Safestyle have now released their final results for the year ended 2018.

Revenues declined by £42.1M when compared to last year and after cost of sales also fell the gross profit was £25.5M lower. There was a £795K reversal of share based payments but restructuring costs were up £587K, there were litigation costs of £1.9M, fines of £1.1M, onerous leases of £294K, commercial agreement costs of £1.3M, non-recurring pay awards of £635K and a dilapidation provision of £618K so despite other operating expenses reducing by £1.4M there was a £30M negative swing to an operating loss. Finance costs increased by £132K but there was a £6M favourable swing to a tax income so the loss for the year came in at £13.3M, a detrimental movement of £24.1M year on year.

When compared to the end point of last year, total assets declined by £1.6M driven by a £6.8M decrease in cash, partially offset by a £2.3M growth in current tax assets and a £2.2M increase in the commercial agreement “asset”. Total liabilities also increased due to a £2.4M growth in trade payables, a £3.9M increase in borrowings, a £2.3M increase in accruals and deferred income and a £1M growth in the commercial agreement provision. The end result was a net tangible asset level of £4.7M, a decline of £14.1M year on year.

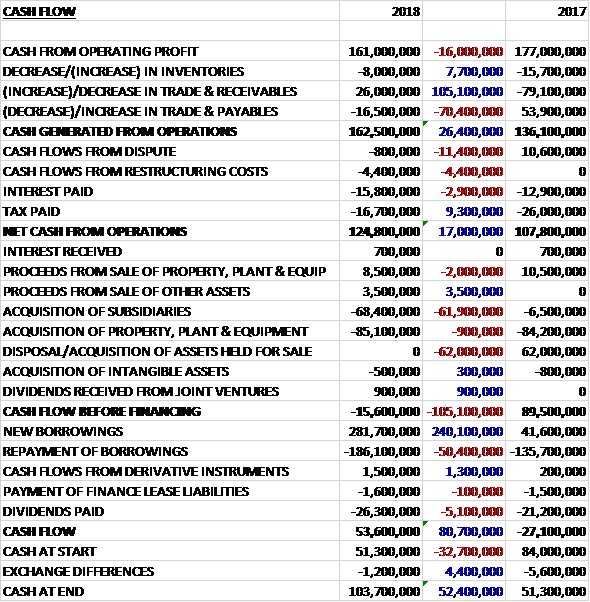

Before movements in working capital, there was a £27.6M detrimental shift to cash losses of £12.1M. There was a cash inflow from working capital due to an increase in payables and tax payments reduced by £2.1M to give a net cash outflow from operations of £8.8M, a detrimental movement of £20.6M. The spent £1M on tangible assets and £855K on intangibles which meant there was a cash outflow of £10.7M before financing. New borrowings of £3.9M gave a cash outflow of £6.8M for the year and a cash level of £4.2M at the year-end.

After 13 years of market share gains, the group’s market share fell from 10.7% to 8.2% this year. This reflected a 28% drop in installations to 42,995 although they were able to increase their average frame sales price by 6% to £646 as a result of price actions and a larger mix of higher average priced composite guard doors, and their average installed order value by 3% to £3,319.

Leads generated from direct response media increased by 2.8% but leads from other sources fell by 60% due to the actions of NIAMAC. In the last two months of the year, following the recovery of the workforce, the group experienced a marked improvement in lead generation with total leads only 4% lower than in the same period last year.

As well as the reduced volumes, the decrease in gross profit was also affected by an increased usage of traditional scaffolding solutions to ensure the teams are working safely; the change of mix generated via direct response media drove an adverse cost per order effect. This mix effect was compounded in 2018 by a significant year on year increase in Pay Per Click rates which were driven by increased online competition. Agent commission costs increased in the year, driven by the more competitive recruitment environment.

Much of the year was severely impacted by the activities of an aggressive new entrant, NIAMAC, which affected all areas of the group’s operations and resulted in them taking legal action to protect themselves in May. This, combined with a backdrop of a challenging consumer environment resulted in a severe decline in their financial performance in the year. The group settled its legal action in September and subsequently entered into a commercial agreement which led to a recovery in the contracted workforce across their canvass, sales, surveying and installations operations at the start of November.

The group invested significantly in lead generation, commissions and associated overheads prior to the end of the year. This occurred too late in the year to improve 2018s financial performance, however. Sales order intake for the final two months saw a step change in performance though.

The commercial agreement with Mr. Misra encompasses a five year non-compete agreement and the provision of services by Mr. Misra in support of the continued recovery of the group. They agreed a consideration with him subject to the satisfaction of both clear performance conditions by him and the group’s trading performance in 2019. The consideration will take the form of an allotment by the group of four million shares and a cash consideration of up to £2M, to be made in Q4 2020.

Due to the issues this year there has been large changes to the structure of the board. Mike Gallacher was appointed CEO, Alan Lovell was appointed Chairman, Rob Neale was appointed CFO, Fiona Goldsmith joined as a non-executive director and Julia Porter jointed as non-executive director.

