Waterman provides engineering and environmental consultancy advice to the property and infrastructure markets. They operate in two business segments: property and infrastructure & environment. The Property segment encompasses the UK Structures and Building Services businesses which are involved in development projects both in public and private sectors. In addition, this segment includes the overseas business in Australia, which is partly owned by the group, Ireland and Poland which are solely involved in the engineering design of buildings. The group also operate an outsourcing office in India which solely provides draughting services for the UK structures team.

In Australia the group have businesses in Melbourne and Sydney with a 51% ownership of the business in Melbourne and a 100% ownership of the Sydney business. The Australian operation primarily provides building services consultancy advice to the public and private sectors. The majority of the revenue is generated from healthcare, educations, prisons, residential, technology and bank fit out markets.

The group has a number of long term contracts that span more than one year. In calculating revenue, the percentage of completion method is used, based on a review of contract progress and the proportion of contract work completed in relation to the total contract works. Profits are only recognised where they can be reliably measured, which is normally after the contract has reached 40% completion. Contract costs comprise direct labour, direct expenses and attributable overheads. Gross amounts due from customers are stated at the value of the costs incurred plus recognised profits less recognised losses where they exceed progress billings. Progress billings not yet paid by customers are included within receivables. To the extent that progress billings exceed costs incurred plus recognised profits they are included in payables as amounts due to customers on long term contracts.

Waterman has now released its final results for the year ended 2015.

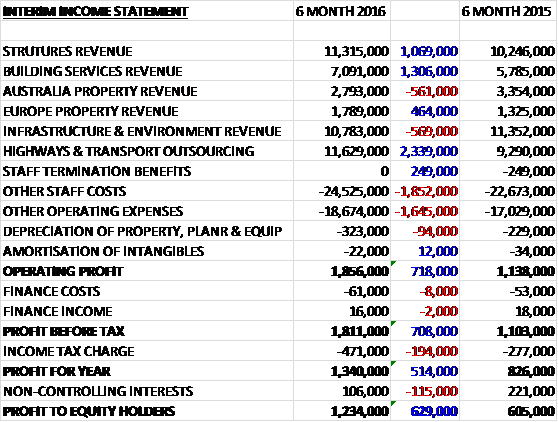

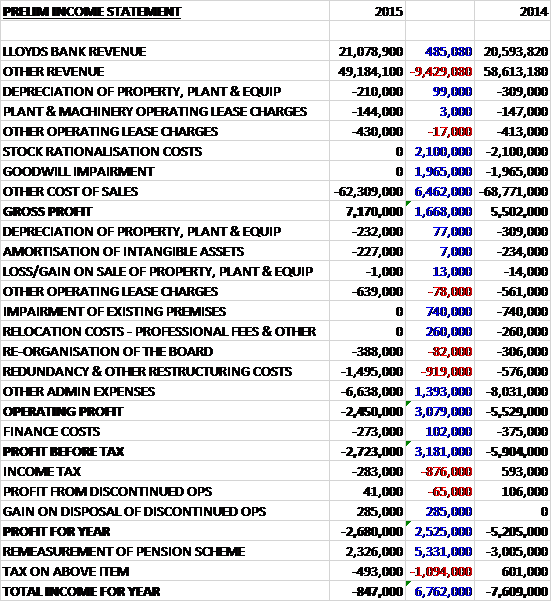

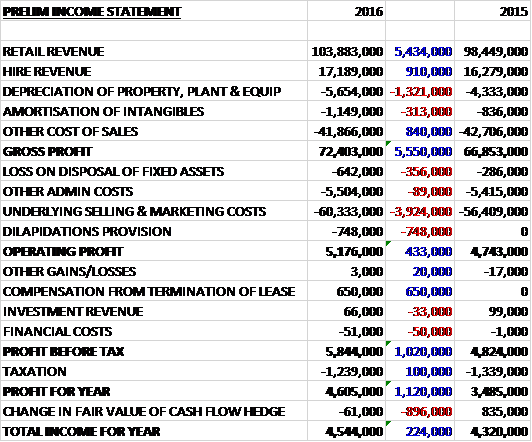

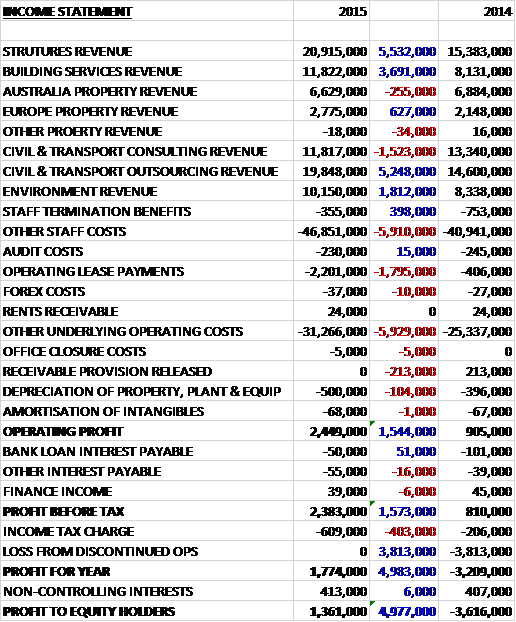

Revenue increased when compared to last year as a £1.5M fall in civil and transport consulting revenue and a £255K decline in Australia property revenue was more than offset by a £5.2M growth in civil and transport outsourcing revenue, a £5.5M increase in structures revenue and a £3.7M growth in building services revenue. Underlying staff costs increased by £5.9M and operating lease payments were up £1.8M with other underlying operating costs increasing by £5.9M which meant that after the lack of released provisions which were £213K last year and a £104K increase in depreciation, the operating profit increased by £1.5M when compared to 2014. There were negligible changes in the finance costs but tax costs were up £403K and there was no loss from discontinued operations which cost £3.8M last year so the profit for the year came in at £1.4M, a positive movement of £5M year on year.

