completed in the second half of the year. This will enable chrome removal ahead of Lesedi’s PGM plant, aligned with the standard SDO operating model employed at existing operations in the group and will contribute towards higher PGM feed grades and ounce production at the operation.

During the period monthly instalments of R222K were paid to the investment linked to the rehabilitation insurance guarantee. These guarantees have been moved to a new facility and the investment was withdrawn and the account closed. The investment is no longer required as the method of funding the rehabilitation has changed. The balance of the funds were transferred to the company in January.

Going forward, management have taken corrective action and implemented various improvement measures to address challenges experienced during the period in order to mitigate the impact and to ensure that planned production targets are met for the remainder of the year. Although the SDO team is looking for alternatives to compensate for H1 losses in the second half, they have revised the current PGM production guidance for 2019 to between 73K and 76K ounces.

At the current share price the shares are trading on a PE ratio of 9.1 which falls to 5.5 on the full year consensus forecast. The shares are yielding 1.3% which increases to 2.9% on the full year forecast.

Overall then, operationally this has been a very difficult period but this has not translated over to financial performance with profits up, net assets increasing and the operating cash flow improving with plenty of free cash being generated. Production was slightly up but the performance seems to have been down to the rise in the basket price for PGM products with the more minor products all increasing to more than offset the weak price of platinum.

Lesedi has struggled with continued high costs and water shortages, and it doesn’t seem as though these have been fully sorted yet. Doornosch is also struggling with feed instability at the end of life dump and both Tweefontein and Millsell have suffered lower arisings due to safety stoppages. This has caused production guidance to be lowered for the year. Despite this the shares are still looking decent value with a forward PE of 5.5 and yield of 2.9%. I continue to hold as long as the basket price remains favourable.

On the 29th April the group released a trading update covering Q3. They delivered 16,256 ounces for the quarter, a 9% increase on Q2’s total. This was due to a 7% improvement in feed tonnes and a 3% increase in recovery efficiencies with the feed grade at similar levels. The total cash costs decreased by 4% in ZAR terms and 1% in USD terms to $599 per ounce. The capex decreased by 21%, aligned to the forecast project Echo schedule.

The drought conditions continued to impact water availability to the Western operations, particularly Lesedi. Measures to mitigate the impact such as additional boreholes and water transfer from neighbouring operations have helped improve supply but Lesedi still experienced significant downtime during the quarter. The final upgrades to the water supply system were completed in March and the plant has since been running with limited downtime.

Management continued to focus on the Doornbosch re-mining operation at the current dump, which is at the end of its life. This improved PGM feed tonnes but the significantly lower than planned current arisings from the host mine still negatively impacted the feed grade. The overall chrome mining and treatment rate of the host mine did not deteriorate but the specific ratio of current arisings to other products reduced which led management to investigate and implement process improvements at the host mine operation. As a result, since March, current arisings tonnes and feed graded have been improving.

Optimisation of the enhanced process circuit modifications that utilise improved fine screening technology needed for more efficient upgrading of PGMs at Doornbosch, Millsell and Tweefontein was commissioned during the previous quarter and will help improve grades and ounce production.

The Mooinooi module which is part of Project Echo was commissioned earlier than planned, in March. It is currently being optimised and is expected to boost PGM ounces from Q4. The construction of the Lesedi chrome plant project is progressing well and is on track to be completed in H2. This will enable chrome removal at Lesidi’s PGM plant in line with the standard SDO operating model.

The higher basket price coupled with the increase in ounce production meant that there was a net revenue increase of 23% to $18.3M. The basked price improved 15% to $1,383 per ounce due to the continued upward trend of Palladium and Rhodium. Total operating costs increased 6% in ZAR terms mainly due to the increase in electricity costs following a rebate received from the host mine last quarter and planned transport to costs to transport dump material to the Lannex operation. Group cash costs decreased 2% to $624 per ounce due to the higher ounce production. All in sustaining costs decreased 8% to $756 per ounce.

EBITDA increased 55% to $8.2M due to the higher production and basket price. The group cash balance increased by $3.5M to $23.7M.

The board are forecasting 21,800 ounces for Q4, up marginally on Q4 last year provided there are no unforeseen disruptions. They are revising their production guidance to 72,000 ounces for the year which would mean record production being attained in Q4. With Mooinooi MF2 now added, grade improvement at Doornbosch and more consistent production at Lesedi, this should be achievable.

On the 31st July the group released a trading update covering Q4. The SDO delivered a record 21,789 ounces for the quarter, a 34% increase on Q3. This increase was due to a 10% improvement in feed tonnes and a 12% improvement in recovery efficiencies as well as a 9% increase in the feed grade.

Improved running times as Lasedi which experienced less water shortages than in the previous quarter, and increased and more stable re-mining performance at Doorbosch in particular assisted to increase the PGM feed tonnes for the period. The feed grade was assisted by improved current arisings and ROM fines at operations after Q3 saw fresh feed sources being impacted by the host mines operating schedule after the Christmas break. Higher grade feed material was also treated at both Lannex and Lesedi.

The improvement in the PGM recovery efficiency can be attributed to a more stable feed into operations at Lesedi and Doornbosch as well as the improved efficiencies associated with the commissioning of the MF2 module at Mooinoi in May and June, as well as better quality feed material being used at Lannex since May.

The total SDO cash costs decreased 17% in ZAR Terms and 19% in USD terms to $485 per ounce.

Based on challenges experienced with the water shortages at Lesedi during the past year and re-mining challenges at Doornbosch where the current dump reached its end of life in Q3, significant management focus went into exploring and implementing alternative measures to supplement water to operations and to optimise the current re-mining strategy for historical dumps.

Although minimal disruptions were experienced during Q4 due to water shortages, water availability at certain operations remains a concern and an ongoing focus area. While the water supply system to Lesedi has already been upgraded, more boreholes are being drilled in consultation with experts and process options are being explored to minimise consumption.

With the third project Echo MF2 module now commissioned at Mooinooi and the new chrome beneficiation circuit commissioned at Lesedi the respective management teams will now focus on optimising these circuits to unlock the full potential of these projects going forward.

The Mooinooi MF2 module will assist to further improve PGM recovery efficiencies while the Lesedi chrome plant project, utilising the dismantled and relocated chrome circuit from the old Steelpoort operation will enable chrome removal at Lesedi’s PGM plant. The circuit will enable the operation to have more flexibility and will contribute towards higher PGM feed grades and ounce production.

Revenue for the quarter increased 10% to $20.2M mainly due to the increase in ounces produced, offset by a 4% drop in the basket price to $1,328 per ounce. Total operating costs increased 10% as higher production resulted in higher lab costs and concentrate transport costs. Transport costs at Lannex increased due to the change in feed source and the annual electricity increase. Group EBITDA increased 14% to $9.3M but net profit decreased 2% to $4.8M due to a higher amount of income tax paid in South Africa. Cash balances were $21.8M, a $1.9M decrease.