Since late 2017 the business has changed its approach to managing health and safety with significant investment in additional resource, new processes, training and equipment. Their prime focus has been on working at height. This followed a working at height incident with one of their staff in 2017 for which they received a significant fine from HSE in 2018.

During the year West Yorkshire trading standards took the group to court over a number of incidents. As a result of this, the new business leadership team has put in place a comprehensive series of actions while aiming to establish and effective collaborative partnership with WYTS. Good progress has been made so far.

At the start of 2018 the first phase of the Electronic Lead Generation project was launched. In August, the second phase, Electronic Contract, was put in place. Before these changes, all their self-employed sales reps carried paper price lists and entered orders onto forms which were faxed to head office every day. They have now been equipped with a tablet with a sales process that ensures quick and accurate pricing and an immediate digital contract submission process. The programme has enabled simplification and delivered some cost savings and is a rich source of management information.

There were a number of non-recurring items this year. As part of a review by management of provisions made for the group’s future obligations, a revision to the estimates used for future product guarantee claims has been made which they consider more accurately reflects their obligations which led to a charge of £801K. Litigation costs of £1.9M are expenses incurred as a result of the NIAMAC litigation, predominantly legal advisor’s fees. Restructuring costs of £1.2M included redundancy payments as a result of the changes made to reduce the cost structure of the business.

Fines of £1.1M relate to the HSE and WYTS fines and related legal representation fees. Onerous leases of £294K represent an accrual for all rental costs up to the first lease break data for properties that were closes during the year. Commercial agreement costs of £311K are expenses incurred in securing the commercial agreement such as legal advisor fees and a set of one-off payments made as part of the contractual terms of the final agreement. The Commercial Agreement service fee of £1M is the assessed fair value of the consideration payable under the terms of the commercial agreement that has been attributed to services received in the year.

Non-recurring pay wards of £635K relate to the bonus payments made to executives reflecting the supplementary duties undertaken in a period of significant disruption and reward delivery of key actions required to secure and stabilise the business and are not linked to profit performance. The accounting policy for providing for exit obligations on leased property, principally dilapidations, has also been assessed in the year. Management concluded that a provision is appropriate based on new circumstances during the year which led to a charge of £618.

Going forward, the momentum generated by an improvement in sales order intake in the last two months of 2018 following the recovery in the group’s contracted workforce numbers has continued into the first part of 2019. The board expects to return to profitability in 2019 and to generate positive cashflow. Whilst aware of the broader macroeconomic uncertainty surrounding Brexit, 2019 represents a year of turnaround as opposed to an immediate return to their historical levels of financial performance.

No dividend was paid during the year or is being recommended but the shares are yielding 0.4% on the forecast for next year. The shares are loss making so there is no PE ratio of this year but on next year’s consensus forecast they are trading on a PE ratio of 21.7. At the year-end the group had a net cash position of £260K compared to £11M at the end of last year.

Overall then this year has been a bit of a disaster for the group. They made losses, the net asset level deteriorated considerably and there was an operating cash outflow. The main issue has been the NIAMAC problems but the group has also had health and safety fines to contend with. It is quite hard to determine the health of the underlying market. The NIAMAC issues seem to be mostly resolved, albeit with a rather costly commercial agreement to stop them competing. Aside from this, we also have Brexit approaching with the potential knock on effect on consumer spending. This is a turnaround year apparently which explains the expensive looking forward PE of 21.7.

Not sure what to do here, this could be a good entry point but there is a lot of uncertainty surrounding the company.

On the 16th May the group released a trading statement. Phase 2 of the turnaround plan is now well underway. The focus continues to be on recovering volumes and market share, restoring operational effectiveness, reducing costs and enhancing margins. They remain on track to finish this by the end of the year.

During the first four months of the year, the business has continued to rebuild its order book and the board expects revenue to grow by 10% against H1 2018, accelerating towards 20% in the second half. While elements of consumer demand appear to be soft, the market has seen volume growth in the first four months of the year of 2.7% with the group growing at more than twice that.

Progress has also been made on the gross margin and the board expects the first half margin performance to have improved by 4.5% which is expected to continue towards the second half. Despite the progress, margin improvement has been slower than expected, impacted by higher lead generation costs and the pace of recovery in improving the group’s operational effectiveness. Therefore, despite forecasting a small profit this year, the board does expect profit to be below current market expectations.

On the 26th July the group released a trading update covering the first half of the year. Management has continued to make progress on Phase Two of the turnaround plan. As expected, the first half of the year will result in a small loss, but despite a challenging market where consumer demand appears soft, the group remains on track to deliver a small profit for the year in line with current market expectations.

Revenues in the first half will be around 6.4% higher year on year with May and June being 15% higher. FENSA installation stats for the first half indicate that the market has declined in volume by 8.2%. The group continues to improve margins and the board expects a significant reduction in overheads against last year. The full year net cash position should be around £300K.