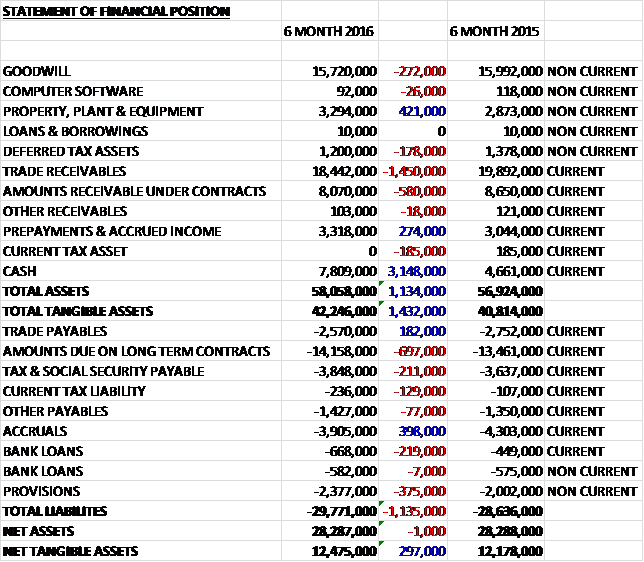

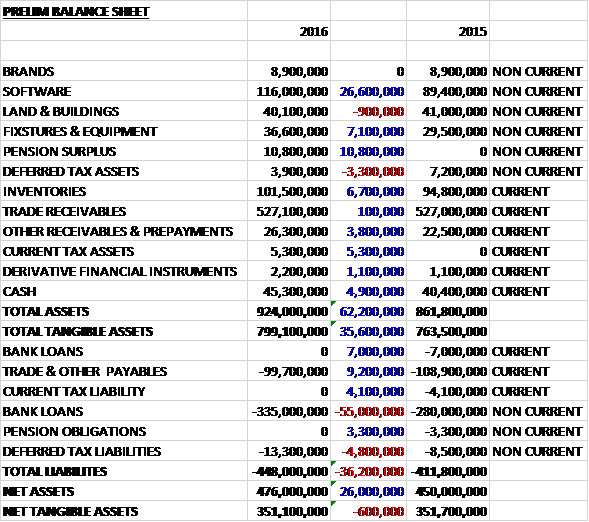

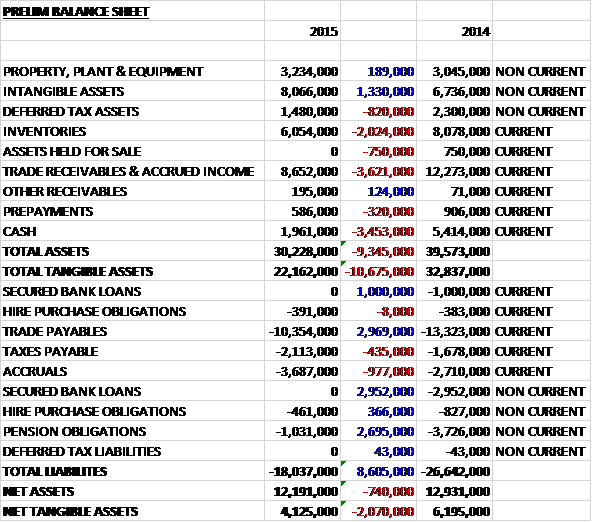

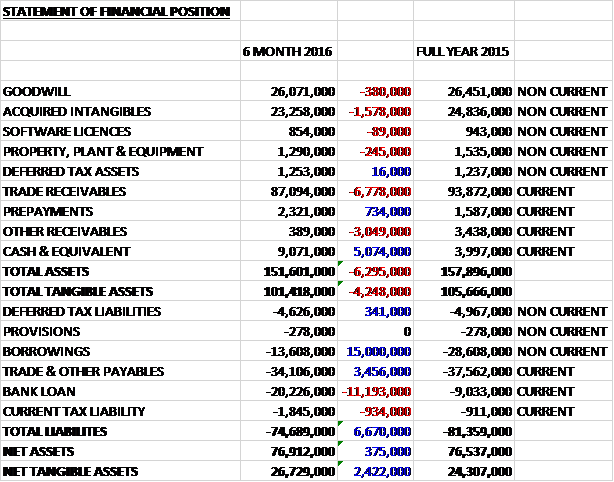

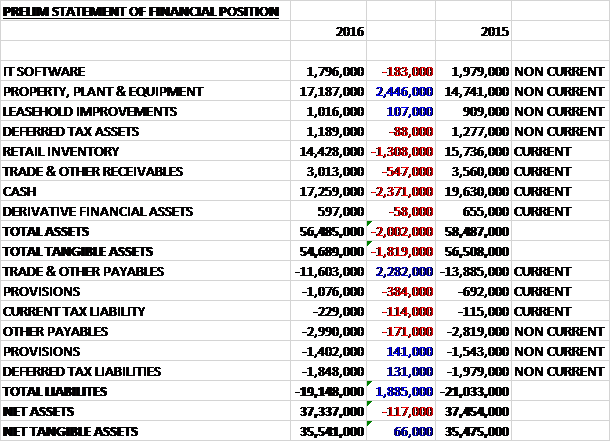

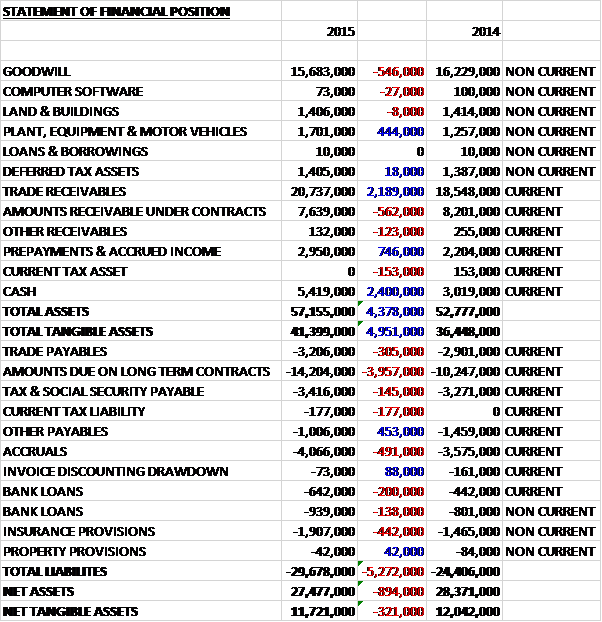

When compared to the end point of last year, total assets increased by £4.4M driven by a £2.4M growth in cash, a £2.2M increase in trade receivables and a £746K growth in prepayments and accrued income, partially offset by a £546K decline in goodwill and a £562K fall in amounts receivable under contracts. Total liabilities also increased during the year as a £4M growth in amounts due on long term contracts, a £491K increase in accruals and a £442K growth in insurance provisions were partially offset by a £453K fall in other payables. The end result was a net tangible asset level of £11.7M, a decline of £321K year on year.

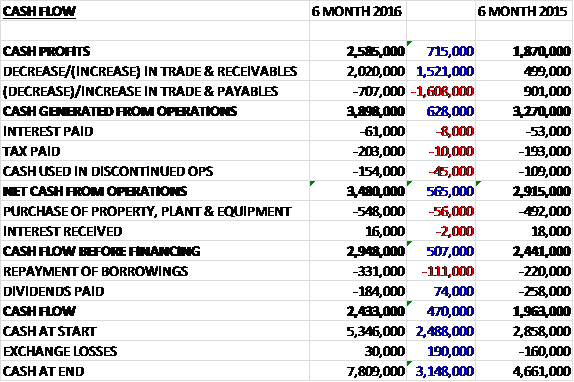

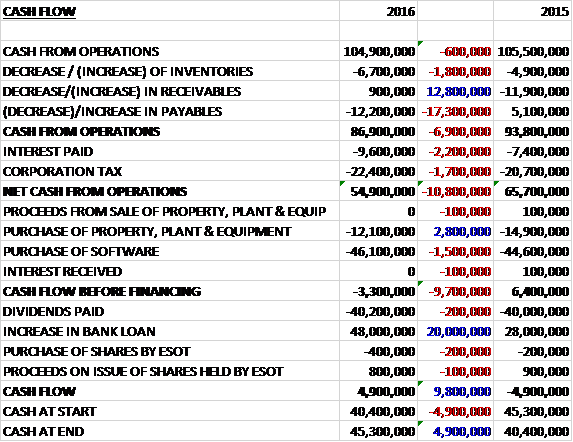

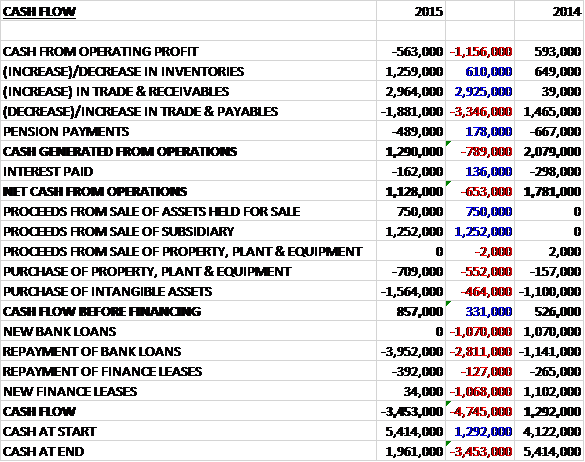

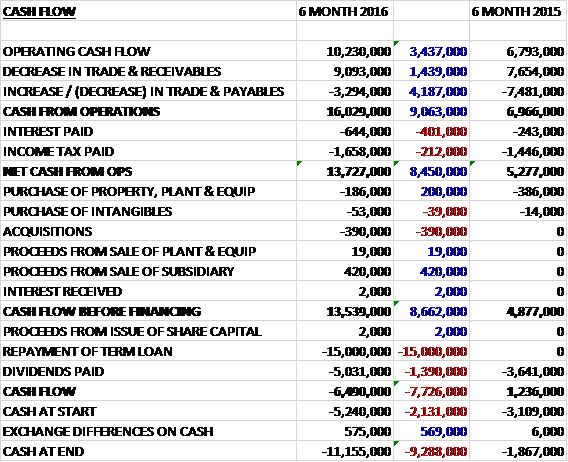

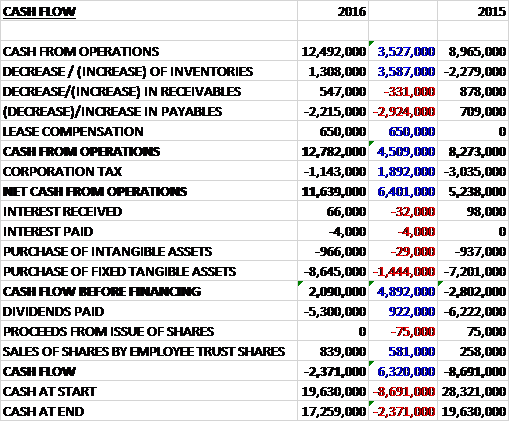

Before movements in working capital, cash profits increased by £2.1M to £3.5M. There was a cash inflow from working capital, although it was broadly similar to last year but tax payments increased by £250K and there was £1.3M less cash used in discontinued operations than last time so the net cash from operations was £5.1M, a growth of £3.1M year on year. The group then spent £1M on fixed tangible assets and £874K on the acquisition of some non-controlling interests in the Australian business so the free cash flow was £3.2M. Of this, £488K was used to pay back borrowings and £812K went on dividends but there was also an £825K draw-down of new loans so I suspect these figures have been massaged somewhat to show a good cash position at the year-end. In any case, there was a cash flow of £2.7M and the cash level at the year-end was £5.3M.

Overall, the UK business grew by 25%, significantly ahead of the published 7% growth in output of the UK construction industry in the year. In Australia they delivered a consistent financial performance even though the slowdown of China’s growth has impacted on the local economy. The office in Dublin has reported improving trading conditions as the requirement for new office space and residential properties increases. Whilst fee levels remain competitive, there are some signs of improvement particularly in the Highways and in the private development sectors.

During the year the group have recruited an additional 151 staff, an increase of 14%. This recruitment has impacted on the operational costs and margins in several of the businesses as it has proved necessary to recruit through agencies involving on off recruitment fees. The majority of the group revenue is generated from London based clients comprising major development companies, banks, pension and property investment finds. They are experiencing an increase in retail sector activity with 160,000 m2 of development designed by the group currently under construction on sites in Leeds, Newport and Oxford.

The operating profit in the Property businesses was £2.6M, a decline of £500K when compared to last year on margins that fell from 9.5% to 6.2% as the group needed to invest in the recruitment of additional technical staff to service the greater workload and salary costs have increased in line with the market.

The operating profit in the Structures division was £1.1M, a decline of £346K year on year on margins that fell from 9.7% to 5.3%. It has been necessary to increase headcount during the period to meet their client’s requirements and this has resulted in additional costs being incurred for one off agency recruitment fees which has reduced the operating profit and margins. The enhanced capacity within the team will be available to service the increasing workload and therefore the investment in staff should lead to higher margins in future.

The business continues to win awards for the structural design of buildings in all markets such as offices, retail and residential. One of the residential projects, Neo Bankside situated next to the Tate Modern, was shortlisted for the Royal Institute of Architects Stirling Prize.

The operating profit in the Building Services business was £452K, a fall of £122K when compared to last year on margins that fell from 7.4% to 4.2%. In October 2014, the Everyman Theatre in Liverpool won the Stirling prize for the ingenious use of natural ventilation to provide cooling in the theatre. This design involved the development of computerised thermal modelling to predict the future temperatures within the auditorium, thereby enabling the building services design to be finalised.

Tenant demand continues to drive towards commercial development, particularly in London where projects have provided a high proportion of the group’s revenue this year. They are also experiencing increased demand for their services in cities such as Manchester and Birmingham where developments are moving forward to tender and construction.

The group provided multidisciplinary services on the Land Securities development at New Ludgate in London which comprises office space located above retail units on the ground floor.

Following the completion of the project, the group has been retained by Land Securities on New Street Square in London which is a 27,000m2 pre-let to Deliotte. An unusual commission which is progressing on site is Angel Court in London developed by Mitsui Fudosan and Stanhope. This 27,000m2 project has involved the retention of significant parts of the existing core structure which is enclosed with a new steel superstructure incorporating an efficient building services system.

The Building Services team have been appointed by Generali to provide consultancy services on 10 Fenchurch Avenue which is a 46,000m2 mixed use office development located in the centre of London’s insurance district. The 17 storey building has been designed by the group to have an energy efficient façade to reduce solar gain while maximising useful daylight. In Birmingham the group has recently been appointed by Legal and General on their 15,000m2 Temple Court development.

In the residential market the demand the group’s structural and building services has been high. The Clarges development by British Land opposite the Ritz hotel in London where the group is providing a multidiscipline service, includes a new HQ for the Kennel Club. This 18,000m2 residential project provides 34 apartments arranged over ten floors. Two Fifty One is located in Elephant and Castle. This whole district is undergoing an extensive redevelopment and the group originally provided environmental planning advice on the regeneration of the area. The development is a 41 storey residential tower designed by the group in conjunction with Laing O’Rourke using their prefabricated system for the structure and building services systems.

Another project under construction is Tribeca Square at Elephant and Castle which comprises 40,000m2 of high quality residential homes for developers Delancey and Oakmayne. The group is appointed to provide structural engineering design services to Barratt on the development of the Sainsbury Nine Elms site. On completion, this site will deliver over 700 new residential units in Vauxhall. Recent completions include Buildings P1 and T1 for Argent at Kings Cross which provide over 300 luxury apartments.

Within retail and urban regeneration, several of the group’s clients’ town centre retail led developments designed by the group have progressed onto the construction phase. They are currently providing advice on over 600,000m2 of future retail development, of which over 160,000m2 is currently on site.

Large retail developments can often take many years to proceed through planning to completion and these projects provide good opportunities for the group to provide consultancy services at all stages. They are currently moving into a period where retail commissions will be providing an increasing proportion of revenue. Their extensive track record has enabled them to secure commissions on the next series of large retail centres moving through the planning system such as Brent Cross in London and Whitgift Centre in Croydon.

Projects designed by the group include Friars Walk in Newport, a 38,000m2 retail led development for Queensbury Real Estate which is opening in autumn 2015. The 42,000m2 first phase of Victoria Gate in Leeds commenced on site in 2014 and involves the construction of a John Lewis store and retail units. The group has been involved in this project for over ten years providing planning and preconstruction services to the developer, Hammerson, for the 100,000m2 development. They are currently providing design services for structures and building services to Sir Robert McAlpine who appointed for the construction of the first phase of the project with completion in 2016.

The third development designed by the group, which recently commenced on site, is the 80,000m2 extension to the Westgate Centre in Oxford for Land Securities and the Crown Estate. This project is due for completion in autumn 2017 and is anchored by a 14,000m2 John Lewis store with retail and leisure units along a mall leading onto the existing shopping centre, which is also being refurbished. In London the group has provided consultancy services to the Crown Estate on their projects in Regent Street. The latest development is St. James Market which provides 31,000m2 if mixed use retail and commercial space in two significant buildings between Haymarket and Lower Regent Street.

In the Leisure industry, the group is providing building services to Reignwood Group on the redevelopment of Ten Trinity Square of London. The original building was previously the HQ of the Port of London authority, is grade II listed and overlooks the Tower of London. The building is being retained and sympathetically transformed into a luxury Four Seasons hotel with 100 rooms. The complex routing and access requirements of the building’s services has been considered by the group to limit damage to any of the heritage areas and particularly the ceilings.

The group has been appointed by the British Museum to carry out a full energy review of their Bloomsbury site which extends over 75,000m2. This review will evaluate and proposed means of significantly reducing the carbon emissions from the buildings.

The Education market has remained a major sector for the group’s regional offices with commissions for primary and secondary schools plus further and higher education schools. As part of the Education Funding Agency priority school building programme, the group has been appointed as designers for the Harris Academy for 1,150 students and the Stratford Academy for 1,500 students in London. They are currently designing the Holywell primary and secondary schools as part of the North Wales schools framework. Construction is progressing and the schools are programmed for delivery in the summer for 2016.

In the North West they have been appointed to provide detailed design of six schools within the priority schools building programme. These schools are of significant importance as they represent the first series of schools designed to the new education funding agency design guidelines. There is a greater emphasis on computer simulation based design techniques and strict energy targets for all aspects of the building energy use.

The group’s regional involvement in industrial projects is increasing. They are currently providing design advice to Rolls Royce on their jet engine casing production facility in Nottinghamshire and Siemens have appointed them to design their new wind turbine factory in Hull. In Nuneaton they continue to provide multidiscipline consultancy services on the Motor Industry Research Association complex. The redevelopment of the site will provide a location for the European research and development of motor vehicles and associated components. It is expected that development will be phased over the next ten years.

As part of the ongoing framework with the Manufacturing Technology Centre, the group have designed a third technology building for their client in Coventry. This advanced manufacturing technology centre will showcase the cutting edge of British technology and provide teaching facilities for R&D engineering. The group have been appointed by Vinci to provide multidiscipline design services for the construction of Allerton Waste Recovery Park. This project is a 13,500m2 multi-treatment development comprising an energy from waste facility, a mechanical treatment facility and an aerobic digestion unit. The park will produce 220,000 MWh of renewable electricity per annum and is due for completion an operation in 2018.

The operating profit in the Australian business was £1M, a growth of 156K when compared to 2014 on margins that increased from 13% to 15.2% with demand remaining robust in many of the markets despite the slowdown in China. In Melbourne, justice, healthcare, residential, sports and recreational markets have provided a base workload for the office. During the year the group designed and documented the A$130M Royal Victorian Eye and Ear Hospital and the Monash Children’s Hospital with a construction value of A$260M. They have recently been appointed designers for the A$200M Sunshine Hospital Women’s and Children’s Centre and this will generate fee income over the next two years. Another appointment is the technical advisory role on the A$100M expansion of Casey Hospital in Victoria.

In the Sports and Recreation market, the group have completed the design of the Eltham Leisure Centre and Aquanation Aquatic Centre in Ringwood. They are currently designers for Franksten stadium and Bendigo Stadium. They have completed building services designs for the new A$40M Robert Bosch HQ on the Clayton Campus in Melbourne. New appointments include a technical advisory role at St. James Cook University in Cairns and building services designs for an $A150M residential development in St Kilda Road in Melbourne.

In Sydney, the residential, education, bank fit out and telecoms markets remain strong. The group have been appointed to provide building services design on the A$100M Northpoint retail and hotel development in North Sydney where the client wishes to use their 3D design and draughting capability on this project. In the residential market, Airlie Beach resort development providing 101 apartments in Queensland has recommenced and the group is appointed for both the building services and structural design. Universities have continued to generate revenue as they expand their campuses to accommodate overseas students. They are currently working on projects at UTS, Sydney University, University of South Wales, Wollongong University and Macquarie University.

The financial services sector is experiencing a roll out upgrades in the retail outlets of many high street banks. The group has been appointed to provide building services designs for the refits for Commonwealth Bank, Westpac Bank and St. George Bank across Australia. These are ongoing commissions and they have completed one hundred branches to date with an additional three hundred branch refurbishments expected to continue to generate revenue over the next three years.

The group relocated their offices from the outskirts of Sydney into a more central city location in February 2015. The new office provides better connections with clients, thereby reducing travel time. In addition they are aiming to recruit additional staff to service the increasing workload and the city centre location provides a greater access to the available staff pool in the city.

The operating profit in the European business was £48K, an increase of £47K year on year on margins of just 1.7%, although the business has returned to profitability after a number of very challenging years. The Irish economy recorded the strongest growth figures in the Eurozone last year and investment in commercial property in Dublin has increased significantly. The residential sector is also growing with a drive towards properties for lease rather than traditional housing for sale. Retail, hotel, industrial and logistics sectors are expected to become more active in the future. The property sector in Poland remains subdued, though, with some signs of increasing investment. The Warsaw team has therefore continued to provide technical support on London and Dublin projects.

The Dublin office has seen considerable growth in its residential workload in the year as projects start to move from the planning stage to construction. New commissions secured include the 200 unit Marrsfield apartment scheme and projects at Waterside Swords, Station Road Portmarnock, Oldourt in Firhouse and at Kilternan. Planning for phase 3 of the Clancy Quay development has also commenced. Construction is now underway at Royal Canal Park for Ballymore, Oldtown and Clongriffin for Gannon and at Clancy Quay and Central Park for Kennedy Wilson.

The group has been appointed by Green REIT to provide structural design services for a 13,000m2 office scheme at Central Park and by state agency IDA Ireland for an office development at Tralee Technology Park, County Kerry. Construction of a major refurbishment and extension to Baggot Court in Dublin has started and will provide 18,000m2 of grade A office space on completion. Planning stage services have also been completed for 35,000m2 of new development as part of the Capital Dock Scheme.

The retail sector remains more subdued, although there are signs of activity levels starting to pick up. Planning stage services have been provided for a major upgrade to Stillorgan Shopping Centre where the group are appointed to provide structural and building services engineering. Construction of Aldi’s Terenure store in Dublin, which incorporated elements of a historic tram terminus building, has recently been completed and is due to open for business in autumn 2015. They have subsequently been appointed for the design of several new Aldi stores.

The group continues to be one of the leading consultancies in the education sector in Ireland. Several new commissions have been secured, including the 32 classroom Harcourt Urban primary school which is to be developed as an exemplar project for the Irish Department of Education, a six hundred pupil secondary school in Galway, and the rapid build schools framework for 2015. For this latter appointment, they have already provided all civil and structural work required to obtain planning and to procure design and build contractors for new schools at thirteen sites. Detailed design has started for the 1000 pupil Kingswood secondary school in Dublin while construction of several primary school projects has been completed in the year.

The group have strengthened their teams through recruitment of additional senior and support staff. Their building services team, only established in 2014, has made better than expected progress and an increasing number of projects are now being awarded on a multi-discipline basis. As a result the group is well positioned to benefit from the recovery in the Irish economy.

In Warsaw they have completed a number of fit out commissions for tenants of the Pramerica Tower in Krakow, following completion of refurbishment work at the building in early 2015. Structural design work for a 34,000m2 office in Warsaw has now been completed with construction due to start in the coming months. They have been appointed to provide multi-discipline engineering services for Palace Park, a new leisure and residential community development south of Warsaw and feasibility work for a retail refurbishment and extension scheme at Zielona Gora. The operating loss in the other International business was £16K, a detrimental movement of £201K when compared to last year.

The operating profit in the Infrastructure and Environment segment was £200K, a positive movement of £1.8M year on year on margins for just 0.5% with the improvement in revenues primarily due to growth in the Highways and Transportation Outsourcing business which has experienced a strong demand for services. The actions taken in 2014 to restructure the management of the Civil and Transportation Consulting business and to reduce costs and increase utilisation has significantly reduced the losses in this business with the current year loss in part due to one off provisions in legacy projects as the underlying performance moves towards a profit in the future. The board anticipate that public sector frameworks and transportation planning will generate additional revenue in the near future.

The operating loss in the Civil and Transportation consulting business was £1.2M, an improvement of £1.7M when compared to 2014. Included in this loss are legacy issues from historic projects which have been protracted and one off provision of £500K on two projects where financial account settlements have been reached with clients. Following the restructuring of the business in 2014 significant improvements in the underlying performance have been achieved. It has now been streamlined and the forward order book has improved, giving confidence that it is on course to deliver a return to profitability in the future.

In Transport Planning, in the South the residential sector has provided a good revenue stream through the delivery of immediate supply sites as well as promotion of strategic land through local plans for clients including Linden Homes, Barratts, Crest Nicholson, Coca Cola, Cala Homes, Network Housing and Hyde Group. Key commissions included providing the transport planning advice on a major mixed use and residential development at Sampson House in Blackfriars, in addition to ongoing work advising the redevelopment of Cringle Dock adjacent to Battersea Power Station to provide a new waste transfer station with 450 residential units above.

The group continue to provide transportation and highways advice to the States of Jersey Development Corp for the six building finance centre on the St. Helier sea front. Following planning consent, they are also working with the new owner of the site adjacent to Hampton Court Station to further optimise the site layout and junction work for this residential led mixed use scheme. In Milton Keynes they have provided transportation advice to Hermes, the owners of the main retail centre, on their emerging development plans and have recently helped secure planning consent for a major new multi storey car park.

The Manchester transportation team has continued to grow and provide technical support to the teams across the North of England and Scotland. Notable commissions included assisting Peel Energy with the expansion of their Scout Moor onshore wind farm, and delivering numerous transport assessments for Scottish school projects commissioned through the Hub West Framework.

Within Transport Infrastructure and Highways, in London and the South East, having completed the design of the Bedford Western Bypass on behalf of the local council, the team is now retained for the £18M construction phase by J Breheny Contractors. They have also been providing transportation advice and support to a number of proposed allocations in local development plans that are being formulated throughout the UK. In the South West the team was appointed on a number of significant sized infrastructure schemes including a new link road and enabling works in Abbeymeads in Swindon, Crosshands and South Sebastopol near Cwmbran.

In the rail sector the team has been engaged on the National Station Improvement Programme designing upgrades at Clapham Junction, Farnborough, Crystal Palace, Faversham, Rainham, Portsmouth and Southsea, Putney, Virginia Water, Walton on Thames and Hatfield. They are also providing the Network Rail role contractor’s engineering manager for a number of sizeable developments. One includes the redevelopment around Twickenham stations and another the 32 storey Atlas development adjacent to the railway viaduct in Vauxhall.

In the aviation sector the group have provided support to British Airways at Heathrow with maintenance projects and recent new commissions relating to aprons, carparks, fire mains and hydrants. Work at London City airport has also been growing with the group providing civil, structural and building services support for the extension of the West Pier and civil engineering support on a number of maintenance projects. In the marine sector the group provided engineering input and ground contamination advice to support the planning application for a new cruise liner berth at Dun Laoghaire harbour in Ireland, supporting the wider services being provided by the Dublin office.

In Scotland the group has been very active in the energy sector, providing design services to a number of distribution network operation companies in the uploading of the national grid infrastructure on projects of national significance such as the Moray to Caithness high voltage direct current project and the Foyers to Knochnagle upgrade. They have undertaken the design role for a number of major substations in the Highlands including a twin 275KV substation at Darigaig which involves the blasting of rock and conventional mechanical extraction of over 200,000m3 of material in some of the remotest country in the UK.

The group have also, in conjunction with SSE and Shell, provided geotechnical assistance for the horizontal directional drilling study on the world’s first large scale gas carbon capture and storage project at Peterhead power station. The group has continued to support Vinci in constructing the Energy from Waste plant in Allerton and in the design of the Cringle Dock project in London.

The London infrastructure teams continue to provide urban regeneration services to many clients including Hammerson, Land Securities and Hermes. In Brent Cross and Canada water they are providing strategic infrastructure advice on drainage and services within the site perimeter. Other retail and residential projects include schemes in Didcot Orchard Centre, Exeter Bus Station and Nine Elms in Battersea. Within London the drainage team are working on the refurbishment and extension of several office, retail and residential blocks including the redevelopment of St. Barts hospital and several sites around Covent Garden and Southampton Street.

The civils teams in the south have been engaged on a number of Waterman Property group projects as well as supporting Berkeley Homes on their Riverside development in Woolwich, St. James Street and Ringway Island roads. The services provided include ground movement analysis, bridge assessments and design, design checks of all subcontractor work as well as obtaining approvals for development over or adjacent to third party assets such as London Underground, Network Rail, RMG, Thames Water and London Overground. They also continue to provide temporary works design and checking for major contractors such as O’Rourke, O’Keefe, Volker Fitzpatrick, ISG and Vinci.

In Bristol, they were appointed to provide civil and sub-structure design advice on Cody Park, a data centre for Ark Continuity, which follows similar ongoing work at Spring Park for the same client. Pre-planning flood risk assessments and water resources assessments have been completed for St. James Group for the redevelopment of Southall Gasworks, which has led to the provision of design advice. The Civils and Infrastructure business in Manchester continues to work on projects commissioned through the Mersey Travel framework, which is the integrated transport authority for Merseyside. Work also continues for Metrolink and MPT in relation to the tram system. Schemes in Leeds and Oxford are nearing design completion and are on site encompassing drainage, S278 and streetscape improvements for major shopping centres.

The group have been working in long term partnerships with many public sector clients for nearly 20 years and have recently secured significant extensions to some of these frameworks. In the London borough of Bexley, the group has held frameworks with the council since 1996 providing a range of engineering consultancy services. Earlier in the year, this contract was extended for up to four years and includes provision of traffic and transportation engineering services over and above the current scope of civil, highway, bridgework, drainage and staff secondment. The framework is an important part of the long term regeneration framework of the borough’s growth strategy for its economic, environmental and social regeneration. The programme aims to strengthen Bexley’s reputation as a desirable location to live and do business with plans to expand its transport infrastructure and education programmes.

In Crawley, the group has secured a two year extension of three partnering contracts with the council, providing civil engineering, flood alleviation, drainage and structural engineering services. More recently the business was appointed to the North Lincolnshire Council Framework which is for an additional two years with the option for further extensions. Services include highway design, bridge engineering, traffic and transportation, drainage design and surface water management.

Following on from previous successful frameworks, the group has been appointed to a new four year framework with Mersey Travel to provide multidisciplinary engineering consultancy services covering expertise across rail, civil and structural, transport, highways infrastructure and business case development.

The operating profit in the Civil and Transportation outsourcing division was £787K, a growth of £117K year on year on margins that reduced from 4.8% to 4%. This year saw continued strong demand for the group’s specialist secondment services in the highways and transport markets and in response to this they increased staff numbers. This necessitated an enhanced overhead support structure to manage the larger number of engineers on secondment and support plans for future growth. Government investment in the highways programme and on major infrastructure projects has created a skills shortage. The requirement for the group’s services has increased and margins are likely trend upwards in future years as skilled resources become sought after by local authorities, consultants and contractors.

The group’s specialist secondment business has built a strong track record by seconding engineers to a range of clients in the highways and transportation sector. In the last year the significant increase in employee numbers has been achieved by incremental growth in all parts of the UK, underpinned by a strong performance in servicing three major local authority frameworks.

The Midlands Highways Alliance Professional Services Partnership contract was re-awarded to an AECOM/Waterman partnership in April 2015. This framework is in its seventh year and has expanded to serve 20 local authorities and extends to 2018 with the additional potential for a one year extension. Demand has remained strong at as of the year-end they had 76 staff working within these authorities. The group is also supporting AECOM with a further 18 staff on its other local authority commissions.

The West Midlands Highways Alliance is the corresponding framework in the West Midlands area. This contract was awarded in 2013 to an Atkins/Waterman partnership. Over the course of the year, the number of seconded staff working within the three main participants, Warwickshire County Council, Coventry City Council and Solihull Borough Council, has increased to 82 with the framework extending to 2017.

The Hampshire County Council Strategic Partner contract, also in association with Atkins, was awarded in April 2014 and the group have 30 seconded staff in place. With satisfactory performance this initial four year contract which ends in 2018 has the potential to be extended to 2022. The group is also supporting Atkins with a further 30 staff working throughout the UK.

These major framework wins have been captured by collaborating with partner consultants and the group continues to secure further opportunities on future bids and frameworks. The client facing management team has been strengthened in all parts of the UK and they are targeting diversification into new sectors such as water, utilities and rail. The group differentiate themselves from recruitment agencies by employing the majority of their secondees and employees receive varied experience and effective training and development.

The operating profit in the Environment division was £600K, broadly flat year on year on margins that declined from 7.2% to 5.9%. The group has made progress with respect to diversifying the business into the infrastructure market and prospects for the new year remain positive with good levels of forward orders. The business focuses on maintaining long term relationships with clients.

It has been a good period for the group’s due diligence service. They cemented their position as a leading advisor to the real estate sector and was awarded Property Due Diligence Firm of the Year by Acquisitions International. In the UK the business advised Blackstone on the refinancing of the large and recently acquired Max Property Group, whilst in Europe they supported BMO Real Estate Partners on their first European acquisition involving properties in Germany, Belgium and Netherlands.

In the infrastructure sector, the team supported the acquisition of Glasgow, Aberdeen and Southampton Airports by Macquarie and Ferrovial, Toulouse Airport, Green Highlands Renewables and Wightlink Ferries. Transactional work in the mergers and acquisitions field also experienced growth, with particular emphasis on the leisure sector. They also advised on a number of corporate deals, including the acquisition of Away Resorts and Bridge Leisure. As the business continues to diversity its service offering, it has established itself as a leading adviser in responsible investment, developing a series of services.

The environmental management advisory system was expanded to cover corporate environmental, health, safety and carbon management services. In addition to data security, this year the team developed a new Hazard Register function, initially for Tata Steel, but with a view to expanding the function to other clients. This tool allows customers to document, assess and control their occupational health and safety hazards. There has also been growth internationally and the hazard register is now operational in Sweden, Holland, Australia, China, Russia, Malaysia and the US.

The health and safety team has positioned itself at the forefront of the transition to CDM 2015, offering high quality and commercial principal designer and client advisor services having been appointed as advisor on a large number of high profile projects.

The group strengthened its position as a leading provider of pre-panning environmental impact assessment services for urban regeneration projects. Notable large scale commissions in London included continuing to support the proposals at Brent Cross for Hammerson and Standard Life Investments; phase 4A of Battersea Power Station for the development company; British Land’s plan for Canada Water encompassing Harmsworth Quays, Surrey Quays Shopping Centre, and the Surrey Quays Leisure Park; Ballymore’s 2.43 hectare residential scheme in the docklands; and advising Car Giant and London & Regional Properties’ masterplan for their 46 acre site at Old Oak Park.

In the South West the team provided pre-planning services to a host of schemes across the residential, commercial, industrial, leisure and retail sectors. In the residential sector the business supported Taylor Wimpey on three schemes in Wales, in addition to advising on a major residential development on the outskirts of Hereford. For the past two years the business has also been advising on environmental issues and designing the infrastructure and highway improvements for the Graven Hill New Urban Village in Bicester, a 207 hectare operational MOD site that has been purchased by Cherwell District Council.

In the North and Midlands, the business began the year advising on major residential led developments proposed in Lincolnshire and Cambridgeshire. As the year progressed, an outline planning application was submitted for a 90 hectare strategic greenfield site in the Midlands for a residential led scheme providing up to 1,700 units along with a retirement village, commercial units, community facilities, a primary school and an energy centre. During the year a new masterplan was also developed for the Hungate site, the residential led scheme for Lend Lease/Evans Property joint venture in York.

In Scotland, the team have been provided detailed support to TH Real Estate on the detailed design and application process for the £850M Edinburgh St. James project, involving key inputs to support two successful planning committee hearings, including the high profile central hotel design. The business is also finalising the EIA, together with specialist marine consultancy Fugro, for the £350M Aberdeen Harbour expansion project, one of Scotland’s key national infrastructure projects. Elsewhere, specialist technical support has been provided on a wide range of residential, retail, education and healthcare projects, the latter of which as part of a multidisciplinary Waterman offering in the HUB framework.

Ecological services continued to build on the growth seen in previous years with the business expanding nationally and advising on a number of projects including Land South of Newark for Catesby Properties, Land South of Clovelly Road Bideford for Linden Homes, Leybourne Grange for Taylor Wimpey and a portfolio of sites for Aldi across Scotland. Of particular note is the addition of specialist aquatic ecology services to the national skill set via the Glasgow office. Complimenting this service line, the Landscape and Heritage teams also grew nationally, providing a holistic approach and an integrated design solution.

The acoustics team continues to experience growth in both the property and non-property sectors. The business has recently completed acoustics assessments for Hampden Park Stadium in Glasgow together with providing acoustic support from pre-planning to completion for major developments throughout the UK. Key commissions include St. James Quarter, Edinburgh, and One Angel Court in London, whilst work also continues on a number of high profile projects including Two Fifty One a residential development in Elephant and Castle, Clarges Estate, a high end residential development in Mayfair, and 10 Trinity Square, the conversion of an existing Grade II listed building to provide residential and hotel development.

The group’s land quality and brownfield regeneration team experienced significant growth in workload during the year, advising on a number of complex projects. In London, work progressed at the Old Gasworks in Sutton with the demolition of two has holders and an eleven storey tower block. The business has also been supporting Royal Mail in the redevelopment of the South London Mail Centre at Vauxhall, itself a former gas works. This site is one of the largest remediation projects in London at the moment.

Detailed geotechnical and environmental investigations have been completed on a number of projects where the interaction of London Underground infrastructure has been carefully modelled and where foundation solution for high rise towers have been designed without impacting the neighbouring buildings. Outside London, the Bristol business has had a busy year, delivering a wide range of assessments on a number of different mixed use and commercial schemes for Kier and residential led developments for Taylor Wimpey. They have also completed a large ground investigation for the Esplanade Quarter in Jersey and continue to support the client on delivering the first phase of development as part of the overall group engineering services.

The Leeds and Manchester businesses are continuing to assist with the John Lewis anchored Victoria Gate scheme in Leeds, supporting Sir Robert McAlpine with site enabling works. The team is also continuing to provide support to Vinci with the geotechnical design of the plant in Allerton and the remediation specialists are also assisting with the ground remediation of a former RAF base in Cambridgeshire.

In 2013 the board decided to discontinue trading in the UAE and in 2014 they stopped trading in Russia and last year, the loss from these discontinued operations was £3.8M.

Clearly the group is very susceptible to the economic environment which would impact on expenditure on construction projects from both public sector and private sector clients. It is also worth noting that one client represents 7% of the total group revenue. Whilst not that excessive they are still rather susceptible to the loss of this client. The group is somewhat susceptible to exchange rate movements. If sterling had strengthened 10% against the Australian dollar the profit would have been £77K lower and if it had strengthened 10% against the Euro, profits would have been £12K lower.

In April 2015 the group purchased an additional 20% of Waterman International Asia from a retiring director, John North, for the sum of £820K. The book value of net assets acquired was £570K and the difference has been deducted from equity. They now own 100% of WIA, 100% of AHW and 51% of AHW Victoria. The purchase was funded by a term loan from HSBC which is repayable over four years.

It is worth noting that the directors have awarded themselves 3,000,000 options over shares at nil costs which all vest if the share price hits 150p and stays there for 25 days, over the next ten years. This does not seem to be a particularly taxing target and as I have seen with Tristel, it can be counter-productive to have these kinds of targets as bad news tends to be held back if the options are lose to vesting.

The group’s order book has grown by 8% to £130M and the range of future work is more diverse than in previous years. In the short term, the group is focused on improving the performance of their Civil and Transport Consulting business. The board is confident of meeting their targets for the coming year and aim to increase operating profit margins from the current level of 3.3% towards 6% by 2019.

The group had a net cash position of £3.8M at the year-end compared to £1.6M at the end of last year. At the current share price the shares have a PE ratio of 18.5 which reduces to a cheap-looking 10.5 on next year’s consensus forecast. After a doubling of the total dividend, the shares are yielding 2.4% which increases to 3% on next year’s forecast.

Overall then this has been a decent year for the group. Profits were up but net assets were modestly down. Operating cash flow improved, however, and the group generated a decent level of free cash flow. The operating performance was mixed with the structures and building services businesses suffering from increased costs relating to a greater level of staff being taken on. The Australian and Irish businesses fared well, however, which is good to see particularly with the Australian economy being effected by the Chinese slow down – perhaps this is yet to filter through. The Polish market is still difficult though.

The Civil and Transportation consulting business remains loss making but the performance has improved and the board seem confident that it can contribute a profit going forward. The outsourcing business put in a strong performance, however, and the environment business put in a solid performance with profits flat despite a fall in margins. Going forward, the order book has increased, there is a decent 3% forward yield and the forward PE of 10.5 looks good value. It is worth noting, however, that the business would be very susceptible to a slowdown in construction. Despite this, this could be a good investment.